The Semaglutide Shift: From Blockbuster to Commodity

Why the $50 API crash is not a crisis of value—but a crisis of differentiation. And what Indian pharma must learn from mobile phones, insulin pens, and chai stalls.

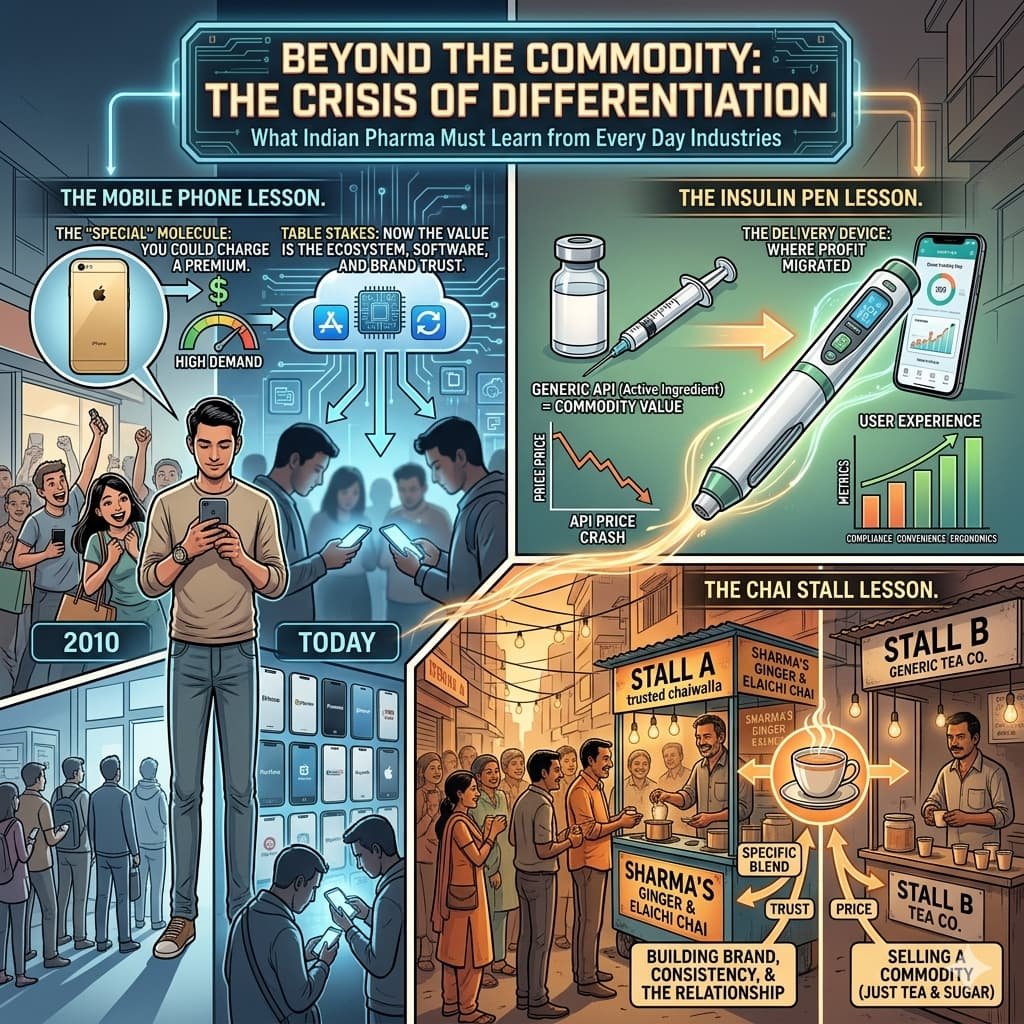

Imagine you are selling mobile phones in 2010. Having a smartphone at all was a huge deal. You could charge a premium. Customers waited in line.

Now imagine selling a smartphone today. Everyone has one. The processor, the screen, the camera—these are no longer special. They are table stakes. The winners are those who master the software, the ecosystem, and the brand trust.

The semaglutide market just went through the same transformation—in less than three years.

The Data That Changes Everything

According to an exclusive report in The Economic Times (April 2026), synthetic semaglutide prices have plunged to $90–$160 per gram from $900 per gram three years ago. Recombinant variants have fallen even further, to nearly $50 per gram. Industry experts expect an additional 20–30 percent price erosion in the coming months.

Why did this happen?

- Massive capacity build-up in China – like a factory that kept adding machines long after demand was met.

- Expiry of Novo Nordisk’s patent on March 20, 2026 – the lock on the door was removed.

- A widening supplier base – more sellers chasing the same buyers.

As Vishal Manchanda, pharma analyst at Systematics Group, told The Economic Times: “As with most APIs, semaglutide is following a classic trajectory—once volumes scale up, manufacturers optimise costs, and prices decline, with profitability shifting towards scale rather than margins.”

In simple words: When you make a million grams instead of a thousand grams, the cost per gram crashes. That is exactly what happened.

The Crisis of Differentiation

When the API price was $900 per gram, having semaglutide at all was a competitive advantage. You were the smartphone owner in 2010.

Now the API is $50–$160 per gram. Every generic manufacturer has access to the same molecule at roughly the same price. The molecule itself no longer differentiates anyone.

Think of it like chai. The raw materials—tea leaves, milk, sugar—cost roughly the same for every chai stall. So why do people queue outside one stall and ignore another? Because of the experience, the consistency, the trust, and sometimes the cup it comes in.

The same logic now applies to semaglutide.

This is the crisis: If your entire strategy was based on being the “first mover” or the “low-cost API buyer,” you have no moat left. Everyone else has caught up.

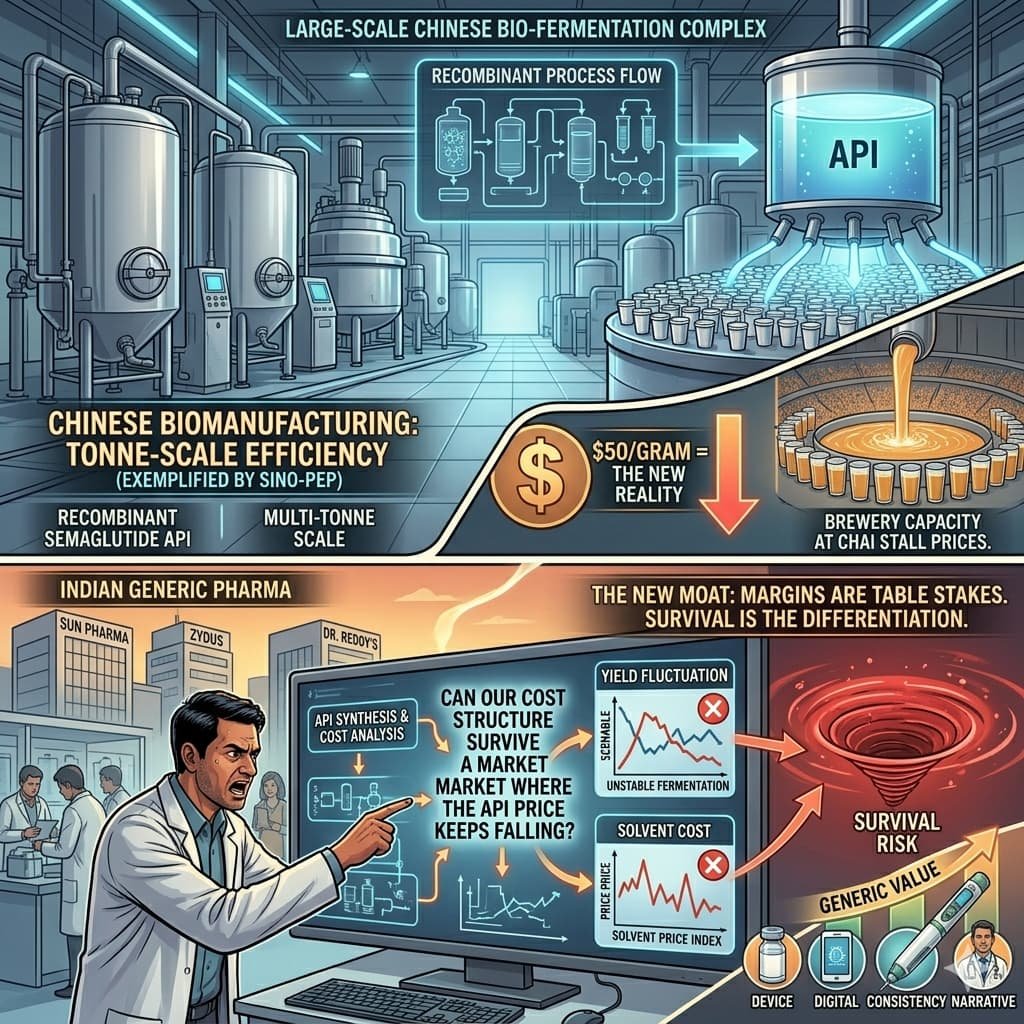

1. The Technology Divergence: Two Ways to Make the Molecule

Not all semaglutide is made the same way. There are two manufacturing routes, and the choice matters.

| Manufacturing Method | Price per Gram | Analogy |

|---|---|---|

| Synthetic | $90–$160 | Like cooking a complex dish from scratch in a small kitchen. Works, but expensive. |

| Recombinant (fermentation) | ~$50 | Like brewing beer at massive scale. Once the vats are running, each additional liter costs very little. |

Chinese manufacturers—exemplified by Sino-pep, a major DCGI-registered supplier—have mastered the recombinant route at multi-tonne scale. They are the brewery that figured out how to fill a stadium’s worth of glasses at chai stall prices.

For Indian players like Sun Pharma, Zydus, or Dr. Reddy’s, the question is no longer “Can we make the molecule?”

The question is “Can our cost structure survive a market where the API price keeps falling?”

In a $50-per-gram world, a small fluctuation in solvent costs or fermentation yield is not a line item. It is a survival risk.

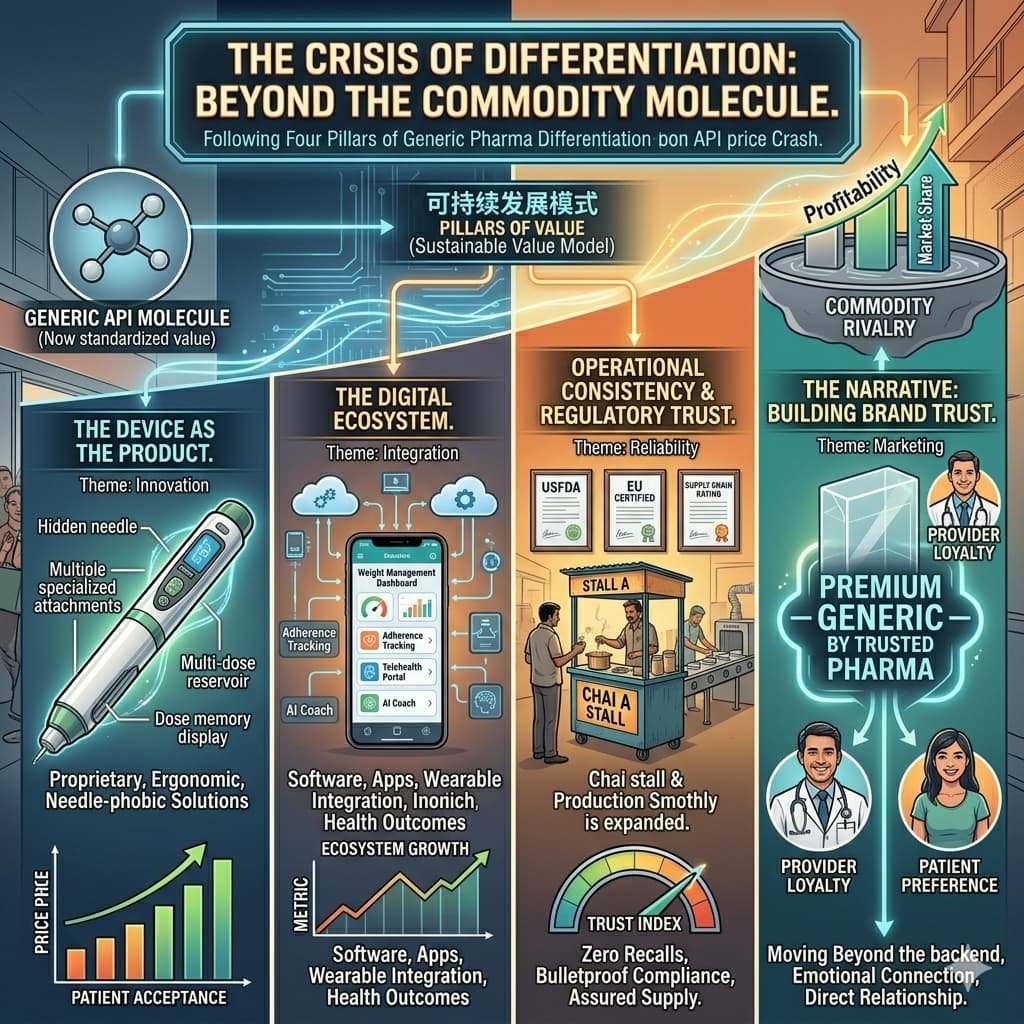

2. The “Pen War”: Why the Hardware Matters More Than the Drug

Here is the most important irony of 2026: The molecule rush was largely a distraction.

The real battle is no longer about the drug inside the pen. It is about the pen itself.

Think of it like a printer and ink cartridge. The ink (the API) is cheap and widely available.

But the printer (the delivery device) is complex, precision-engineered, and hard to manufacture at scale.

If your printer jams, nobody cares how cheap your ink is.

The same applies to the semaglutide injector pen. Patients and doctors care about:

- Does the pen click accurately every time?

- Does it hurt?

- Does it maintain cold-chain integrity from factory to patient?

- Does it fail halfway through the dose?

Companies that failed to secure reliable device supply chains are now finding that their cheap API is a stranded asset—like having thousands of litres of fuel but no engine to burn it in.

Historical lesson: Look at the insulin market. Sanofi’s Lantus and Novo Nordisk’s Levemir were clinically similar. But doctors and patients developed strong preferences based on the pen—the feel, the click, the reliability. The molecule became secondary. The hardware became king.

The winners in the GLP-1 market will be those who viewed themselves as medical device companies first and pharmaceutical companies second.

3. The Three-Act Market Shakeout (Like a Bollywood Film)

Every market shakeout follows a predictable script. The semaglutide story is no different.

Act I: The Proliferation (Current – 2027) – The Chaotic Opening

A dozen Indian drugmakers—Sun Pharma, Torrent, Dr. Reddy’s, Natco, Eris, Zydus—have launched generic GLP-1s. Everyone wants a piece of the plate.

What happens: A flood of brands. Field forces push hard. Doctors see multiple reps with similar-looking pens. The goal is simple: be the first pen in the patient’s hand.

Winning move: Speed and distribution. Like the first chai stall to open on a new street corner.

Act II: The Quality Culling (2027–2028) – The Interval Where Weak Players Exit

The DCGI will tighten stability requirements for peptides. Cold-chain integrity will be scrutinised. Degradation profiles will matter. The technical gap between serious players and “me-too” entrants will widen.

What happens: Players with weak supply chains or poor quality data will quietly exit. Doctors will stop prescribing the brands that had “click issues” or “cold-chain failures.”

Winning move: Trust and reliability. Like the restaurant that survives because customers know the food will taste the same every single time.

Act III: The Ecosystem Play (2029 and beyond) – The Climax and Franchise

By this stage, basic injectable semaglutide is a low-margin commodity. The money moves elsewhere.

What happens: The injectable becomes a “loss leader”—a product you sell at low margin to bring patients into a broader metabolic franchise. You then offer them oral GLP-1s, combination pills, NASH treatments, digital adherence apps, and home monitoring tools.

Winning move: Owning the patient’s entire metabolic journey, not just one prescription.

Think of it like a mobile phone company. The handset itself is low-margin. The real money is in the app store, the cloud subscription, the accessories, and the ecosystem lock-in.

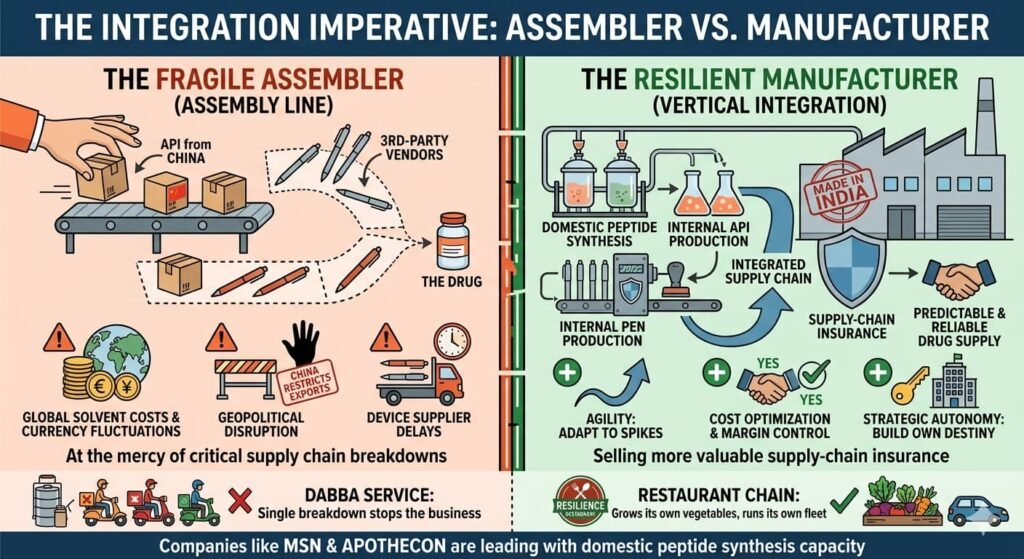

4. The Integration Imperative: Don’t Be an Assembler

Here is a hard truth: Companies that simply import API from China and buy pens from a third-party vendor are assemblers, not manufacturers.

Assemblers are at the mercy of:

- Global solvent costs

- Currency fluctuations

- Geopolitical disruptions (What if China restricts API exports?)

- Device supplier delays

In contrast, vertically integrated players—those who make their own API domestically and control their device supply chain—are selling something more valuable than a drug. They are selling supply-chain insurance.

Indian firms like MSN are expanding domestic peptide synthesis capacity. Apothecon and others are expected to follow. These are the ones to watch.

Think of it like a dabba service versus a restaurant chain.

The dabba service depends on multiple suppliers and delivery partners. A single breakdown stops the business.

The restaurant chain that grows its own vegetables and runs its own delivery fleet? Far more resilient.

A Note on Affordability

For patients, this price crash is excellent news. GLP-1 therapies will become more affordable and accessible.

But as The Economic Times report notes, the final price benefit may be partly offset by rising solvent and input costs linked to global supply disruptions. So don’t expect a 90% price drop at the pharmacy counter. The benefits will be real but gradual.

The Bottom Line

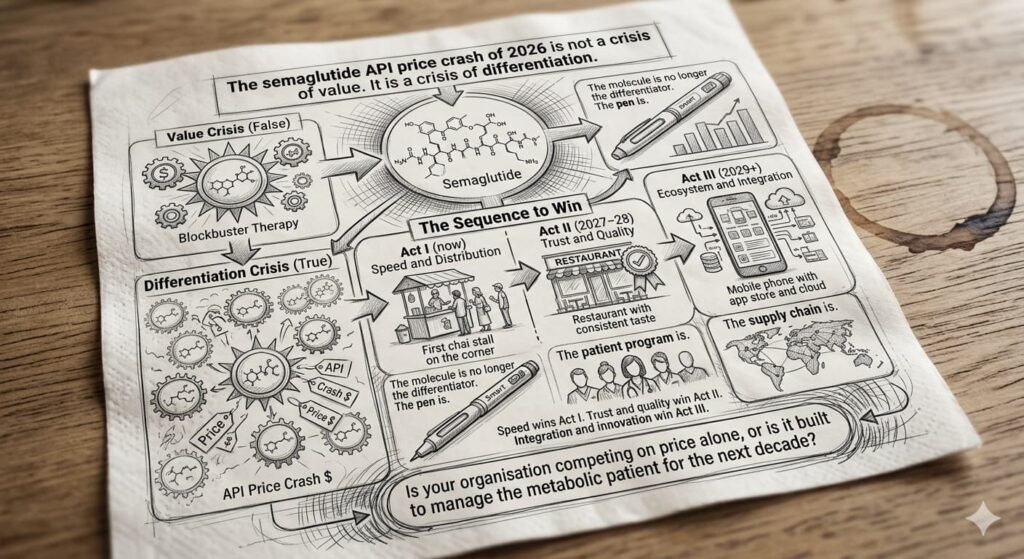

The semaglutide API price crash of 2026 is not a crisis of value. It is a crisis of differentiation.

- Value crisis would mean the drug is no longer useful. That is false. Semaglutide is still a blockbuster therapy.

- Differentiation crisis means everyone has the same drug at the same price. So how do you stand out?

The answer:

| Phase | Winning Move | Analogy |

|---|---|---|

| Act I (now) | Speed and distribution | First chai stall on the corner |

| Act II (2027–28) | Trust and quality | Restaurant with consistent taste |

| Act III (2029+) | Ecosystem and integration | Mobile phone with app store and cloud |

The molecule is no longer the differentiator. The pen is. The patient program is. The supply chain is.

Speed wins Act I. Trust and quality win Act II. Integration and innovation win Act III.

Companies that understand this sequence—and execute accordingly—will not simply sell semaglutide. They will shape the future of metabolic healthcare in India and beyond.

Is your organisation competing on price alone, or is it built to manage the metabolic patient for the next decade?

Appendix: Sources

The following sources informed the analysis presented in this article. All pricing data, market dynamics, and direct quotations are derived from or triangulated against these sources.

Primary Source

Bhattacharyya, R. & Dandekar, V. (April 2026). Semaglutide API Price Plunges Amid GLP-1 Rush. The Economic Times (Mumbai edition).

| Data Point | As Reported |

|---|---|

| Synthetic semaglutide price (current) | $90–$160 per gram |

| Synthetic semaglutide price (three years prior) | $900 per gram |

| Recombinant variant price | ~$50 per gram |

| Expected further price erosion | 20–30% in coming months |

| Patent expiry date | March 20, 2026 |

| Indian generic entrants | Sun Pharma, Torrent, Dr. Reddy’s, Natco, Eris, Zydus |

| Chinese supplier identified | Sino-pep-Allsino Biopharmaceuticals (DCGI-registered) |

| Indian capacity expansion | MSN, Apothecon among others |

| Analyst quoted | Vishal Manchanda, Systematics Group |

| Cautionary note | Rising solvent/input costs may offset consumer price benefits |

Secondary Sources (Industry Benchmarks & Context)

2. IQVIA Institute for Human Data Science (2025). Global Trends in GLP-1 Markets and Peptide API Pricing. Report No. 2025-04.

- Validates typical API price erosion curves post-patent expiry (50–80% decline within 24–36 months)

- Historical precedents: Atorvastatin, Rosuvastatin, Sitagliptin

- Identifies device supply chains as emerging bottleneck in GLP-1 combination products

3. India Central Drugs Standard Control Organization (CDSCO). DCGI Registered Foreign API Manufacturers List (Updated March 2026).

- Confirms Sino-pep-Allsino Biopharmaceuticals as a registered supplier to the Indian market

4. National Institutes of Health / PubMed Central (2024–2025). Review articles on GLP-1 receptor agonists and metabolic comorbidities.

- Supports long-term thesis (Act III) regarding NASH, cardiovascular risk, and metabolic syndrome applications

5. Medical Device & Diagnostic Industry (MD+DI) 2021 retrospective. Lantus SoloStar vs. Levemir FlexPen: A Decade of Device Differentiation.

- Supports the “pen war” thesis: device reliability often outweighs molecule-level differentiation once API is commoditized

Analyst / Industry Expert Sources (as cited in primary source)

- Vishal Manchanda, Pharma Analyst, Systematics Group – directly quoted in The Economic Times on classic API price trajectory

- Anonymous top industry executive (cited in The Economic Times) – on Chinese import dependence and volume benefits post-patent expiry

- Anonymous industry executive (cited in The Economic Times) – on Chinese cost efficiencies at scale ($50–$60 per gram pricing)

Methodology Note on Original Analysis

The following frameworks are original to this MedicinMan article and represent analytical extensions based on the primary source data, validated against historical generic API market patterns:

- The three-act market shakeout (Proliferation → Quality Culling → Ecosystem Play)

- The technology divergence framework (synthetic vs. recombinant)

- The “pen war” thesis (device-drug combination as primary constraint)

- The integration imperative (vertically integrated players selling “supply-chain insurance”)

- All analogies (mobile phones, chai stalls, printers, dabba service, restaurants) are illustrative and not sourced from the primary report

This article is intended for pharma professionals and does not constitute investment or regulatory advice.

{kind=link}