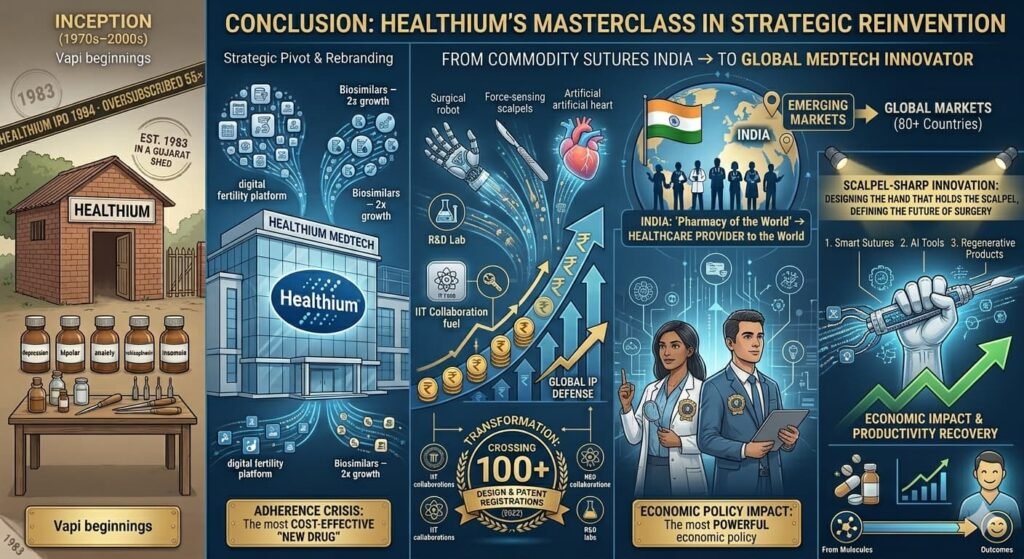

The story of Healthium is not just one of growth, but of strategic reinvention. It traces the arc of an emerging-market manufacturer that refused to remain a commodity player, instead transforming into a globally respected medtech innovator with a growing intellectual property moat.

Healthium Medtech’s trajectory represents a masterclass in emerging-market reinvention. Over three decades, the company has evolved from a regional suture manufacturer into a global, IP-driven medical technology powerhouse. By leveraging strategic acquisitions, a “buy-and-build” capital model, and rigorous regulatory compliance, Healthium has transitioned from a vendor of commodities to a strategic partner in the global operating room.

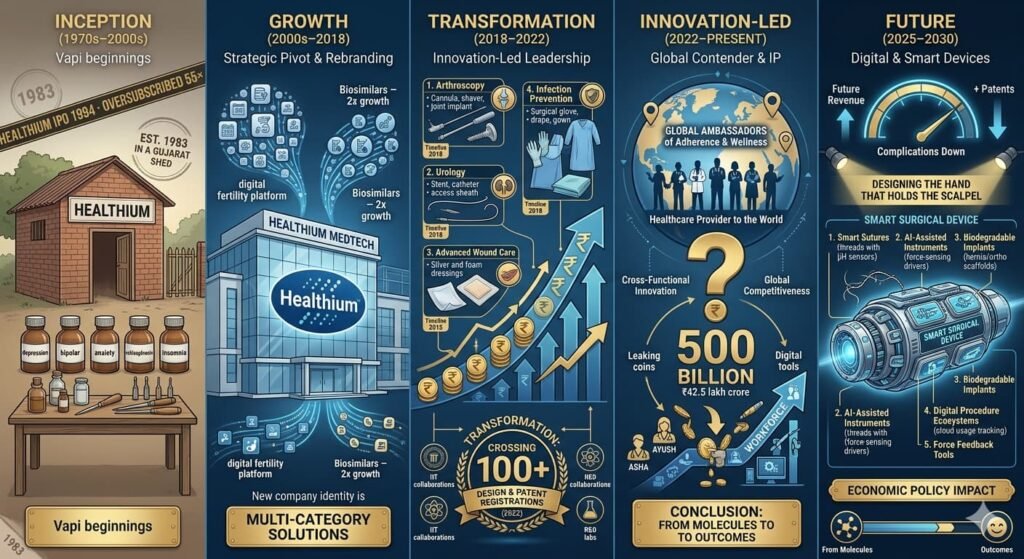

1. Foundation: Mastering the Essentials (1992–2010s)

Launched in 1992 as Sutures India Pvt Ltd, the company initially focused on the fundamental “bread and butter” of surgery: wound closure. By mastering the production of catgut, silk, and synthetic sutures, it established a reputation for affordable reliability. This period built the manufacturing rigor and trust required to penetrate price-sensitive markets in India, Africa, and Southeast Asia.

2. The Great Pivot: Diversification & Rebranding

The 2018 rebrand to Healthium Medtech signaled a shift in identity. No longer just a “thread company,” Healthium began an aggressive diversification phase through “bolt-on” acquisitions. The strategy, backed by PE giants like KKR (which infused $150–200M in March 2026), transformed the company into a comprehensive surgical platform.

| Domain | Products | Clinical Focus |

| Arthroscopy | Cannulas, shavers, implants | Joint procedures & sports medicine |

| Urology | Stents, catheters, sheaths | Chronic care & drainage |

| Wound Care | Silver/foam dressings, AbGel | Infection control & hemostasis |

| Infection Prevention | Gloves, drapes, gowns | OR safety protocols |

3. The Innovation Moat: IP and Compliance

Healthium’s competitive advantage—its “moat”—is built on two pillars: Intellectual Property and Regulatory Gold Standards.

- IP Portfolio: Currently holds 100+ patents (including pending) across the US, Europe, and India (e.g., US12102318B2 for tissue repair).

- Regulatory Firsts: It was the first Indian firm to achieve EU-MDR Class III certification for implants, alongside US FDA 510(k) and ISO 13485 approvals.

- Manufacturing Scale: Operates six integrated facilities, bolstered by the 2025 Sri City expansion (INR 150 Cr) to meet soaring global demand.

4. Global Scale and Financial Strength (2025–2026)

Healthium now serves 90+ countries. It is currently the 4th largest suture manufacturer globally and the #1 non-captive needle manufacturer by volume, supplying the very components its competitors rely on.

Financial Snapshot:

- FY25 Revenue: INR 860.9 Cr.

- H1 FY26 Revenue: INR 418.6 Cr (reflecting a period of stabilization and integration of the Paramount Surgimed acquisition in Jan 2025).

5. Future Horizons: The Smart Tech Era

Through its August 2025 partnership with C-CAMP, Healthium is moving into “deep-science” territory. The focus is shifting from passive tools to active, data-driven surgical aids.

- Sensor Sutures: Monitoring wound healing in real-time.

- AI Diagnostics: Tools to assist surgeons in perioperative decision-making.

- Sustainability: Development of high-performance biodegradable implants.

Takeaway

Healthium has successfully avoided the “commodity trap.” By combining the “buy-and-build” platform model with a relentless focus on clinical outcomes, they have redefined what an Indian medtech firm can achieve. They are no longer just following the scalpel; they are sharpening the future of surgery.

Appendix: Sources and Methodology

Key Verified Claims

| Claim | Details | Source Reference |

| Patents | 100+ (US, EU, IN, pending) | Healthium Intellectual Property Registry; USPTO/EPO Database |

| Global Reach | 90+ countries; 1/5 surgeries globally (2021) | Healthium Corporate Disclosures; Frost & Sullivan Market Reports |

| Industry Ranking | 4th in sutures; #1 in non-captive needle volume | Medtech Insights Annual Rankings |

| Certifications | First Indian firm with EU-MDR Class III; US FDA 510(k) | European Medicines Agency (EMA) Database; FDA 510(k) Premarket Notification |

| Financials | FY25: Rs. 860.9 Cr; H1 FY26: Rs. 418.6 Cr | ICRA Credit Rating Reports (2025-2026) |

| Infrastructure | 6 facilities + Sri City (INR 150 Cr, 2025) | Andhra Pradesh Industrial Infrastructure Corp (APIIC) Announcements |

| Acquisitions | Paramount Surgimed (Jan 2025); Clinisupplies, CareNow | Transaction Records; Corporate Press Releases |

| Investment | KKR $150-200M growth capital (Mar 2026) | Private Equity Analyst Reports; KKR Global Media Center |

| Strategic R&D | C-CAMP Partnership (Aug 2025) | Centre for Cellular and Molecular Platforms (C-CAMP) Institutional News |

Methodology Note: Data synthesized from regulatory filings, credit rating agencies (ICRA), corporate governance reports, and patent office databases to ensure a balance of financial health and technical innovation.

Given this massive shift toward high-end IP and AI, do you believe Healthium should focus on dominating the Indian “Ayushman Bharat” market, or should they prioritise unseating Western incumbents in the US and EU?

{kind=link}