Dilip Shanghvi didn’t begin in a lab or inherit a pharmaceutical empire. In the late 1970s, he helped his father distribute generic medicines as a wholesale distributor in Kolkata. Decades later, he sits atop Sun Pharmaceutical Industries Ltd., the company that turned opportunistic acquisitions and painstaking regulatory work into predictable engines of growth. The lesson is simple and ruthless: buy problems cheaply, fix them methodically, and extract long-term value.

Sun Pharma’s playbook is repeatable and has been executed with precision: distressed asset → acquisition during regulatory/financial crisis → operational remediation → market consolidation and cash generation. Four landmark deals show how the strategy evolved from simple generics to specialized therapies, culminating in an unprecedented global move.

The Deal History: Evolution of the Playbook

Taro: Buying America’s Cash Engine

Taro Pharmaceuticals was a profitable U.S.-listed generic and dermatology player with roots in Israel. Between the mid-2000s and 2010s, it suffered promoter fights, delayed financial filings, and investor distrust, making it a prime takeover target. Sun Pharma initiated a bid in 2007. After prolonged litigation and multi-jurisdictional negotiations, Sun secured a controlling interest in September 2010. Demonstrating Shanghvi’s signature multi-decade patience, Sun steadily managed the asset before acquiring all remaining public shares and fully privatizing Taro in June 2024. The asset became a steady U.S. dermatology cash engine that financed later strategic pivots.

Ranbaxy: Remediation at Scale

Ranbaxy’s collapse is the ultimate case study for opportunistic buyers. After Daiichi Sankyo acquired Ranbaxy in 2008, the company faced catastrophic U.S. FDA compliance failures, including import alerts and data-integrity issues that crippled exports. By 2014, Daiichi wanted an exit. Sun Pharma stepped in with an all-stock transaction valued at $4 billion, using its own highly valued equity to absorb Daiichi’s operational headache without draining cash reserves. The merger, completed in March 2015, created the largest pharmaceutical company in India by revenue. Turning Ranbaxy around required years of intensive regulatory remediation and plant upgrades, but it ultimately delivered a dominant domestic market share and vast manufacturing capacity that Sun optimally redeployed.

Recent Specialty Moves (2023–2025): Building the Bridge

As simple generics in the U.S. faced severe deflationary pricing pressure, Sun shifted capital toward branded specialty assets protected by patents.

- Concert Pharmaceuticals (2023): Sun acquired Concert for approximately $576 million in cash, gaining Leqselvi (deuruxolitinib), an oral JAK inhibitor for alopecia areata.

- Checkpoint Therapeutics (May 2025): Sun completed the acquisition of Checkpoint for an upfront cash payment of $4.10 per share (approximately $355 million upfront) plus contingent value rights (CVRs). The transaction added UNLOXCYT (cosibelimab), an FDA-approved anti–PD-L1 monoclonal antibody for advanced cutaneous squamous cell carcinoma, into Sun’s high-growth onco-dermatology pipeline.

These transactions served as vital commercial practice runs for the massive specialty scale that followed.

The Organon Transaction: The Ultimate Culmination (2026)

On April 26, 2026, Sun Pharma announced its largest and most transformative transaction: a definitive agreement to acquire U.S.-based Organon & Co.

Under the terms, Sun will pay $14.00 per share for all outstanding stock in an all-cash offer to Organon shareholders. The offer represents a premium of 103% to Organon’s unaffected share price. The transaction carries a total enterprise valuation of $11.75 billion due to Organon’s substantial legacy debt. Sun plans to fund the deal using available balance sheet cash ($2.0–$2.5 billion) and committed bank financing ($9.25–$9.75 billion).

Spun off from Merck in 2021, Organon possessed strong underlying assets but faced growth bottlenecks from its debt load. The deal is projected to propel Sun Pharma into the top 25 global pharmaceutical players, with combined pro forma revenue of $12.4 billion. The transaction gives Sun an immediate top-three global position in women’s health, a robust established brands portfolio, and entry into the global biosimilars market as a top-10 player.

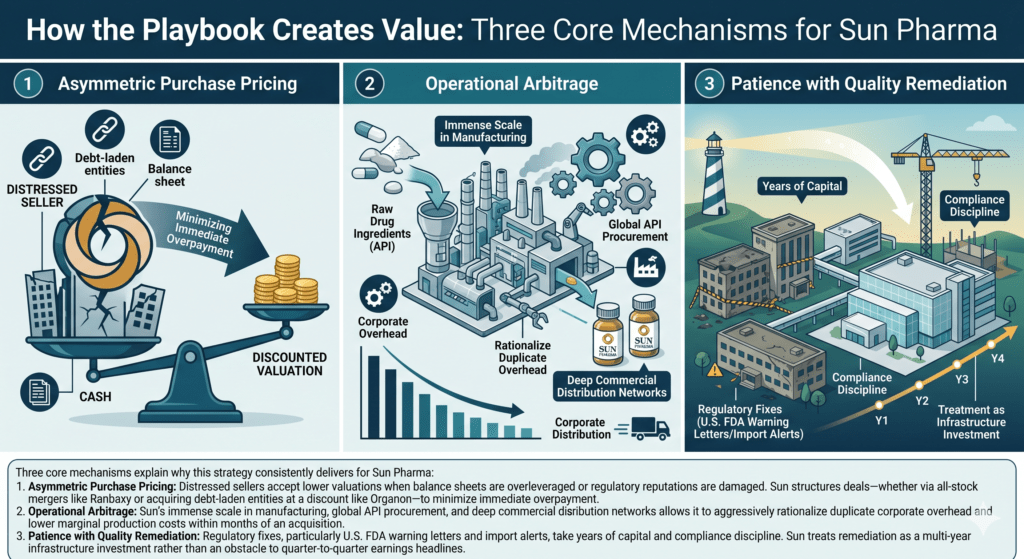

How the Playbook Creates Value

Three core mechanisms explain why this strategy consistently delivers for Sun Pharma:

1. Asymmetric Purchase Pricing: Distressed sellers accept lower valuations when balance sheets are overleveraged or regulatory reputations are damaged. Sun structures deals—whether via all-stock mergers like Ranbaxy or acquiring debt-laden entities at a discount like Organon—to minimize immediate overpayment.

2. Operational Arbitrage: Sun’s immense scale in manufacturing, global API procurement, and deep commercial distribution networks allows it to aggressively rationalize duplicate corporate overhead and lower marginal production costs within months of an acquisition.

3. Patience with Quality Remediation: Regulatory fixes, particularly U.S. FDA warning letters and import alerts, take years of capital and compliance discipline. Sun treats remediation as a multi-year infrastructure investment rather than an obstacle to quarter-to-quarter earnings headlines.

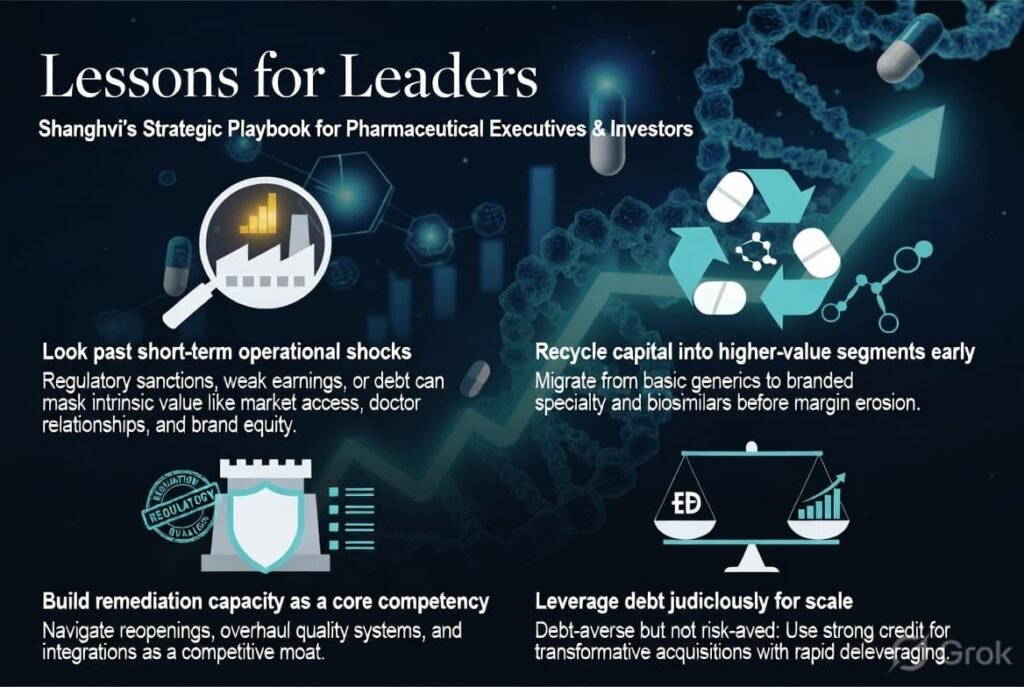

Lessons for Leaders

For pharmaceutical executives and industrial investors, Shanghvi’s method offers clear strategic takeaways:

- Look past short-term operational shocks: Regulatory sanctions, weak quarterly earnings, or heavy inherited debt can temporarily mask intrinsic commercial value such as market access, trusted doctor relationships, and established brand equity.

- Recycle capital into higher-value segments early: Sun’s systematic migration from basic generics to branded specialty dermatology, oncology, and biosimilars illustrates how to anticipate secular margin erosion and pivot capital before structural decline sets in.

- Build remediation capacity as a core corporate competency: The internal capability to navigate regulatory reopenings, overhaul quality-management systems, and execute cross-border integrations is a massive competitive moat. It deters more timid peers and opens exclusive acquisition pipelines.

- Leverage debt judiciously for generational scale: Shanghvi has frequently described himself as “debt-averse, not risk-averse.” While the Organon deal represents a major departure from Sun’s historically debt-free balance sheet, it leverages a strong credit profile to secure bank financing for an asset projected to nearly double Sun’s cash and EBITDA generation, enabling rapid post-transaction deleveraging.

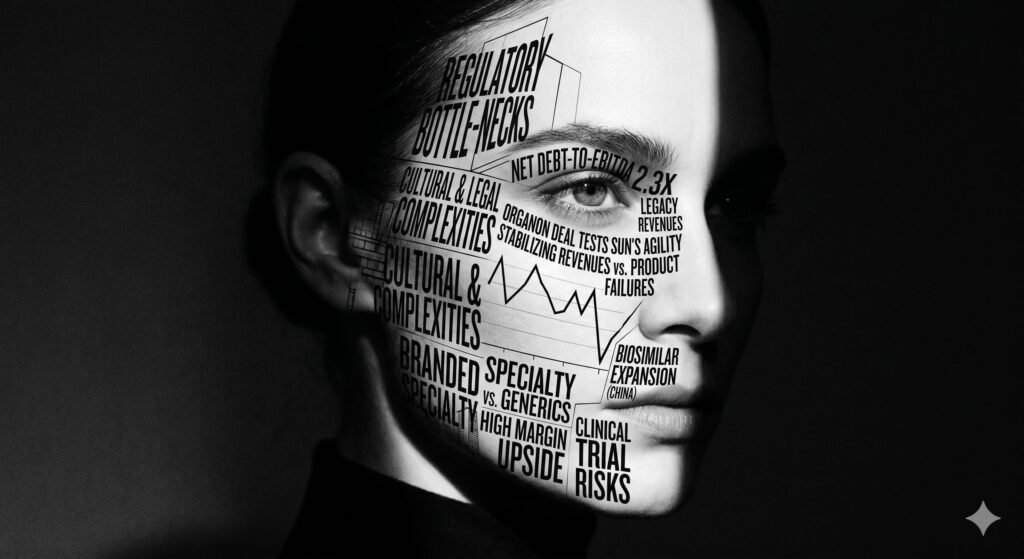

Caveats and Risks

The playbook is not risk-free. Regulatory remediation can hit unexpected bottlenecks, and multi-billion-dollar cross-border integrations introduce severe cultural and legal complexities.

With a post-transaction net debt-to-EBITDA ratio projected at 2.3x, the Organon deal tests Sun’s financial agility. Success hinges on stabilizing legacy women’s health revenues, expanding the biosimilar commercial footprint in key markets like China, and realizing targeted operational synergies. Operating heavily in branded specialty drugs also brings clinical trial, R&D, and high-intensity marketing risks that differ fundamentally from the low-overhead generics business—offering much higher margin upside but introducing the potential for expensive product failures.

Appendix — Fact-Check Notes and Primary Sources

- Sun Pharma — Organon & Co. Acquisition Announcement (April 26, 2026): Definitive agreement for an all-cash transaction at $14.00 per share; total enterprise valuation of $11.75 billion. Combined pro forma revenue estimated at $12.4 billion, positioning the combined entity in the top 25 globally and top 10 in biosimilars. Net debt-to-EBITDA projected at 2.3x. Sources: Sun Pharma Official Regulatory Filings (NSE/BSE), Organon & Co. Investor Relations Disclosure (April 2026), and The Hindu (Business/Industry, April 27, 2026).

- Sun Pharma — Checkpoint Therapeutics Acquisition (March–May 2025): Definitive acquisition agreement announced March 9, 2025, completed May 30, 2025. Consideration structured as upfront cash of $4.10 per share (approx. $355 million) plus non-transferable CVRs. Acquired full rights to FDA-approved anti-PD-L1 antibody UNLOXCYT (cosibelimab). Sources: Sun Pharma Press Release Archive (May 2025) and Checkpoint Therapeutics Corporate Closing Disclosures.

- Sun Pharma — Taro Pharmaceutical Industries Privatization Timeline (2007–2024): Initial takeover attempt in 2007; operational control gained September 2010. January 17, 2024: definitive merger agreement to buy all remaining minority shares at $43.00 per share in cash. Merger completed and Taro delisted from NYSE in June 2024. Sources: Taro SEC Schedule 13E-3 Filings and Sun Pharma Investor Presentations (H1 2024).

- Sun Pharma — Ranbaxy Laboratories Merger (2014–2015): All-stock transaction valued at approximately $4 billion, announced April 2014, concluded March 2015. Ranbaxy shareholders received 0.8 shares of Sun Pharma for every 1 share held. Sources: Sun Pharmaceutical Industries Ltd. Scheme of Arrangement Documentation and BSE/NSE Merger Archives.

- Sun Pharma — Concert Pharmaceuticals Acquisition (2023): Cash transaction of approximately $576 million enterprise value completed in early 2023, adding deuruxolitinib (Leqselvi) to the specialty dermatology framework. Sources: Sun Pharma Corporate Press Releases (January/March 2023).

All Images are AI Generated for Illustration Only. E&OE

Editor’s Note: I had the privilege of watching Sun Pharma from the early 1990s in Baroda, when I moved from Pharma to medical publishing. Baroda and Ahmedabad-based pharma companies were early adopters of a wide range of medical communications to reach a broader audience of doctors, including readers of over a dozen periodicals and the patient information leaflets we produced.

Baroda was then the capital of Indian Pharma with giants like Alembic and Sarabhai, and Ahmedabad was full of enterprising companies that are now the market leaders.

What was remarkable about the pharma companies in Baroda and Ahmedabad was that they were absolutely easy to approach and partner with to create some of the finest work I accomplished in medical communications.

{kind=link}