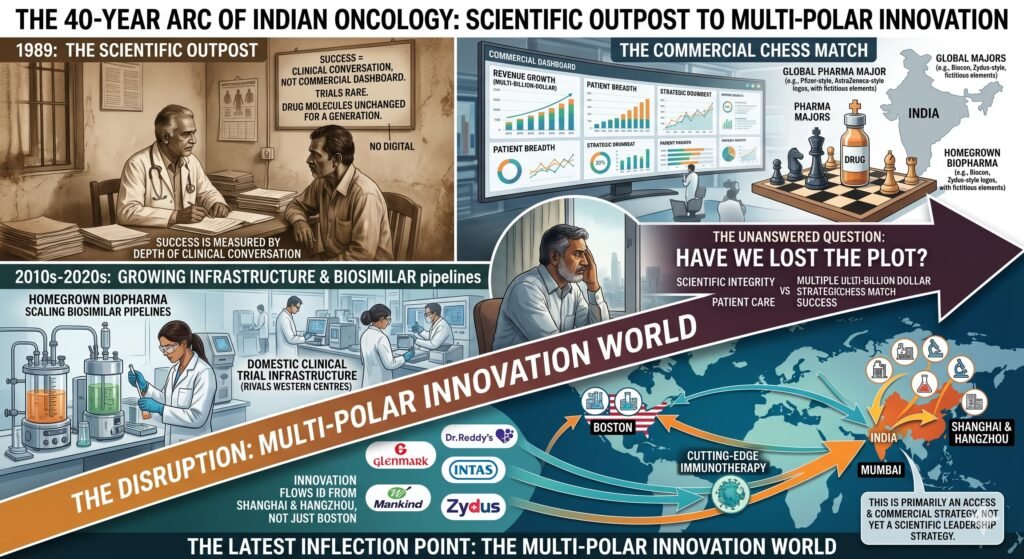

A Brief History of Scale and an Unasked Question

In 1989, oncology in India was not a business unit. It was a scientific outpost. In that era, practitioners measured success by the depth of a clinical conversation, not the breadth of a commercial dashboard. Clinical trials were rare. Drug innovation was a distant hum, not a strategic drumbeat. The patient who walked into a cancer ward often walked out with little but a prescription for a molecule that had remained unchanged for a generation.

Four decades later, the Indian oncology ecosystem is unrecognisable. It has grown into a multi-billion-dollar strategic chess match, with global pharmaceutical majors vying for position, homegrown biopharma firms scaling biosimilar pipelines, and a domestic clinical trial infrastructure that rivals many Western centres. As Subroto Banerjee observed, however, the transformation has come with a lingering question: Have we lost the plot?

That question was posed before the latest inflection point. Now, a significant but often misunderstood disruption is underway. It is powered by a set of actors that barely featured in the strategic calculus of the 1990s or even the 2010s. This disruption is forcing a fundamental re-evaluation of what Indian oncology strategy means, who defines it, and for whose benefit it operates.

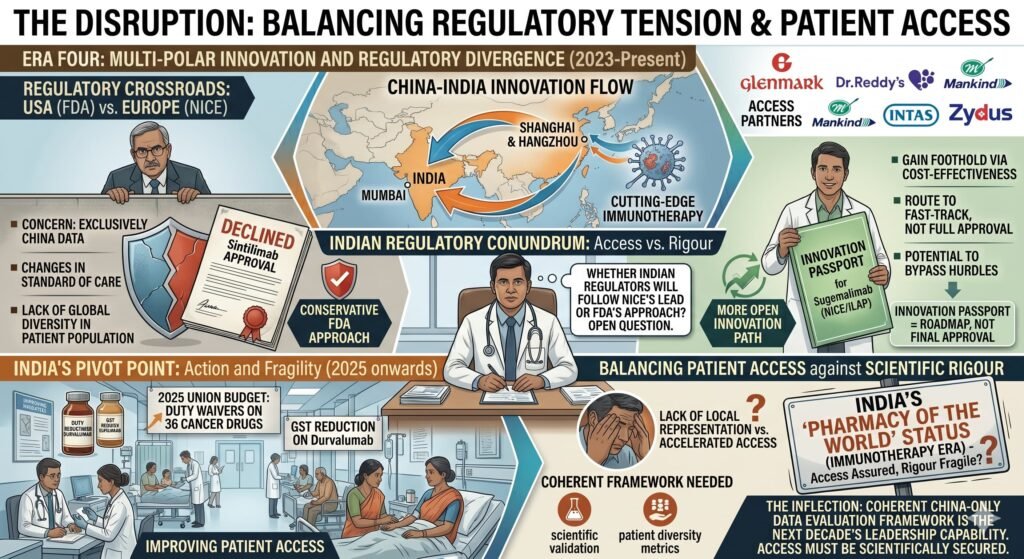

This article revisits Banerjee’s 40-year arc, extends it into the present, and argues that the next decade of Indian oncology leadership will be defined by a specific capability: the ability to navigate a multi-polar innovation world. In this world, cutting-edge immunotherapy no longer flows exclusively from Boston to Mumbai, but increasingly from Shanghai and Hangzhou, via partners like Glenmark, Dr. Reddy’s, Mankind, Intas, and Zydus. However, this is primarily an access and commercial strategy, not yet a scientific leadership strategy. That distinction is critical.

II. The First Four Decades: Three Eras of Building Capability

Before examining the current shift, it is worth mapping the historical framework that preceded it.

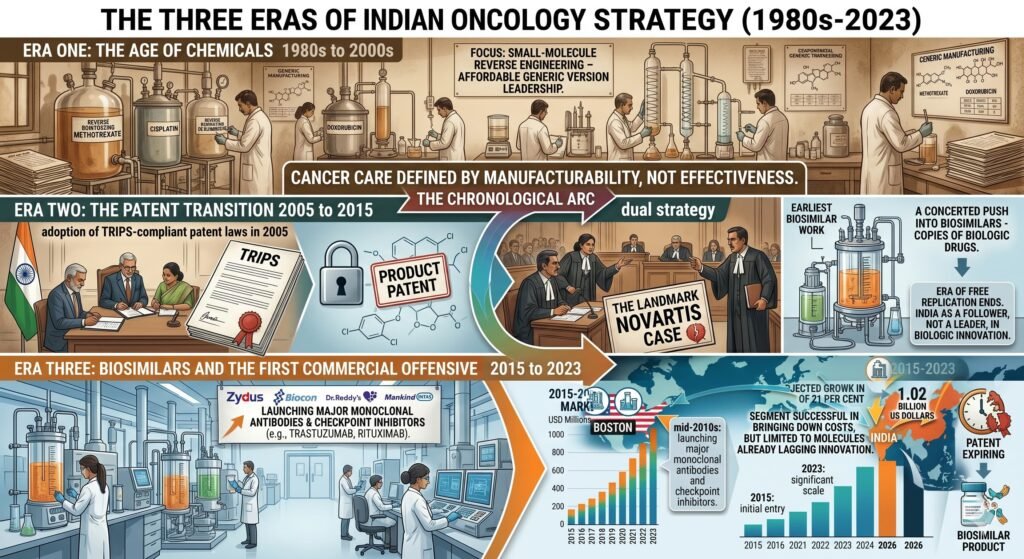

Era One: The Age of Chemicals – 1980s to 2000s

India’s early oncology strategy was defined largely by the reverse engineering of small-molecule chemotherapeutics. Under a patent regime that did not recognise product patents, Indian manufacturers became world leaders in producing affordable generic versions of drugs like methotrexate, cisplatin, and doxorubicin. Cancer care was defined by what was manufacturable, not necessarily what was most effective.

Era Two: The Patent Transition 2005 to 2015

India’s adoption of TRIPS-compliant patent laws in 2005 marked a tectonic shift. The era of free replication ended. In its place emerged a dual strategy: aggressive patent litigation, the landmark Novartis case being the most famous example, and a concerted push into biosimilars, which are copies of biologic drugs just complex enough to keep the legal doors open. During this period, India built early expertise in biologics manufacturing, but the country remained largely a follower, not a leader, in biologic innovation.

Era Three: Biosimilars and the First Commercial Offensive 2015 to 2023

By the mid-2010s, Indian firms had begun launching biosimilar versions of major monoclonal antibodies and checkpoint inhibitors. Zydus, Biocon, Dr. Reddy’s, and others entered the oncology biosimilar space in earnest. By 2026, this segment is projected to grow from 184 million US dollars to 1.02 billion US dollars at a compound annual growth rate of 21 per cent. The biosimilar strategy succeeded in bringing down costs, but only for molecules that had already lost patent protection or faced legal vulnerability.

III. The Disruption: A New Axis Emerges, But With Caveats

Banerjee’s question, Have we lost the plot, assumed that the plot was singular: that Indian oncology strategy could be judged by a single metric of scientific advancement or commercial success. The current disruption suggests a different answer: the plot has not been lost, but it has multiplied.

The first plot, the one Banerjee described, is about clinical depth, therapeutic innovation, and the race toward cell therapy. That race continues, with Indian biotech ImmunoACT developing a CAR-T cell therapy that costs 30,000 to 40,000 US dollars per treatment, approximately one-tenth of Western equivalents.

The cost has been brought down to approximately 50,000. The second plot is about access, commercial partnerships, and the reconfiguration of the global oncology supply chain. In this plot, the leading actors are Chinese biotech firms and their Indian commercial partners. A significant shift is underway in Indian oncology. Chinese-origin cancer drugs, brought to India through a growing number of pharma partnerships, are dramatically cutting the cost of immunotherapy, making treatment accessible to patients who previously had no options. Western immunotherapy can cost up to five lakh rupees per session. Chinese-origin alternatives are bringing the cost down to approximately 50,000 rupees per session. Doctors across India are prescribing these therapies, and early patient responses are positive.

However, a key caveat needs to be stated clearly. The current rewiring is primarily a commercial and access strategy, not yet a scientific leadership strategy. Indian firms are acting as agile distributors and integrators of non-Western innovation. They are not yet co-discovering or co-developing novel molecules at scale. This is not a criticism. Access matters enormously. But the difference between consuming innovation and creating it is essential for long-term strategic planning.

IV. The Clinical Reality: Efficacy Data from China

The affordability argument would carry little weight without clinical substance. The clinical data emerging from Chinese phase III trials, increasingly presented at ASCO and ESMO, suggest that these drugs are not merely cheaper. They are clinically competitive.

In the phase III HARMONi-6 trial, the bispecific antibody ivonescimab, given with chemotherapy, improved progression-free survival by 4.2 months compared with the PD-1 inhibitor tislelizumab plus chemotherapy. This represented a 40 per cent reduction in risk as a first-line treatment for advanced squamous non-small cell lung cancer. Median progression-free survival was 11.1 months with ivonescimab versus 6.9 months with tislelizumab, with benefit consistent across PD-L1 expression subgroups.

At ASCO 2025, Henlius Biotech presented data on serplulimab, an anti-PD-1 monoclonal antibody. The phase III ASTRUM-005 trial showed that serplulimab plus chemotherapy achieved a median overall survival of 15.8 months versus 11.1 months for placebo in extensive-stage small cell lung cancer patients, a 40 per cent reduction in death risk. With a median follow-up of 42.4 months, the four-year overall survival rate was 21.9 per cent in the serplulimab arm versus 7.2 per cent in the placebo arm.

These are not marginal improvements. However, two qualifications are necessary. First, the HARMONi-6 trial compared ivonescimab to tislelizumab, another Chinese PD-1, not directly to Western standards like pembrolizumab. Second, long-term safety and immunogenicity data in genetically diverse Indian populations are still limited. Indian post-marketing surveillance is needed.

V. The Deal Flow: From Glenmark to Dr. Reddy’s to Mankind

What makes this disruption structural, not anecdotal, is the volume and scale of licensing agreements signed between Indian and Chinese pharma companies. Indian firms are not passive distributors. They are active, strategic partners, though primarily in a licensing and commercialisation role.

In April 2026, Glenmark Pharma licensed envafolimab from Jiangsu Alphamab Biopharmaceuticals and 3D Medicines. The drug is a subcutaneously administered PD-L1 inhibitor, the first drug in its class to be approved in a subcutaneous formulation. Glenmark secured rights across India, Asia-Pacific, the Middle East, Africa, Russia, the CIS, and Latin America, with a low double-digit million upfront payment and triple-digit million dollar milestone payments based on sales. Glenmarks chairman and managing director described the deal as transformational.

In December 2025, Dr. Reddy’s entered a strategic collaboration with Immutep for eftilagimod alfa, a first-in-class novel immunotherapy that directly activates the immune system to fight cancer. The drug is under evaluation in a registrational phase III trial for advanced metastatic non-small cell lung cancer. Dr. Reddy’s secured exclusive rights to develop and commercialise the drug in all countries outside North America, Europe, Japan, and Greater China. The terms included a 20 million US dollar upfront payment, milestone payments up to 349.5 million US dollars, and double-digit royalties on commercial sales.

In 2023, Dr Reddy’s struck a deal with Shanghai Junshi Biosciences to sell toripalimab for recurrent metastatic nasopharyngeal carcinoma, covering 21 countries, including Brazil. The drug has been positioned as a next-generation PD-1 inhibitor, improving market access and bridging treatment gaps for patients in India.

Chinese bispecific antibodies are also entering the pipeline. Jiangsu Hengrui received an upfront payment of 18 million US dollars and milestone payments of up to 1.09 billion US dollars from Glenmark Specialty for rights to an antibody-drug conjugate. In July 2025, Henlius Biotech’s serplulimab was approved by Indias Central Drugs Standard Control Organisation for first-line treatment of extensive-stage small cell lung cancer, the first anti-PD-1 monoclonal antibody approved for that indication in India. It was launched at approximately 75 per cent lower cost than existing immunotherapies for this indication.

Intas, Glenmark, and Dr. Reddy’s are not alone. In December 2024, Mankind Pharma entered an agreement with Innovent Biologics to sell sintilimab in India under license, with exclusive rights to register and commercialise the drug. Sintilimab has eight approved indications in China, including non-small cell lung cancer, liver cancer, and gastric cancer. Market sources indicate Mankind intends to price sintilimab competitively.

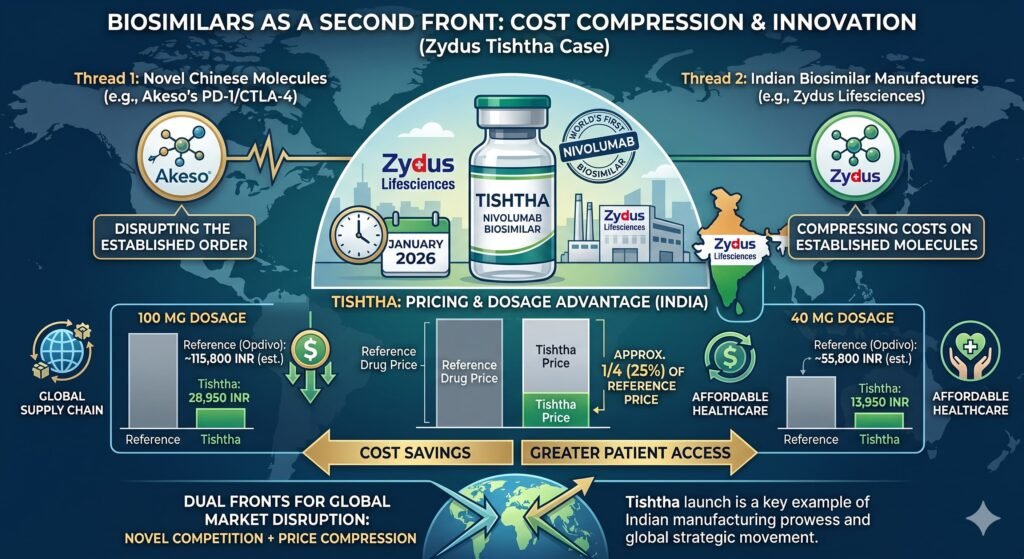

VI. Biosimilars as a Second Front: The Case of Tishtha

While Chinese novel molecules represent one disruptive thread, Indian biosimilar manufacturers are further compressing costs on established molecules. In January 2026, Zydus Lifesciences launched Tishtha, the worlds first biosimilar of nivolumab, in India. Tishtha is available in 100 milligram and 40 milligram dosages priced at 28,950 rupees and 13,950 rupees respectively, approximately one-quarter of the reference drugs price.

Nivolumab, branded as Opdyta, typically ranges from 36,000 to over 90,000 rupees per vial, depending on dosage. The two-strength portfolio enables oncologists to optimise dosing and minimise wastage, a key driver of treatment economics in immunotherapy.

The Indian biosimilars market is moving beyond a launch-centric phase into one where the depth of the pipeline and therapeutic diversification define long-term competitiveness. With Indias biologics and biosimilar markets projected to double to 30 to 35 billion US dollars by 2030, oncology biosimilars are emerging as a high-growth segment. However, the 30 to 35 billion dollar figure likely refers to the total biologics market, including novel biologics, not biosimilars alone. The oncology biosimilars segment specifically is growing at a compound annual growth rate of 8.22 per cent.

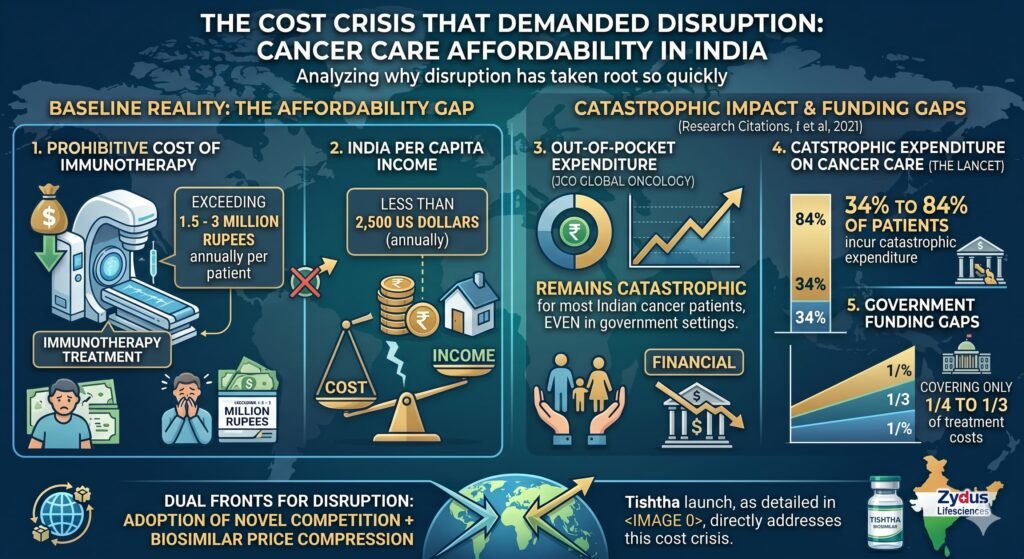

VII. The Cost Crisis That Demanded Disruption

To understand why this disruption has taken root so quickly, one must appreciate the baseline reality of cancer care affordability in India.

The cost of immunotherapy in India is often prohibitive, exceeding 1.5 to 3 million rupees annually per patient, in a country where per capita income is less than 2,500 US dollars. A study published in JCO Global Oncology highlighted that out-of-pocket expenditure remains catastrophic for most Indian cancer patients, even in government settings. A study in The Lancet found that 34 to 84 per cent of patients in India incur catastrophic expenditure on cancer care, with government funding covering only a quarter to a third of treatment costs.

Dr Sunil Chopadecancer specialist at Mumbai’, a medical oncologist at Mumbai’s Jaslok Hospital, notes that western-origin immunotherapies, including nivolumab and pembrolizumab, have historically been prohibitively expensive in India. Keytruda can cost 1-2 lakh rupees per cycle. The key driver behind the shift to Chinese medicines is the cost of treatment.

Dr Vijay Patil, a cancer specialist at Mumbai’s PD Hinduja Hospital, prescribed a newly approved Chinese-origin immunotherapy for a 72-year-old patient with advanced small-cell lung cancer when the standard multinational drug was beyond reach. Administered alongside chemotherapy, it delivered a strong clinical response within four cycles. The patient has since transitioned to maintenance immunotherapy and remains stable. These are not isolated anecdotes. An increasing number of doctors in India are treating cancer patients with Chinese-origin drugs imported through tie-ups with Indian companies.

However, the claim that Chinese alternatives cost 50,000 rupees per session compared to 5 lakh rupees for Western immunotherapy requires context. Fifty thousand rupees per session still translates to 6 to 10 lakh rupees annually for a full course of 12 to 20 cycles. For a majority of Indian patients, this remains catastrophic expenditure. The improvement is real and valuable, but it is not a solution to the affordability crisis. It is a significant reduction in harm.

VIII. Regulatory Hurdles and the Path Forward

The disruption, however, is not frictionless. A significant regulatory tension remains. At present, many of the new PD-1 and PD-L1 drugs have clinical trials conducted exclusively in China. This can raise concerns with local regulators that wish to see more diverse or locally representative patient inclusion criteria. The United States Food and Drug Administration declined approval of Lillys sintilimab in part due to the availability of China-only data. However, the FDAs concern was not just the China-only nature of the data but also changes in the standard of care during the trial and a lack of global diversity in the patient population. The article simplifies this issue.

In Europe, however, the calculus may differ. Lower-priced innovation could gain a foothold if calculated to be highly cost-effective. Sugemalimab received an Innovation Passport in NICE’s Innovative Licensing and Access Pathway in 2021, potentially allowing it to bypass some conventional evidentiary hurdles. However, an Innovation Passport is not an approval. It is a route to potentially faster approval. The distinction is important.

Whether Indian regulators will follow NICE’s lead or the FDAs more conservative approach remains an open question. This question could determine the pace of patient access. India has already begun to act. The 2025 Union Budget introduced duty waivers on 36 cancer drugs, including a goods and services tax reduction on durvalumab. The Central Drugs Standard Control Organisation has approved multiple Chinese-origin drugs for specific indications. But a coherent framework for evaluating China-only data, one that balances patient access against scientific rigour, has yet to be fully articulated.

IX. A New Strategic Framework for Indian Oncology

What does this mean for the strategic direction of Indian oncology?

First, the source of innovation has diversified beyond the Western-dominated axis. For decades, Indian oncology strategy was reactive: copy what the West invented, then litigate or subsidise access. The current disruption suggests that proactive licensing of non-Western innovation, particularly from China’s rapidly maturing biopharma sector, offers a faster path to patient access and commercial growth.

We identify, evaluate, and partner with the most promising global innovations, wherever they come from. Second, affordability and innovation are no longer trade-offs. The Chinese PD-1 inhibitors in trials are not inferior generics. They are novel molecules that sometimes demonstrate superior progression-free and overall survival compared to existing standards of care, at a fraction of the price. Indian pharma’s challenge is no longer just manufacturing cheap copies. We identify, evaluate, and partner with the most promising global innovations, wherever they come from.

Third, policy must evolve from a defensive to a strategic posture. The focus on blocking patent extensions and defending compulsory licensing, while important, is insufficient. India needs a proactive regulatory framework that expedites approval of well-designed innovation from emerging biotech hubs, that incentivises local phase III confirmatory trials when appropriate, and that acknowledges that patient access is itself a public health priority.

Fourth, the patient must remain the unit of analysis. As Banerjee noted, earlier eras measured success by the depth of a clinical conversation. The commercialisation of oncology brought scale but risked abstraction. The current disruption, powered by affordable and clinically robust therapies, offers an opportunity to return that conversation to the centre of clinical practice.

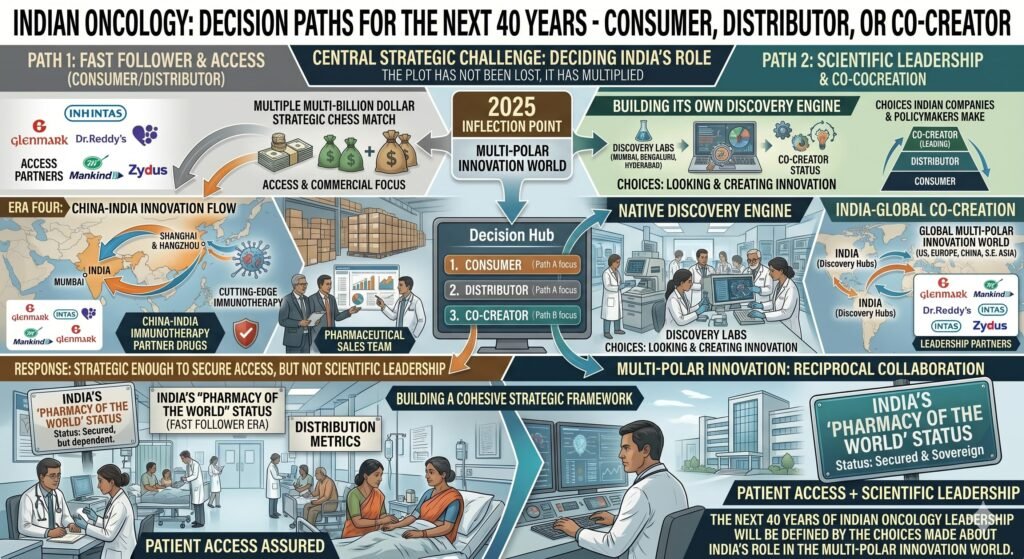

Fifth, and critically, Indian firms must decide whether they wish to remain distributors or become co-developers. The current wave of licensing deals is a commercial success. But if Indian capital and clinical talent are deployed only to commercialise Chinese phase III assets, while Chinese firms build global brands and direct market access, then India will have improved access without building strategic scientific leadership. The quiet rewiring is real. But it is not yet a scientific rewiring.

X. The Next 40 Years

Banerjee asked whether Indian oncology had lost the plot. This article argues that the plot has not been lost. It has multiplied. However, the central strategic challenge has been misdiagnosed. It is not simple to manage a multi-polar innovation world. It is to decide what role India will play in that world: consumer, distributor, or co-creator.

The next 40 years of Indian oncology strategy will not be defined solely by which cell therapy receives approval or which clinical trial completes enrolment. It will be defined by the choices Indian companies and Indian policymakers make about where to look for innovation, how to assess it, and how quickly to bring it to patients who need it most. But it will also be defined by whether India builds its own discovery engine or remains a fast follower to both Boston and Shanghai.

China has entered the room. The question is no longer whether Indian oncology will respond. It is whether the response will be strategic enough to move beyond access and toward genuine scientific leadership.

APPENDIX: SOURCES AND RECOMMENDED FURTHER READING

MedicinMan Sources

The Economic Times Sources

ET Online, Morning Brief Podcast, How Chinese Pharma Helping Indian Patients with Cutting Edge Therapies, The Economic Times, May 10, 2026. This podcast episode explores the India-China pharma axis and its impact on patient access. A key statistical claim cited is that Western immunotherapy costs up to 5 lakh rupees per session while Chinese-origin alternatives bring this down to 50,000 rupees.

Zydus Launches Nivolumab Biosimilar Tishtha in India, The Economic Times, January 22, 2026. This is primary reporting on the world’s first nivolumab biosimilar, including pricing at one-quarter of the reference drug and availability in 40 milligram and 100 milligram dosages.

Peer-Reviewed and Academic Literature

Pramesh CS, Badwe RA, Borthakur BB, et al., Delivery of Affordable and Equitable Cancer Care in India, JCO Global Oncology, 2020. This is a foundational study highlighting catastrophic out-of-pocket expenditure for most Indian cancer patients even in government settings, cited in the BMJ rapid response analysed below.

BMJ Rapid Response, Should India Fund Free Immunotherapy for Cancer Patients A Policy Dilemma, BMJ, May 2025. This is a comprehensive analysis of the affordability crisis in Indian immunotherapy, citing annual costs exceeding 1.5 to 3 million rupees per patient and Indias per capita income below 2,500 US dollars. It includes references to Ayushman Bharat coverage gaps and cost-effectiveness thresholds in low- and middle-income countries.

Frontiers in Pharmacology, Comparative Cost-effectiveness of Sintilimab, Toripalimab and Camrelizumab, December 2025. This is a quantitative analysis of Chinese PD-1 inhibitors, finding that sintilimab incurred the lowest cost of 230,813 Chinese yuan generating 1.1 quality-adjusted life years, with toripalimab yielding the same quality-adjusted life years at higher cost.

Indian Healthcare and Biopharma Industry

Sheetal Sapale, Vice-President Commercial, Pharmarack Technologies, Indian Biosimilar Market is Moving Beyond Launch-Centric Phase, BioSpectrum India, February 2026. This provides an industry perspective on the Indian biosimilars market evolution toward pipeline depth and therapeutic diversification.

Budget 2026 Targets Indias Cancer Crisis With Duty Relief, BW Healthcare World, February 2026. This provides an analysis of Indias oncology biosimilars market growth of 8.22 per cent compound annual growth rate and policy measures including duty waivers on 36 cancer drugs.

India Emerging as Major Market for Biosimilar Immunotherapy, But Patient Awareness Still Lags Oncologists, ETHealthWorld, May 2026. This article notes that despite falling drug costs, low patient awareness and late-stage diagnosis prevent many from benefiting from these therapies.

Key Deals and Licensing Agreements Primary Business Sources

Glenmark licenses envafolimab from Alphamab and 3D Medicines, Pharmaphorum, April 2026. This provides detailed deal terms including the subcutaneous PD-L1 inhibitor, rights across emerging markets, and milestone structures.

Hengrui-Glenmark ADC deal, Reuters, September 2025. This reports an 18 million US dollar upfront payment plus up to 1.09 billion US dollars in milestones for an antibody-drug conjugate.

Dr. Reddy’s-Immutep collaboration for eftilagimod alfa, GlobeNewswire, December 2025. The terms include 20 million US dollars upfront, up to 349.5 million US dollars in milestone payments, and double-digit royalties.

Bio-Thera and Henlius grant rights to Intas, Yicai Global, February 2026. This deal can bring up to 165 million US dollars from upfront payments, milestones, and royalties.

Mankind Pharma-Innovent Biologics agreement for sintilimab, Business Standard, December 2024. This grants exclusive rights to sell sintilimab in India with eight approved indications in China.

Clinical Data Sources Major Trials

HARMONi-6 trial for ivonescimab, ASCO Post, November 2025. Phase III data showed median progression-free survival of 11.1 months versus 6.9 months with a hazard ratio of 0.60.

ASTRUM-005 trial for serplulimab, MedPath and ASCO, June 2025. Phase III data in extensive-stage small cell lung cancer showed median overall survival of 15.8 months versus 11.1 months with a hazard ratio of 0.60. The four-year overall survival rate was 21.9 per cent versus 7.2 per cent.

FH-deficient RCC trial for sintilimab, JAMA Network, October 2025. This open-label phase II trial in a rare kidney cancer showed median progression-free survival of 19.8 months.

Ivonescimab versus Keytruda, MedPath, June 2025. The Chinese combination therapy outperformed pembrolizumab in PD-L1-positive lung cancer, increasing median progression-free survival by 3.9 months to 11 months total with a 30 per cent risk reduction.

Regulatory and Policy Context

Low-Priced Oncology Disruptors, Pharmaphorum, April 2026. This provides an analysis of the challenge of China-only clinical trial data for regulatory approvals, citing the FDA sintilimab rejection and the NICE ILAP pathway for sugemalimab.

Indian Cancer Immunotherapy Market forecasts, IMARC Group, 2025. The market reached 4.4 billion US dollars in 2025 and is expected to reach 10.0 billion US dollars by 2034 at a compound annual growth rate of 9.22 per cent.

Indian biosimilars market forecast, Research and Markets. The market is projected to grow from 184 million US dollars to 1.02 billion US dollars by 2035 at a compound annual growth rate of 21 per cent.

Union Budget 2026. This introduced duty waivers on 36 cancer drugs and a goods and services tax reduction on durvalumab.

International Pricing and Global South Perspectives

Intas Hetronifly serplulimab India launch, BioSpectrum India, August 2025. The drug was launched at approximately 75 per cent lower cost than existing immunotherapies for extensive-stage small cell lung cancer in India.

ImmunoACT CAR-T cell therapy, 36Kr, January 2026. The single treatment cost is 30,000 to 40,000 US dollars, approximately 2 to 3 million rupees, which is about one-tenth of Western equivalents.

CytoMed technology acquisition, BioSpectrum Asia, November 2025. This involves T-cell technology repurposed for cancer applications in China and India.

Critical Commentary and Nuanced Analysis Added by MedicinMan Research Desk

The central distinction between access strategy and scientific leadership. This article explicitly distinguishes between improving patient access through licensing, which is valuable and real, and building domestic scientific leadership in novel immunotherapy discovery, which has not yet been achieved. The current rewiring is primarily the former.

Qualification of cost comparisons. The claim that Chinese alternatives cost 50,000 rupees per session compared to 5 lakh rupees for Western immunotherapy is accurate, but this article adds the crucial context that 50,000 rupees per session still represents 6 to 10 lakh rupees annually for a full course of 12 to 20 cycles. For most Indian patients, this remains catastrophic expenditure.

Clarification of regulatory nuance. The FDA rejection of sintilimab was not solely about China-only data but also about changes in the standard of care during the trial and lack of global diversity. The NICE Innovation Passport for sugemalimab is not an approval but a pathway to potentially faster approval. This article corrects both simplifications.

The total biologics market and the distinction between it and the oncology biosimilars market. The 30 to 35 billion US dollar figure for 2030 likely refers to the total Indian biologics market, including novel biologics. The oncology biosimilars segment specifically is projected to grow at an 8.22 per cent compound annual growth rate.

Acknowledgement: This article synthesises reporting from The Economic Times and historical analysis from Subroto Banerjee’s original MedicinMan piece, and is extended with primary-source verification of key deals, clinical trials, and market data. Critical commentary and nuanced qualifications have been added by the MedicinMan Research Desk to address overclaims and simplifications in the original reporting. Direct citations are provided in-line with MedicinMan publication standards.

{kind=link}