The Two Headlines That Should Not Coexist

Two recent news developments create a paradox that every patient, doctor, and healthcare entrepreneur in India should examine closely.

- Item One: Over the past eighteen months, global private equity giants KKR, Blackstone, and TPG have poured nearly one billion dollars into Kerala’s hospital sector. KKR alone invested fifty-one billion rupees into Baby Memorial Hospital, acquiring approximately seventy-five percent control. KIMS, backed by OrbiMed and Ascent Capital, acquired Al Shifa Hospital for three billion rupees. The Economic Times and VCCircle have labeled this a gold rush, noting that Kerala’s long-standing model of doctor-led, family-run, community-trusted healthcare is being fundamentally reshaped.

- Item Two: On May twenty-two, two thousand twenty-six, economist Surjit Bhalla appeared on The Core Report with Govindraj Ethiraj to deliver what many have called a doomsday prediction about the Indian economy: collapsing consumption, stagnant real wages, a drying up of private investment, and exhausted government fiscal space. His core argument is that the bottom eighty percent of Indian households are in acute financial distress—a reality that will eventually drag down the broader macroeconomy.

The Paradox

If Bhalla is directionally correct—if the Indian middle class is financially buckling and broad-based consumption is shrinking—why are the world’s most sophisticated private equity funds racing to sell more expensive healthcare to that exact same population?

Are they delusional? Or is Bhalla looking at the wrong map?

This article tries to resolve that paradox by answering one foundational question: When private equity enters a healthcare system, who wins and who loses?

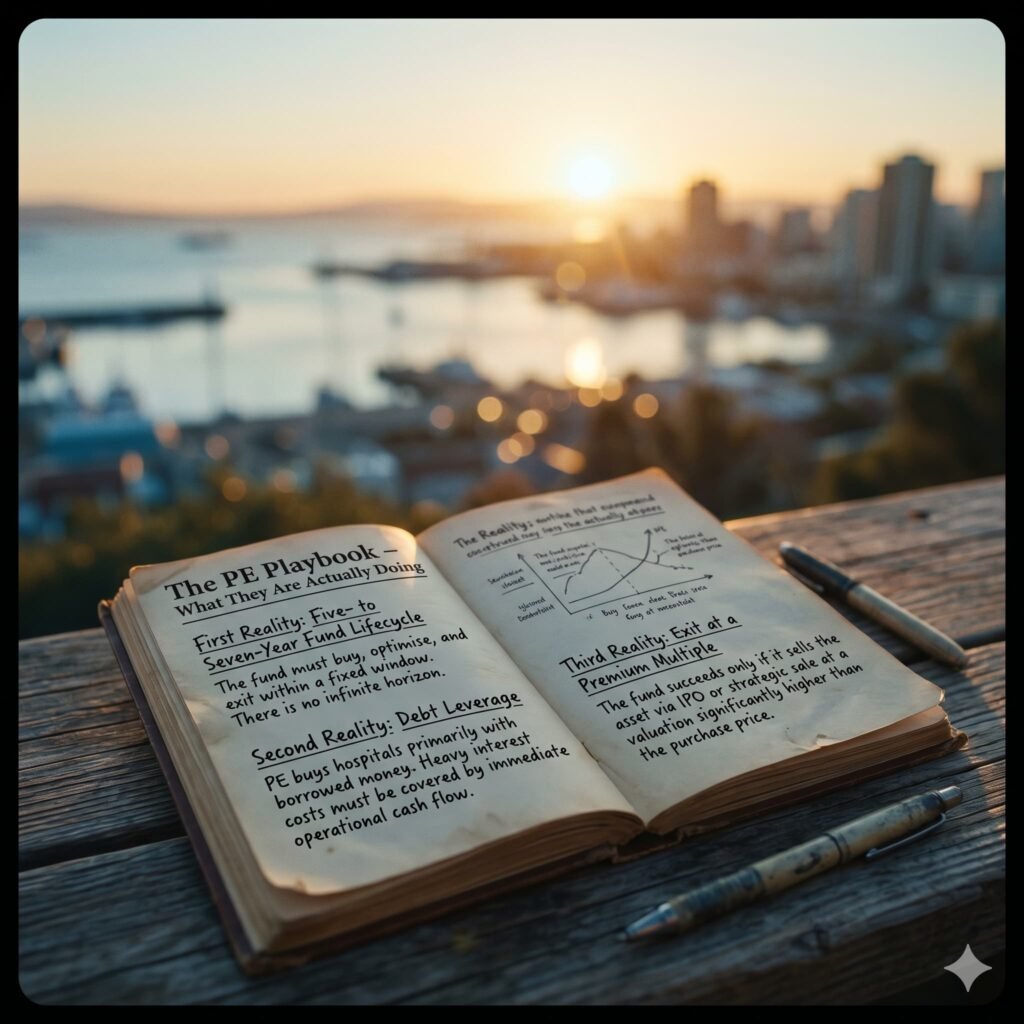

The PE Playbook – What They Are Actually Doing

To understand the shifting landscape of winners and losers, we must first look at the mechanics of the game. Private equity does not operate like a traditional, generational hospital chain. Its behavior is strictly dictated by three structural realities:

- First Reality: Five to Seven Year Fund Lifecycle

- Operational Implication: The fund must buy, optimize, and exit within a fixed window. There is no infinite horizon.

- Second Reality: Debt Leverage

- Operational Implication: PE buys hospitals primarily with borrowed money. Heavy interest costs must be covered by immediate operational cash flow.

- Third Reality: Exit at a Premium Multiple

- Operational Implication: The fund succeeds only if it sells the asset via IPO or strategic sale at a valuation significantly higher than the purchase price.

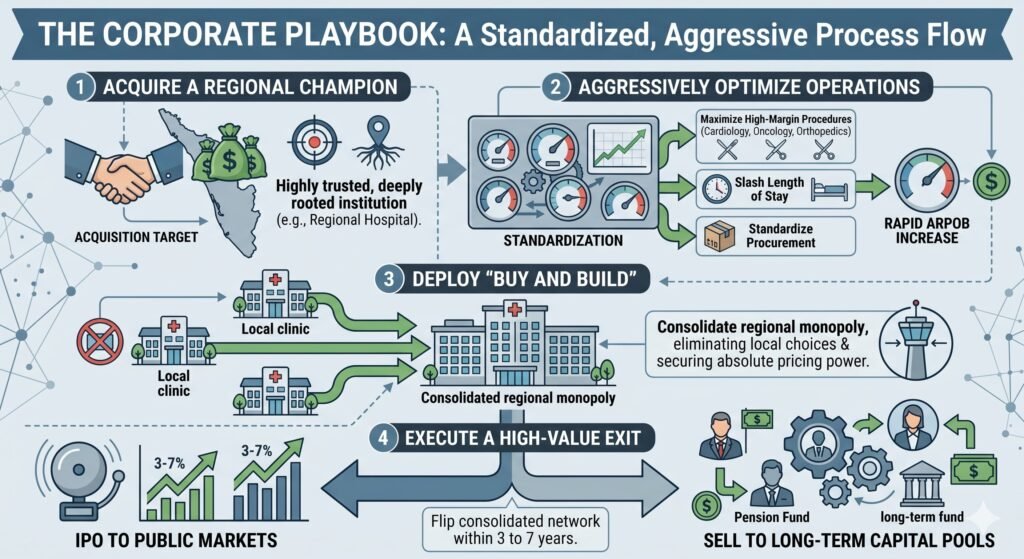

These structural guardrails manifest as a standardized, aggressive corporate playbook:

- Acquire a Regional Champion: Buy a highly trusted, deeply rooted institution such as Baby Memorial Hospital in Kozhikode.

- Aggressively Optimize Operations: Standardize procurement, slash length of stay, and maximize high-margin, asset-heavy procedures like cardiology, oncology, and orthopedics to rapidly increase Average Revenue Per Occupied Bed.

- Deploy “Buy and Build”: Acquire smaller local competitors to consolidate a regional monopoly, eliminating local choices and securing absolute pricing power.

- Execute a High-Value Exit: Flip the consolidated network within three to seven years to public markets via an IPO or sell to longer-term capital pools.

The Key Insight: Private equity does not need a booming economy or a prosperous middle class. It needs a defensive market where demand is entirely inelastic, and pricing power can be consolidated. Healthcare—specifically tertiary care for insured or desperate patients—is the ultimate inelastic market.

Who Wins?

1. Affluent, Insured Patients in the Short to Medium Term

For patients with top-tier corporate insurance or deep pockets, the immediate influx of capital brings undeniable upgrades. They gain immediate access to world-class medical infrastructure, including robotic surgery suites, advanced three-T MRI and PET-CT imaging, and twenty-four-seven cath labs.

Operational optimization means shorter wait times for diagnostics and streamlined bed turnover. Furthermore, standardized clinical protocols heavily reduce variable human errors and improve institutional infection control, while corporate branding seamlessly pulls in premium specialist talent.

A systematic review published in JAMA found that PE-acquired hospitals demonstrated significantly faster adoption of advanced medical technology compared to non-PE controls. For the patient capable of absorbing the premium cost, the clinical environment is genuinely superior. However, this gain comes with a clear expiration date: as the initial PE fund exits and flips the hospital to subsequent buyers, the intense pressure to sustain margins can cause the luxury patient experience to decay into rigid corporate box-checking.

2. Senior Doctors Who Sell Early

For the founding generation of physicians, a PE acquisition is an unparalleled liquidity event. A typical deal valuing a two-hundred-bed hospital at two to four billion rupees allows a founding doctor with a sixty per cent stake to walk away with one point two to two point four billion rupees in liquid wealth.

This structural shift completely removes the crushing operational burdens of modern medicine, such as managing payrolls, navigating volatile nursing shortages, and handling midnight regulatory compliance failures. Many selling doctors successfully transition into handsomely compensated brand ambassadors, retaining a small five to ten per cent equity sliver without carrying any of the underlying financial risk.

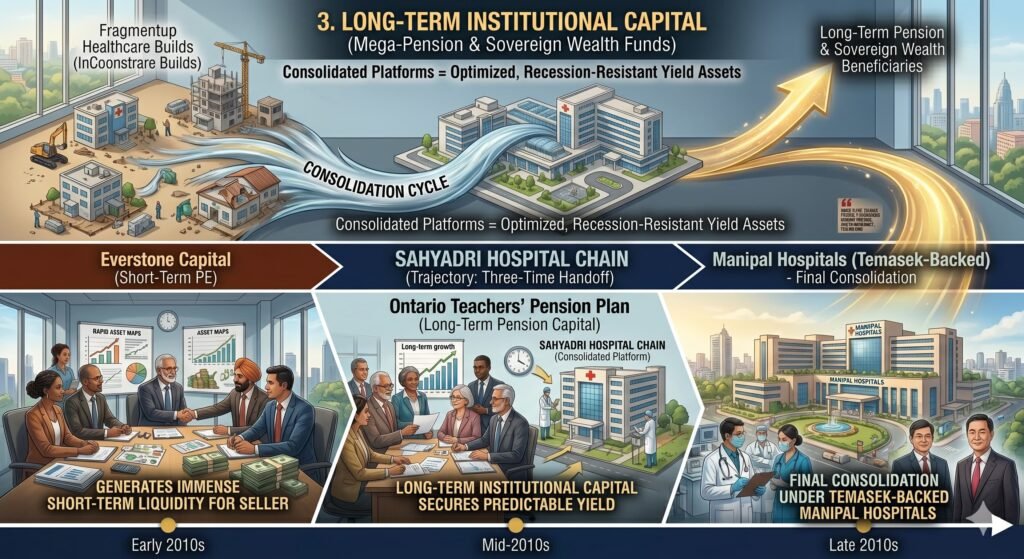

3. Long-Term Institutional Capital

Sovereign wealth funds and mega pension funds are the ultimate long-term beneficiaries of this consolidation cycle. They inherit mature, highly optimized, pre-consolidated hospital platforms from short-term PE funds, often at a distinct structural discount compared to pursuing fragmented, ground-up healthcare builds.

Consider the trajectory of the Sahyadri Hospital chain, which changed hands three times in less than a decade: from its original medical founders to Everstone Capital (short-term PE), moving onward to the Ontario Teachers’ Pension Plan (long-term pension capital), and ultimately consolidating under Temasek-backed Manipal Hospitals. Each evolutionary handoff generated immense liquidity for the short-term seller, while the long-term institutional capital secured a highly predictable, recession-resistant yield asset.

Who Loses?

1. Poor and Uninsured Patients

The collapse of the informal cross-subsidy model is the most devastating consequence of financialization. Historically, Kerala’s family-run nursing homes operated on an unwritten social contract: affluent patients were billed at full price, allowing the doctor-owner to subsidize or entirely waive costs for impoverished locals. Because the physician lived in the community, social capital and local reputation outweighed raw margin maximization.

Private equity operates under no such social contract. Every square foot of a hospital must hit explicit margin targets, and community charity is not a recognized line item. Consequently, the low-income population is systematically filtered out. They are either rerouted to already buckling public facilities, offered complex economy packages that remain far out of financial reach, or denied non-emergency secondary care entirely.

A comprehensive study in Health Affairs tracking PE-owned healthcare facilities revealed that charity care dropped by an average of twenty-eight percent following acquisition, while direct patient out-of-pocket costs surged by thirty-two percent. There is no structural reason to believe India’s trajectory will deviate from this data.

2. Independent Family Hospitals

The independent nursing homes that built Kerala’s exemplary health indicators are facing an existential pincer movement:

- Capital Disadvantages: Small hospitals cannot afford five hundred million rupees for new equipment.

- Talent Poaching: Specialists are drawn away by corporate salaries.

- Marketing Disadvantages: Small clinics are outspent by city-wide PE campaigns.

- Regulatory Burden: High overhead for legal compliance creates a severe strain.

Unable to match corporate scale, these local institutions are systematically drained of talent and patients. Most will eventually be forced to sell to corporate chains at highly depressed valuations, pivot to hyper-focused niches like low-margin palliative care, or shut their doors forever. This represents a catastrophic destruction of local social capital.

3. Junior and Salaried Doctors

Young physicians entering corporate healthcare are finding themselves trapped in a highly commoditized production line. While they receive stable, predictable salaries and protection from arbitrary local management, the trade-offs are steep:

- Erosion of Clinical Autonomy: Standardized, software-driven treatment pathways optimize efficiency but severely restrict a physician’s independent clinical judgment.

- Metricization of Care: Driven by revenue targets, average patient consultation times have shrunk from a meaningful ten to twelve minutes down to a rushed five to seven minutes.

- Accelerated Burnout: When the ancient art of healing is reduced to a performance dashboard metric, professional alienation spikes.

The early indicators of a silent exodus—where top young medical graduates actively abandon clinical practice for corporate roles in pharmaceuticals, insurance, and health tech—are now glaringly visible across PE-heavy zones.

4. Senior Doctors Who Sold (The Psychological Cost)

The emotional aftermath for physicians who cash out follows a remarkably consistent, painful arc. The initial elation of financial freedom quickly gives way to acute corporate friction. Simple, patient-centric decisions like hiring a trusted nurse or upgrading a piece of equipment suddenly require multilayered corporate approval from distant boards.

By the third year, many experience deep professional regret, realizing they have effectively become deskbound employees in institutions that still bear their family names.

As one former owner noted in The Ken: “I sold for eight hundred million rupees. I thought I had won. Now I sit in the same cabin, but the computer tells me how many patients I must see. The old me would have laughed.”

5. The Public Healthcare System and The Broader Economy

As private tiers aggressively scale their pricing, the public healthcare system faces a massive influx of displaced patients who have been priced out of private secondary and tertiary care. This creates an exponential volume surge across state facilities without a matching expansion in public budgetary allocations.

Simultaneously, political and civic attention shifts away from public health funding. Once the affluent, highly vocal middle class completely migrates to world-class corporate networks, the political necessity to maintain premium public hospitals disintegrates.

This directly connects back to Surjit Bhalla’s macroeconomic warnings. The two trends are not contradictory; they are perfectly symbiotic:

- Bhalla’s Warning 1: Consumption is collapsing for the bottom eighty percent.

- PE Calculation: We do not need the bottom eighty percent. Our financial models thrive solely on the top twenty percent who hold corporate insurance or asset wealth.

- Bhalla’s Warning 2: Private industrial investment is drying up.

- PE Calculation: We are not investing in risk-heavy greenfield capacity. We are buying up and consolidating existing local monopolies.

- Bhalla’s Warning 3: Government fiscal space is totally exhausted.

- PE Calculation: This ensures public healthcare infrastructure will degrade systematically, driving desperate patients into our networks.

- Bhalla’s Warning 4: Real wages are flatlining across the board.

- PE Calculation: Healthcare is completely income inelastic. A family will defer buying a car or a home, but they will liquidate assets to pay for a bypass surgery.

The uncomfortable systemic reality is that private equity is not betting on India’s widespread economic prosperity. They are monetizing its structural desperation.

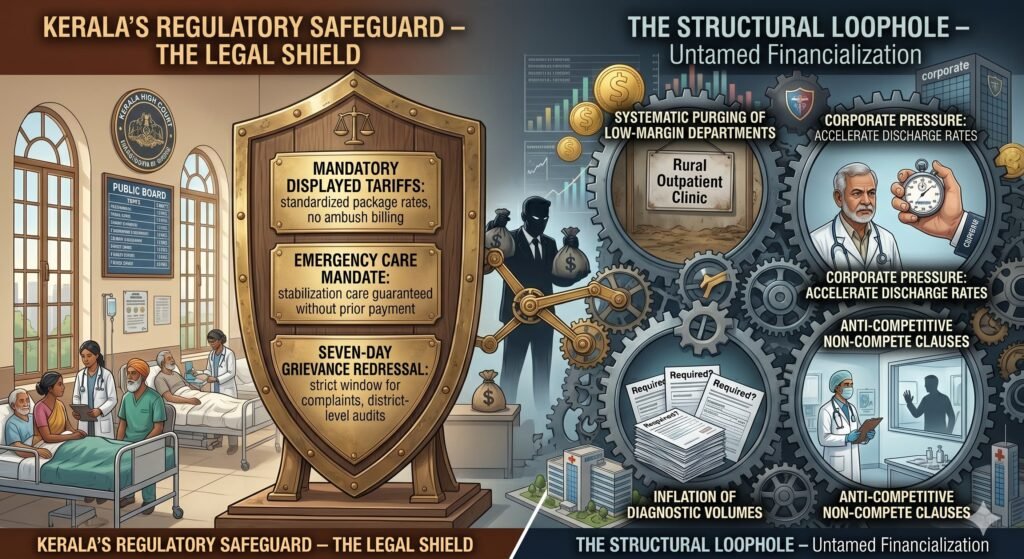

The Regulatory Safeguard – Kerala’s Legal Shield

Kerala’s regulatory landscape possesses distinct legal mechanisms to counter untamed financialization. The Kerala Clinical Establishments Act of two thousand eighteen, decisively upheld by the Kerala High Court, establishes clear operational guardrails:

- Mandatory Displayed Tariffs: Every medical institution must publicly publish standardized package rates. Ambush billing and opaque pricing schedules are legally restricted.

- Emergency Care Mandate: No hospital can legally deny life-saving stabilization care based on a patient’s inability to pay up front.

- Seven-Day Grievance Redressal: Patient complaints must be addressed within a strict one-week window, backed by independent district-level medical audits.

The Structural Loophole

While these laws are vital, they only regulate transparency and immediate crisis management. They are structurally blind to the hidden levers of corporate financialization, such as the systematic purging of low-margin medical departments, corporate pressure to accelerate patient discharge rates, the inflation of diagnostic volumes, and anti-competitive non-compete clauses that lock doctors out of local practices.

Furthermore, regulatory capture remains a permanent threat. Historical precedent suggests that cash-rich global funds possess the legal and political leverage to blunt enforcement in ways small, local nursing homes never could.

Part Five: The Ultimate Winner-Loser Matrix

| Group | Gains | Losses | Verdict |

| Affluent, Insured Patients | Immediate tech upgrades and standardized clinical protocols | Aggressive defensive diagnostics and highly clinical, impersonal care | Mixed short-term operational win; long-term cost caution |

| Poor & Uninsured Patients | Base-level emergency stabilization legally guaranteed | Total loss of cross-subsidy and systematic exclusion from non-emergency care | Clear Loss with severe healthcare marginalization |

| Senior Doctors (Sellers) | Massive liquidity events and complete removal of business risks | Absolute loss of clinical autonomy and severe corporate seller’s regret | Financial Win joined with Professional Loss |

| Junior Salaried Doctors | Highly stable pay scales and structured corporate career paths | Punitive productivity quotas with rapid clinical alienation and burnout | Dependent on individual priorities |

| Small Family Hospitals | None | Severe talent poaching alongside absolute capital and marketing obsolescence | Clear Loss resulting in existential erasure |

| Private Equity Funds | Consistent eighteen to twenty-five percent internal rate of return and massive fee generation | Local reputational backlashes and shifting regulatory compliance costs | Clear Corporate Win |

| Public Health Infrastructure | None | Extreme volume displacement and total loss of middle-class political advocacy | Systemic Loss with deepening structural neglect |

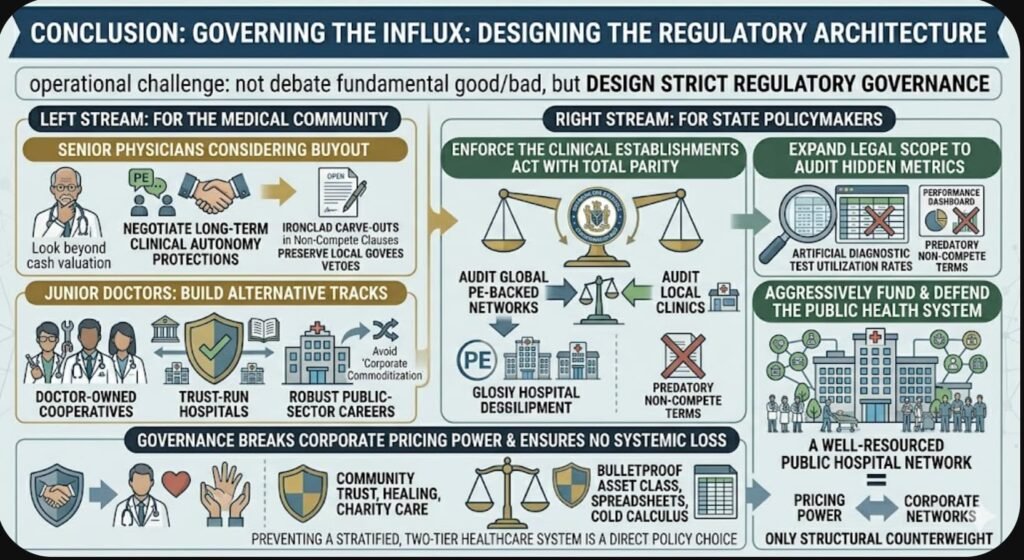

Conclusion: Governing the Influx

Private equity capital cannot be simply wished away; the capital allocations are locked, the acquisitions are legally binding, and market consolidation will accelerate. The operational challenge moving forward is not debating whether PE is fundamentally good or bad, but designing strict regulatory architecture to govern it.

For the Medical Community

Physicians considering a corporate buyout must look beyond the immediate cash valuation. They must explicitly negotiate long-term protections for clinical autonomy, secure ironclad carve-outs in non-compete clauses, and preserve local governance vetoes.

Junior doctors must actively support and build alternative practice tracks—including doctor-owned cooperatives, trust-run hospitals, and robust public-sector careers—to avoid total corporate commoditization.

For State Policymakers

Regulatory bodies must enforce the Clinical Establishments Act with complete structural parity, auditing global PE-backed hospital networks with the exact same rigor applied to vulnerable local clinics. Crucially, the legal scope of the Act must expand to audit hidden profit-driving metrics, specifically artificial diagnostic test utilization rates and predatory non-compete terms.

Most importantly, the state must aggressively fund and defend the public healthcare system. A well-resourced public hospital network is the only structural counterweight capable of breaking corporate pricing power. Preventing a highly stratified, two-tier healthcare system is not an economic impossibility; it remains a direct policy choice.

Private equity is operating on the cold calculus that healthcare remains the ultimate bulletproof asset class in a fracturing economy. They are not intentionally malevolent; they are simply structurally indifferent to any human metric that cannot be rendered on a spreadsheet. Healing, community trust, and medical charity do not show up on financial dashboards. That remains the profound systemic loss that no internal rate of return can ever capture.

Sources:

- VCCircle (April 2026): PE-backed KIMS acquires majority stake in Al Shifa Hospital in Kerala. Documented the three billion rupee enterprise valuation and the corporate strategy targeting consolidation across Northern Kerala.

- Digital Health News (April 2026): KKR Invests an Additional 1,751 Crore Rupees (seventy five percent stake equivalent) in Kerala’s Baby Memorial Hospital. Verified KKR’s scaled cumulative commitment of fifty-one billion rupees, locking down a seventy-five percent controlling interest.

- The Economic Times (May 2023): Blackstone signs binding pact for controlling stake in Care Hospitals. Provided foundational valuation baselines of around eight hundred million dollars for global PE fund entry strategies into Indian multi-specialty ecosystems.

- The Core Report (May 22, 2026): Surjit Bhalla Explains What Is Really Wrong With India Economy. Govindraj Ethiraj, interviewer. Primary source for Bhalla’s macroeconomic thesis outlining the collapse of bottom eighty percent consumption patterns and stagnant real wages.

- BW Legal World (November 2025): Kerala HC Upholds Clinical Establishments Act. Primary legal record of the High Court judgment validating mandated tariff displays and immediate emergency stabilization without up-front financial blocks.

- JAMA (2023): Private Equity Acquisition of Hospitals and Patient Outcomes. A comprehensive systematic review detailing accelerated technological capital expenditures alongside increased systemic costs post-acquisition.

- Health Affairs (2022): Changes in Charity Care and Patient Out-of-Pocket Costs Following Private Equity Acquisition of Hospitals. Provided empirical baseline data documenting the twenty-eight percent contraction in uncompensated charity care alongside a thirty-two percent rise in out-of-pocket patient financial burdens.

- The Ken and Business Standard (2024 to 2025): Multiple qualitative deep dives and anonymous interviews with primary hospital founders across India detailing operational friction, metric-driven clinical structures, and post-sale professional alienation.

{kind=link}