India’s pharmaceutical retail landscape remains one of the world’s largest and most fragmented, dominated by traditional brick-and-mortar chemists. Yet, the online (e-pharmacy) segment is steadily carving out a larger role, driven by digital adoption, omnichannel strategies, and evolving consumer expectations. As of mid-2026, e-pharmacies represent a small but high-growth slice of the total retail pharmacy market.

Market Size and Penetration

The Indian online pharmacy market was valued at approximately USD 3.71 billion in 2025, with projections to reach USD 14.08 billion by 2034, growing at a CAGR of 15.98% (2026–2034).

The broader Indian retail pharmacy market (encompassing both organised and unorganised physical outlets, as well as digital channels) is estimated at around USD 24–27 billion in recent assessments. This puts the online segment’s current penetration at roughly 5–7% of organised/visible retail pharmacy sales, with some reports citing around 5% for organised e-pharmacy within the overall retail ecosystem as of 2025.

For context:

- The wider Indian pharmaceutical market (including manufacturing and exports) stands at approximately USD 57–60 billion domestically in 2025–2026.

- Unorganized independent pharmacies still dominate, accounting for the vast majority of outlets (historically ~85–90%), which keeps overall digital penetration modest compared to categories like groceries or electronics.

This represents meaningful progress from pre-COVID levels (often estimated at 1–3%), but the sector has significant headroom, especially as organized retail chains and e-pharmacies expand.

Competitive Landscape

The online space is increasingly consolidated among a few major players backed by large conglomerates:

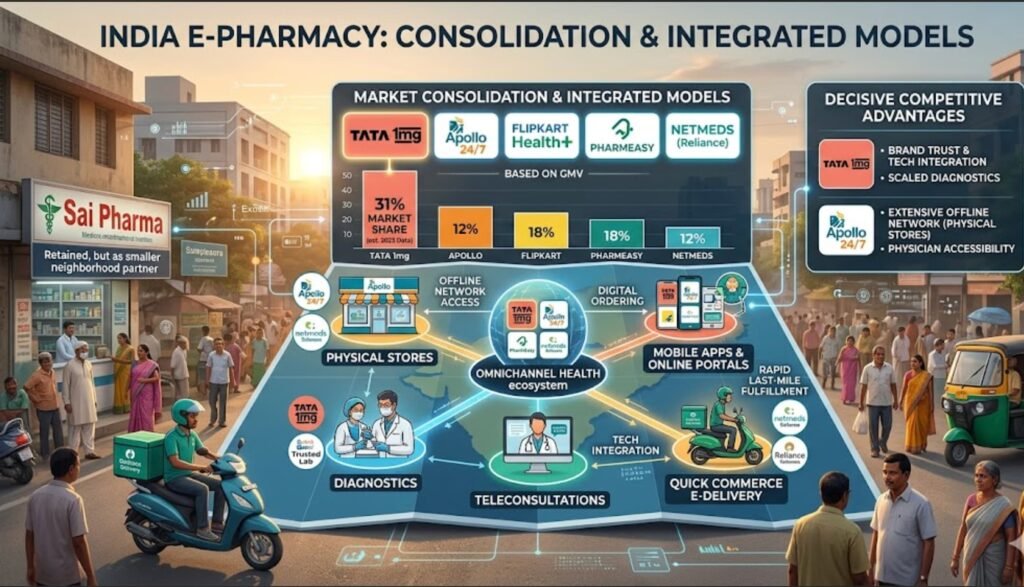

- Tata 1mg continues to lead with approximately 31% market share (GMV basis, based on 2023 Redseer data still widely referenced).

- Apollo 24/7, Flipkart Health+, PharmEasy, and Netmeds (Reliance) follow, each holding significant double-digit shares in the organized online segment.

Omnichannel models—combining physical stores, apps, diagnostics, and teleconsultations—are proving decisive. Apollo benefits from its extensive offline network, while Tata 1mg leverages brand trust and tech integration.

Quick commerce entrants like Zepto are also intensifying competition with ultra-fast medicine delivery in select cities.

Key Growth Drivers

- Rising Chronic Disease Burden and Convenience: Diabetes, hypertension, and wellness products (OTC) drive repeat online orders.

- Digital Infrastructure: High smartphone penetration, UPI payments, and improved logistics.

- Post-Pandemic Habits: Consumer comfort with online health services persists.

- Policy and Investment Support: Government digital health initiatives and continued investor interest in health-tech.

Challenges and Headwinds

- Regulatory Scrutiny: Strict norms on prescription drugs, licensing, and advertising create compliance hurdles and limit pure-play models.

- Trust and Quality Concerns: Fears of counterfeits favor established local chemists in many regions.

- Fragmented Geography: Rural and Tier-3/4 areas lag due to logistics and digital literacy gaps.

- Profitability Pressures: Heavy discounting and high customer acquisition costs have challenged many players, leading to restructuring (e.g., PharmEasy).

The unorganized sector’s resilience remains the biggest barrier to faster digital penetration.

Outlook

Analysts expect the e-pharmacy segment to grow at 16–20% annually in the near term, potentially reaching 10–15% penetration of retail pharmacy sales by 2030–2032 if regulatory clarity improves and omnichannel models scale effectively.

For the pharma industry—particularly field force professionals—this shift implies evolving roles: from traditional detailing to supporting hybrid models, educating on digital platforms, and ensuring compliance in a more transparent, consumer-driven market.

Conclusion: While online pharmacies still represent a single-digit percentage of India’s massive retail pharma market, their trajectory is firmly upward. The winners will be those who blend digital convenience with the trust and accessibility of traditional retail. As India’s healthcare digitizes, e-pharmacies are not just a channel—they are catalysts for greater transparency, efficiency, and patient-centric care.

Appendix: Key Sources

- IMARC Group – India Online Pharmacy Market Outlook 2034.

- Credence Research – India Retail Pharmacy Market Report.

- Nexdigm – India Pharmacy Retail Market Outlook to 2030.

- Pharmabiz / Tata 1mg statements on ePharmacy growth (2025).

- Business Standard / Redseer – Market share data (2023, still referenced).

- IBEF and Mordor Intelligence – Broader Indian Pharma Market.

- Various industry reports from Fortune Business Insights, Coherent Market Insights, and LinkedIn analyses (2025–2026).

This article is based on publicly available market research as of June 2026. Market figures can vary by source due to differences in scope (GMV vs. revenue, organized vs. total). For the latest primary data, consult specialized firms like Redseer or IMARC.

{kind=link}