India’s next healthcare opportunity may not be in the metros

The Rs 4,326 crore Mankind Pharma IPO of 2023 was not just another pharmaceutical listing. It was a referendum on a simple but powerful idea: India’s growth story lives in its small cities.

By focusing on Tier-2 and Tier-3 markets, building deep relationships with general practitioners, maintaining affordable pricing, and creating strong consumer trust, Mankind built one of the country’s most successful healthcare franchises. The company entered the public markets with revenue of approximately Rs 8,749 crore and earnings before interest, taxes, depreciation, and amortisation (EBITDA) of roughly Rs 1,913 crore.

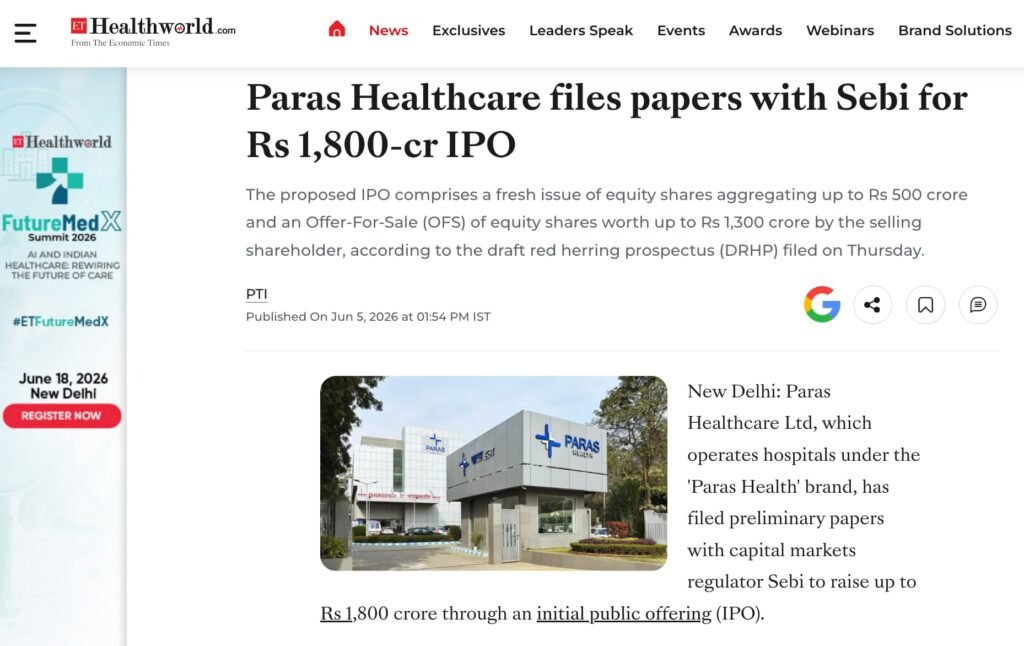

Now, Paras Health, the operator of the Paras Health hospital network, has refiled its draft red herring prospectus (DRHP) with the Securities and Exchange Board of India (Sebi) for an initial public offering (IPO) of approximately Rs 1,800 crore. The offering comprises a Rs 500 crore fresh issue and a Rs 1,300 crore offer-for-sale (OFS).

The comparison with Mankind is not perfect. One is a pharmaceutical company. The other is a hospital operator. Their economies are fundamentally different. Yet the strategic question is intriguing: Can Paras Health build the hospital equivalent of Mankind Pharma’s Bharat-focused healthcare playbook? The answer may reveal much about the future of organised healthcare delivery in India. The hidden advantage: a trusted name in every home

Before examining the hospital chain’s numbers, one critical fact deserves attention. Paras, through its over-the-counter (OTC) medications range, is already a highly trusted name with deep penetration in the very markets where it is building hospitals.

For decades, products such as Paras Lotion for ringworm, Lemolate for cold and cough, and various other OTC remedies have been staples in Indian households, particularly in North and East India. The brand has earned trust through generations of use. A grandmother in Darbhanga who used Paras Lotion is likely to trust Paras Hospital for her granddaughter’s fever.

This existing brand equity has a direct and measurable bearing on patient acquisition. Most hospital chains spend heavily on marketing, doctor referrals, and brand building to attract patients to a new facility. Paras starts with a significant advantage: its name is already recognised and trusted. The cost of acquiring a patient is likely lower, and the ease of conversion is likely higher, than for a competitor entering the same market without this household presence.

This is an advantage no other hospital chain in India can claim. Apollo, Max, Narayana Health, and Fortis have built their brands through decades of clinical excellence. Paras has built its brand through pharmacy shelves. The question is whether that trust transfers from a Rs 50 lotion to a Rs 50,000 hospital admission.

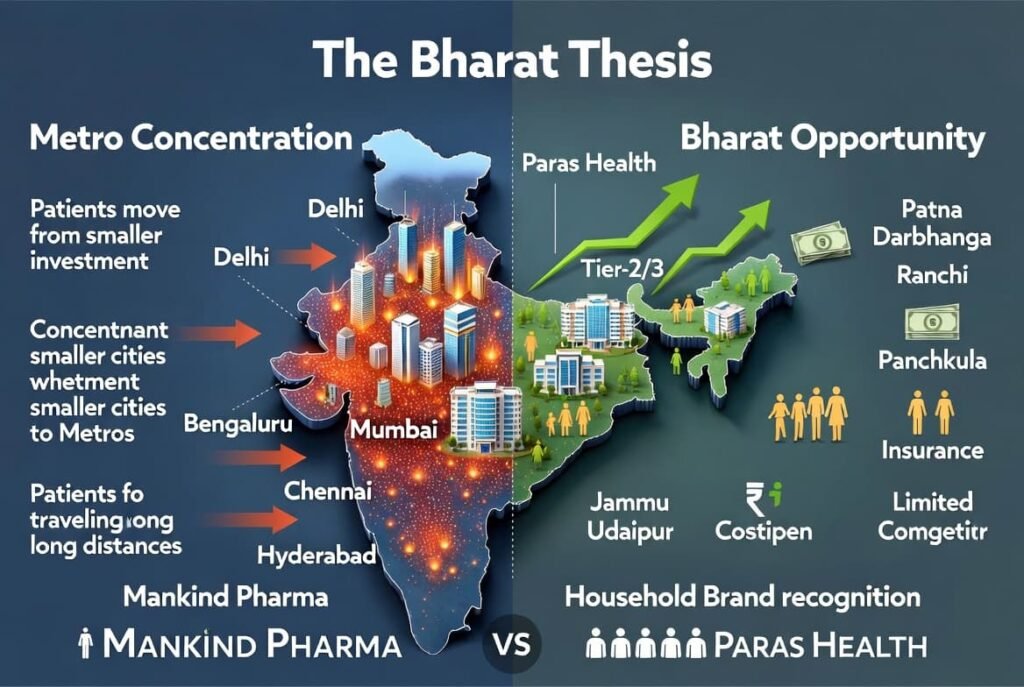

The Bharat Thesis

For decades, India’s organised healthcare infrastructure has remained concentrated in major metropolitan centres. Cities such as Delhi, Mumbai, Bengaluru, Chennai and Hyderabad attracted disproportionate investment in tertiary and quaternary healthcare facilities. Meanwhile, millions of patients in smaller cities continued travelling long distances for specialised care.

Paras Health has chosen a different path.

Its network has been built around markets such as Patna, Darbhanga, Ranchi, Panchkula, Jammu and Udaipur. These are not India’s largest healthcare markets, but they are regions where rising incomes, increasing health awareness, expanding insurance coverage, and limited organised competition create significant opportunities. Crucially, these are also the markets where the Paras OTC brand enjoys its deepest penetration.

This strategic positioning bears resemblance to Mankind Pharma’s early expansion model. Rather than fighting entrenched competitors in overcrowded metropolitan markets, both organisations sought growth where healthcare demand was rising faster than organised supply. Mankind had its distribution network. Paras has its household brand recognition.

Similar strategy, different economics

The similarities between Mankind and Paras are real, but investors must also recognise the critical differences. Mankind operates an asset-light pharmaceutical business. Paras operates an asset-heavy hospital business. Mankind’s products can be distributed nationally with relatively limited incremental capital. Hospitals require land, buildings, equipment, specialists, nurses, and years of operational maturity before optimal returns emerge. Mankind’s growth model benefited from scalable manufacturing and extensive distribution. Paras must depend on occupancy levels, clinical outcomes, and efficient utilisation of physical assets.

However, there is one similarity that investors should not underestimate. Mankind’s deep distribution network gave it a cost advantage in reaching India’s small cities. Paras’s deep OTC brand penetration gives it a patient acquisition cost advantage in exactly those same cities. In healthcare, where marketing expenses can consume 5 to 10 per cent of revenue for a new hospital, this advantage is not trivial.

As a result, Paras should not be viewed as the next Mankind. But it may be viewed as a hospital chain with a unique, non-replicable marketing asset.

The numbers: is the foundation strong enough?

Based on FY25 disclosures and IPO-related filings, Paras Health reported revenue from operations of approximately Rs 1,294 crore and EBITDA of Rs 156.5 crore. The company currently operates around 2,135 beds across its network and remains focused primarily on North and East India.

Note: The company’s subsequently filed DRHP for June 2026 indicates stronger FY26 performance, with revenue of Rs 1,605.9 crore and EBITDA of Rs 335.6 crore. Readers should verify all data against the latest prospectus and audited financial statements.

By comparison, Mankind Pharma entered the public markets in 2023 as a mature cash-generating enterprise. Paras arrives after a turnaround phase, with improving financial performance but a balance sheet that still requires deleveraging.

This distinction does not weaken the investment thesis, but it does alter the risk profile.

Why occupancy matters more than revenue

Many hospital IPO discussions focus on revenue growth. The more important metric is occupancy.

Hospital economics are driven by four key variables:

Occupancy rate

Average revenue per occupied bed (ARPOB)

Average length of stay (ALOS)

EBITDA per operational bed

Paras reported occupancy levels approaching 66 per cent in its mature facilities. For context, this compares to approximately 65-70 per cent for Apollo Hospitals, 75-80 per cent for Max Healthcare, and 70-75 per cent for Narayana Health. The company has also improved ARPOB to approximately Rs 47,668.

At 66 per cent, Paras’s mature facility occupancy trails industry leaders like Max Healthcare but compares favourably to regional peers and indicates room for operating leverage improvement.

This matters because hospitals carry substantial fixed costs regardless of patient volume. Once occupancy crosses certain thresholds, operating leverage improves rapidly and profitability can expand disproportionately. For Paras, sustained occupancy improvement may ultimately prove more important than headline revenue growth. And here, the OTC brand advantage could play a role. A trusted household name may help fill beds faster than a new entrant with no prior brand presence.

The OFS component: what the exits signal

The IPO includes a significant offer for sale component of Rs 1,300 crore. Promoter Dharminder Kumar Nagar is partially selling shares worth Rs 300 crore. More notably, financial sponsors Commelina Ltd. is selling shares worth Rs 800 crore, while the 360 ONE Special Opportunities Fund is selling shares worth Rs 200 crore.

The large OFS component warrants investor attention. While promoters are partially selling, the more significant exits by financial sponsors suggest these investors believe current valuations are attractive for selling. This is not unusual in healthcare IPOs, but it does shift the near-term shareholder base from long-term private equity holders to public market investors with potentially shorter time horizons.

The 800-bed expansion bet – The most consequential aspect of the IPO story is expansion.

Paras plans to add approximately 800 beds through a 300-bed facility in Gurugram and a 500-bed facility in Ludhiana. This could increase total capacity from the current 2,211 beds to approximately 3,011 beds by FY29.

Ludhiana aligns closely with the company’s Bharat-focused strategy. It serves a large industrial and agricultural catchment area with growing demand for advanced healthcare services. The Paras OTC brand is well known in Punjab, which may accelerate patient trust and occupancy ramp-up at the new facility. However, in Ludhiana, Paras will compete with the existing presence of Dayanand Medical College and Hospital (DMCH) and the operations of Mohan Dai Oswal Hospital.

Gurugram presents a different challenge. Unlike Paras’s traditional markets, Gurugram is one of India’s most competitive healthcare ecosystems. The competitive set includes Artemis Hospital, Medanta’s Sohna Road facility, and Max Healthcare’s upcoming 500-bed expansion. Here, the OTC brand advantage is less pronounced. Urban Gurugram patients may not associate Paras with tertiary care, even if they recognise the name from household products.

Success in Gurugram would demonstrate Paras’s ability to compete beyond underserved regional markets. Failure could pressure returns on invested capital. The project, therefore, represents both an opportunity and a strategic test.

Can Paras help redistribute India’s specialist talent?

India’s healthcare challenge is not merely a shortage of doctors. It is also a problem of distribution.

Major metropolitan centres such as Delhi, Mumbai, Bengaluru, Chennai and Hyderabad have become magnets for specialists and superspecialists. As a result, many urban markets now face intense competition among hospitals for patients, while large parts of India’s hinterland remain underserved.

This concentration of talent has not occurred by accident. Specialists gravitated towards metros because they offered superior infrastructure, advanced diagnostic capabilities, stronger clinical support systems, better professional networks, and greater opportunities for career growth.

The consequence is visible across India. Patients from smaller cities routinely travel hundreds of kilometres for cardiac surgery, cancer treatment, neurosurgery, and other specialised procedures. The medical bill is only one part of the burden. Families also incur substantial costs related to travel, accommodation, lost wages, and caregiving.

Paras Health’s expansion strategy raises an interesting possibility: Could organised hospital chains become vehicles for redistributing specialist talent beyond the metros?

If Paras succeeds in creating modern tertiary-care infrastructure in regional markets, it may offer specialists an attractive alternative to overcrowded metropolitan ecosystems. Experienced clinicians could potentially access large patient volumes, leadership opportunities, lower living costs, and improved work-life balance without sacrificing clinical quality. The existing OTC brand trust may also help specialists build their practices faster, as patients are more willing to try a hospital whose parent brand they already trust.

For patients, the benefits could be even greater. Accessing advanced care closer to home reduces both direct healthcare costs and the often-overlooked accessibility costs associated with long-distance travel and prolonged stays in unfamiliar cities.

In this scenario, the outcome becomes a win-win-win proposition. Paras gains access to a differentiated talent pool, doctors gain new professional opportunities, and patients receive specialised care closer to where they live.

However, recruiting specialists to Tier-2 and Tier-3 cities requires more than competitive compensation. It demands robust clinical infrastructure, research opportunities, professional development pathways, quality schooling for families, and confidence that the healthcare ecosystem can support advanced medical practice.

If Paras can solve this equation, it may achieve something more significant than expanding a hospital network. It could help reshape the geography of healthcare delivery in India.

The real question: can Paras generate attractive returns?

Hospital investors often become overly focused on bed additions. The more important question is capital efficiency.

Every hospital chain can announce new projects. The challenge lies in generating attractive returns on the capital deployed.

This is where the comparison with Mankind becomes most difficult. Mankind’s growth required relatively modest incremental capital. Hospitals require continuous equipment upgrades, specialist recruitment, regulatory compliance investments, infrastructure expansion, and working capital support.

For Paras, long-term success will depend not merely on filling beds but on generating sustainable returns from those assets. Investors should therefore monitor return on capital employed alongside occupancy and profitability metrics. The OTC brand advantage may help on the occupancy front, but it cannot substitute for clinical excellence or operational efficiency.

The often-ignored risk: specialist dependency

One underappreciated risk in regional healthcare expansion is talent.

A pharmaceutical company can transfer sales representatives between territories. Hospitals cannot easily replicate specialist doctors.

Cardiac surgeons, oncologists, neurosurgeons, and critical care specialists remain scarce across India. As organised hospital chains expand into Tier-2 and Tier-3 markets, competition for clinical talent is intensifying.

For Paras, retaining specialists may become just as important as attracting patients. A hospital brand can create trust, but clinical excellence ultimately depends on the people delivering care. The OTC brand may bring a patient through the door for the first visit. Only clinical outcomes will bring them back or generate referrals.

Swot analysis

Strengths

Strong regional brand recognition in North and East India through decades of OTC product presence

Established presence in underserved healthcare markets

Improving occupancy and operational performance

Deep referral relationships with local physicians

Lower patient acquisition cost and higher ease of conversion due to existing household trust in the Paras name

Weaknesses

Higher leverage than many listed hospital peers

Limited national brand presence outside North and East India

Execution risk associated with large-scale expansion

Potential perception challenge as patients may associate Paras with OTC products rather than tertiary care

Opportunities

Rising healthcare demand in Tier-2 and Tier-3 cities where the OTC brand already enjoys deep penetration

Growth of government-funded healthcare schemes

Increasing health insurance penetration

Potential for regional medical tourism from neighbouring countries

Cross-selling: OTC products sold in hospital pharmacies, hospital patients becoming repeat OTC consumers

Threats

Expansion by larger organised hospital chains including Max Healthcare, Narayana Health, and Artemis

Specialist doctor shortages

Regulatory interventions on pricing

Delays in commissioning or ramping up new facilities

Brand dilution if clinical quality does not match OTC brand reputation

Verdict: a credible bharat healthcare story with a unique advantage

Paras Health is attempting something few organised hospital chains have achieved at scale: building a tertiary-care network centred on India’s underserved Tier-2 markets.

The strategic logic resembles elements of Mankind Pharma’s highly successful Bharat-focused expansion model. Both organisations recognised that India’s next wave of healthcare demand would emerge beyond the metros.

But Paras brings one asset that Mankind did not need and that no other hospital chain possesses: a household brand name built through decades of OTC products sitting on the shelves of millions of homes across North and East India. This brand trust has a real, quantifiable impact on patient acquisition ease and cost. In markets where a new hospital might spend years building recognition, Paras can open its doors with a name already trusted.

However, hospitals are not pharmaceutical companies. Beds do not scale like tablets. Buildings do not scale like brands. And clinical talent is harder to replicate than distribution networks.

The investment thesis therefore rests less on geographic expansion and more on execution. The OTC brand can bring patients in. Only clinical quality, specialist talent, and operational discipline will keep them coming back and generate the word-of-mouth referrals that drive sustainable occupancy.

The large offer for sale component means that early financial sponsors are exiting at this valuation. Investors must form their own view on whether the company’s growth prospects justify the asking price, particularly given the execution risks associated with the Gurugram and Ludhiana expansions.

The long-term opportunity extends beyond adding beds and hospitals. If the company can successfully attract specialist talent into regional markets, it could play a meaningful role in correcting one of India’s largest healthcare inefficiencies: the concentration of advanced medical care in a handful of metropolitan centres.

In doing so, Paras would not merely be expanding healthcare infrastructure. It would be expanding healthcare access. And it would be doing so with a brand that millions of Indian families already know and trust.

For millions of patients in Bharat, that distinction could prove transformative.

Disclaimer: This article is intended for educational and analytical purposes only and does not constitute investment advice. Readers should consult the company’s latest DRHP, financial disclosures, and qualified financial advisors before making investment decisions. MedicinMan does not endorse or recommend any security.

Appendix: Sources

Primary sources

Paras Healthcare Limited. (2026, June 4). Draft red herring prospectus (DRHP) filed with the Securities and Exchange Board of India (Sebi).

Paras Health annual report FY2024-25.

Paras Health investor presentations and corporate disclosures.

Paras Health corporate website.

Paras brand history and OTC product portfolio disclosures.

Comparative and industry sources

Mankind Pharma Limited. (2023). Annual report FY2022-23.

Mankind Pharma Limited. (2023). Red herring prospectus for Rs 4,326 crore IPO filed with Sebi.

Sebi filings database.

Healthcare Radius. (2025-2026). Hospital industry reports.

National Health Authority. (2025). Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB PM-JAY) annual report 2024-25.

NITI Aayog. (2024). Health insurance for India’s missing middle. Government of India.

ICRA Limited. (2025). Healthcare sector review: Hospital industry outlook.

CRISIL Ratings. (2025). Indian healthcare: Tier-2 cities driving growth.

Apollo Hospitals Enterprise Limited. (2025). Annual report FY2024-25.

Max Healthcare Institute Limited. (2025). Annual report FY2024-25.

Narayana Health Limited. (2025). Annual report FY2024-25.

Fortis Healthcare Limited. (2025). Annual report FY2024-25.

Aster DM Healthcare Limited. (2025). Annual report FY2024-25.

News and market coverage

The Economic Times. (2026, June 4). Paras Healthcare refiles IPO papers with Sebi; aims Rs 1,800 crore via fresh issue and OFS.

Mint. (2026, June 5). Paras Healthcare files DRHP for Rs 1,800 crore IPO.

Business Today. (2026, June 4). Paras Health IPO: Company files papers with Sebi.

Moneycontrol. (2026, June 4). Paras Healthcare files DRHP with Sebi for Rs 1,800-crore IPO.

Livemint. (2023, April 25). Mankind Pharma IPO subscribed 15.3 times on final day.

Financial Express. (2026, June 5). Paras Healthcare IPO: 800-bed expansion, debt repayment among key objectives.

CNBC TV18. (2026, June 4). Paras Healthcare files DRHP for Rs 1,800 crore IPO.

Note on financial figures

All financial figures and operational metrics cited in this article are based on company disclosures and publicly available information as of June 2026. The article references both FY25 and FY26 data from different stages of the filing process. Readers should verify all data against the latest DRHP and audited financial statements before making investment decisions. The author has made reasonable efforts to ensure accuracy but assumes no responsibility for errors or omissions.

{kind=link}