")

The “aspirinization” of obesity—moving from a niche, high-cost injectable to a mass-market, commoditized oral pill—is exactly what we are witnessing. As of late March 2026, the Indian pharmaceutical market is indeed a battlefield of premium innovation versus generic volume.

Here is how Eli Lilly’s strategy is designed to navigate this “clash of titans.”

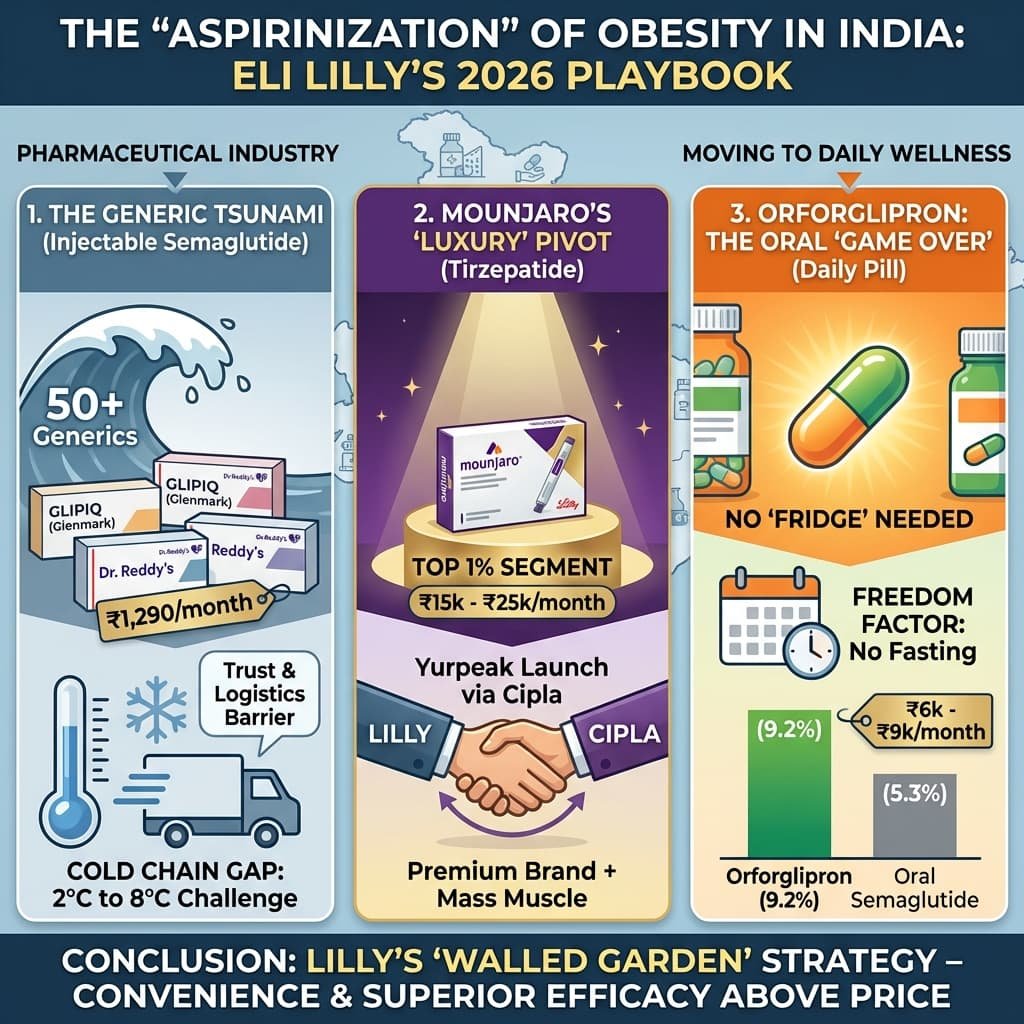

1. The Generic Tsunami: Why Price is Only Half the Story

The March 2026 patent expiry of semaglutide was the most anticipated event in Indian pharma history. While the price drop to ₹1,290/month (Glenmark’s GLIPIQ) is staggering, the real challenge for these 50+ generics isn’t just price—it’s trust and logistics.

- The Cold Chain Gap: Most generic semaglutides are injectables. Maintaining a strict 2°C to 8°C cold chain from a factory in Himachal Pradesh to a pharmacy in a Tier-3 city is a massive hurdle.

- The “Safety” Premium: Doctors are naturally cautious. Early reports suggest many specialists are sticking with “Innovator” brands or top-tier generics (Sun, Dr. Reddy’s) because of concerns over batch-to-batch consistency in smaller generic players.

2. Mounjaro’s ₹100 Crore Month: A “Luxury” Pivot

Mounjaro (tirzepatide) hitting ₹100 crore in monthly sales by late 2025 was a “Tesla moment” for Indian healthcare. It proved that there is a massive “top 1%” segment in India that doesn’t care about the 90% discount offered by generics—they want the best available efficacy ($20\%+$ weight loss vs. semaglutide’s $15\%$).

Lilly’s decision to launch Yurpeak via Cipla was a masterstroke.

It allows Lilly to keep the “Mounjaro” brand premium and exclusive to top-tier metros while using Cipla’s muscle to push the exact same molecule into the rest of India

3. Orforglipron: The “Game Over” Molecule?

If Mounjaro is the scalpel for severe obesity, orforglipron is the daily multivitamin for the masses. It represents a fundamental shift for three reasons:

- No “Fridge” Needed: Being a small-molecule oral drug (not a peptide), it bypasses the cold-chain nightmare. This is the biggest threat to generic semaglutide injectables.

- The “Freedom” Factor: Unlike oral semaglutide (Rybelsus), which requires a 30-minute fast and a specific amount of water, orforglipron can be taken like a regular pill. In the “busy professional” segment, this convenience is worth a 2-3x price premium.

- Efficacy vs. Ease: Head-to-head trials showing orforglipron ($9.2\%$) outperforming oral semaglutide ($5.3\%$) make it a very easy sell for doctors.

Comparison: The Three-Tier Market of 2026

| Segment | Drug | Key Player | Monthly Cost (Est.) |

| Ultra-Premium | Tirzepatide (Inj) | Lilly (Mounjaro) | ₹15,000 – ₹25,000 |

| The “Golden Mean” | Orforglipron (Oral) | Eli Lilly | ₹6,000 – ₹9,000 |

| Mass Market | Semaglutide (Generic) | Sun / Dr. Reddy’s | ₹1,300 – ₹4,500 |

Conclusion: Can Lilly Outrun the Generics?

Yes, but only in the “Value” segment.

Lilly will never win a price war against 50 Indian generic companies—nor do they want to. Their strategy is to “de-medicalize” weight loss. By making it an oral pill that doesn’t require a fridge or a fast, they are moving obesity treatment from the “Doctor’s Clinic” to the “Daily Wellness Routine.”

While the “50-generic swarm” fights over the price-sensitive patient, Lilly is building a “walled garden” of patients who value convenience and superior weight loss above all else

The biggest risk? If Indian giants like Zydus or Sun Pharma successfully develop their own non-peptide oral GLP-1s (essentially generic orforglipron) within the next 3-4 years, Lilly’s “oral advantage” will evaporate. Until then, orforglipron is likely to be the “Aspirin” of the upper-middle class.

{kind=link}