The economic footprint of a truly historic pharmaceutical blockbuster extends far beyond corporate balance sheets; it acts as a sovereign macroeconomic engine. When a single molecule commands billions in annual global trade, it reshapes the economic architecture of its home nation. In countries like Denmark, the meteoric expansion of Novo Nordisk’s metabolic portfolio has fundamentally altered national GDP growth, driven employment, and forced central banks to manage unique currency dynamics. From Switzerland’s multi-generational reliance on Basel’s life-science exports to the massive corporate tax contributions and high-value manufacturing ecosystems that anchor the United States, Germany, and Japan, these twenty-five flagship products serve as vital strategic assets. They draw in immense global capital, directly financing national research infrastructures and solidifying their home countries’ positions in the global knowledge economy. and solidifying their home countries’ positions in the global knowledge economy.

In the pharmaceutical business, Research & Development (R&D) is a high-stakes calculus. Companies invest billions of dollars annually in clinical pipelines, yet the stark statistical reality is that the vast majority of molecules will fail before reaching commercialisation. Yet, when an asset successfully navigates clinical endpoints and captures global medical consensus, it achieves a distinct clinical and economic status—the blockbuster (traditionally defined as generating over $1 billion in annual revenue).

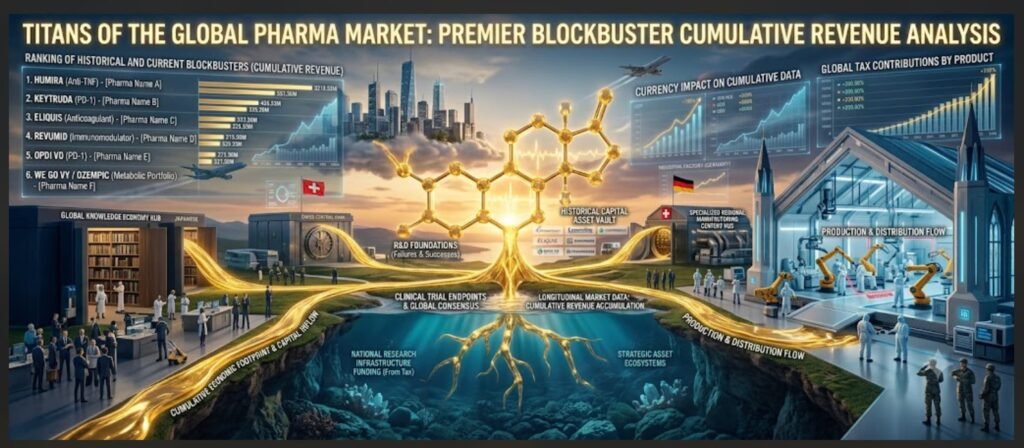

While annual sales charts highlight contemporary commercial growth and expanding indications, assessing a product’s total cumulative revenue from launch till date reveals a different picture. It isolates the few absolute titans of historical and current market volume.

This analysis ranks the premier blockbuster assets of the top 25 pharmaceutical companies globally, based on recent annual corporate disclosures and longitudinal market data through early 2026.

The Lifetime Revenue Leaderboard (Launch to 2026)

The following definitive ranking displays the flagship commercial asset for each of the top 25 pharmaceutical entities, arranged by estimated cumulative gross revenue from its initial global market introduction.

| Rank | Product (Generic Name) | Corporate Anchor | Primary Therapeutic Area | Launch Year | Est. Cumulative Revenue (USD) |

| 1 | Humira (adalimumab) | AbbVie | Immunology (Anti-TNF) | 2003 | $230+ Billion |

| 2 | Keytruda (pembrolizumab) | Merck & Co. (MSD) | Oncology (Anti-PD-1) | 2014 | $155+ Billion |

| 3 | Eliquis (apixaban) | Pfizer / Bristol Myers Squibb | Cardiovascular (Anticoagulant) | 2012 | $115+ Billion |

| 4 | Opdivo (nivolumab) | Bristol Myers Squibb | Oncology (Anti-PD-1) | 2014 | $100+ Billion |

| 5 | Enbrel (etanercept) | Amgen | Immunology (Anti-TNF) | 1998 | $90+ Billion |

| 6 | Stelara (ustekinumab) | Johnson & Johnson | Immunology (IL-12/23) | 2009 | $85+ Billion |

| 7 | Eylea (aflibercept) | Bayer / Regeneron | Ophthalmology (Anti-VEGF) | 2011 | $75+ Billion |

| 8 | Revlimid (lenalidomide) | Celgene / BMS | Oncology (Multiple Myeloma) | 2005 | $70+ Billion |

| 9 | Ocrevus (ocrelizumab) | Roche | Neurology (Multiple Sclerosis) | 2017 | $50+ Billion |

| 10 | Dupixent (dupilumab) | Sanofi / Regeneron | Immunology (IL-4/13) | 2017 | $48+ Billion |

| 11 | Ozempic (semaglutide) | Novo Nordisk | Metabolic (GLP-1 RA) | 2017 | $45+ Billion |

| 12 | Biktarvy (BIC/FTC/TAF) | Gilead Sciences | Virology (HIV) | 2018 | $44+ Billion |

| 13 | Imbruvica (ibrutinib) | AbbVie / Janssen | Oncology (BTK Inhibitor) | 2013 | $42+ Billion |

| 14 | Spikevax (mRNA-1273) | Moderna | Virology (Vaccine) | 2020 | $38+ Billion |

| 15 | Trikafta / Kaftrio | Vertex Pharmaceuticals | Rare Disease (CFTR) | 2019 | $36+ Billion |

| 16 | Entresto (sacubitril/valsartan) | Novartis | Cardiovascular (Heart Failure) | 2015 | $35+ Billion |

| 17 | Tagrisso (osimertinib) | AstraZeneca | Oncology (EGFR Inhibitor) | 2015 | $34+ Billion |

| 18 | Xarelto (rivaroxaban) | Bayer / Johnson & Johnson | Cardiovascular (Anticoagulant) | 2011 | $33+ Billion |

| 19 | Entyvio (vedolizumab) | Takeda | Immunology (Gut-selective) | 2014 | $32+ Billion |

| 20 | Jardiance (empagliflozin) | Boehringer Ingelheim / Lilly | Metabolic (SGLT2 Inhibitor) | 2014 | $30+ Billion |

| 21 | Mounjaro (tirzepatide) | Eli Lilly and Company | Metabolic (GIP/GLP-1) | 2022 | $25+ Billion |

| 22 | Shingrix | GSK | Virology (Vaccine) | 2017 | $22+ Billion |

| 23 | Soliris (eculizumab) | Alexion / AstraZeneca | Rare Disease (Complement) | 2007 | $20+ Billion |

| 24 | Ibrance (palbociclib) | Pfizer | Oncology (CDK4/6 Inhibitor) | 2015 | $18+ Billion |

| 25 | Simponi (golimumab) | Janssen / J&J | Immunology (Anti-TNF) | 2009 | $16+ Billion |

Structural Dynamics of the Lifecycles

Analyzing these 25 assets yields critical strategic insights into contemporary commercial modeling, clinical positioning, and market life cycles.

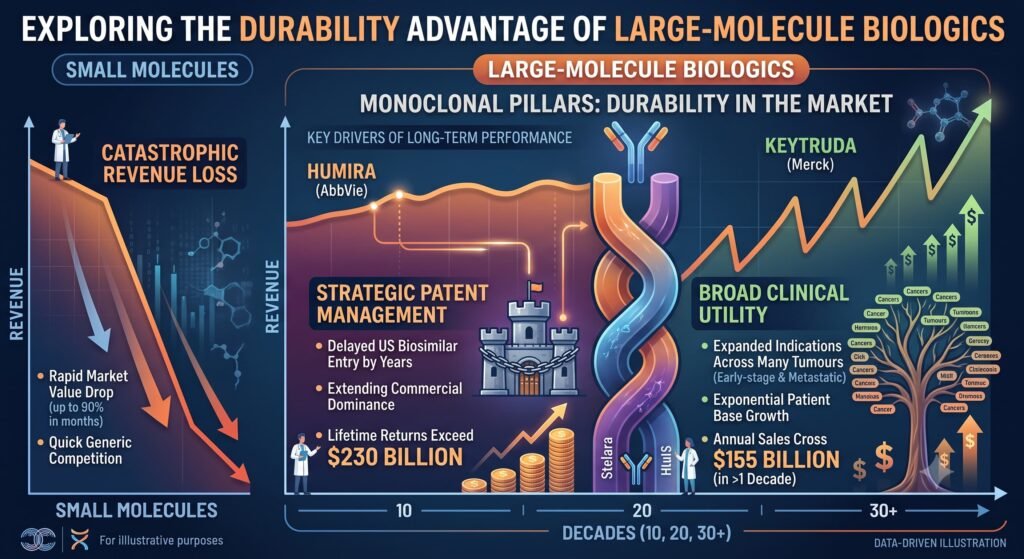

1. The Multi-Decade Monoclonal Pillars

The absolute peaks of the leaderboard—Humira, Keytruda, and Stelara—demonstrate the immense durability of large-molecule biologics. Unlike historical small molecules that faced catastrophic revenue losses of up to 90% within months of patent expiration, complex monoclonal antibodies degrade more gradually.

AbbVie’s strategic management of the Humira patent ecosystem delayed biosimilar entry in the United States for several years, creating a commercial window that pushed its lifetime returns past $230 billion. Similarly, Merck’s Keytruda has capitalised on a broad spectrum of indications across early-stage and metastatic tumours. This clinical positioning has expanded its addressable patient base and accelerated annual sales, bringing them to the $155 billion mark in just over a decade.

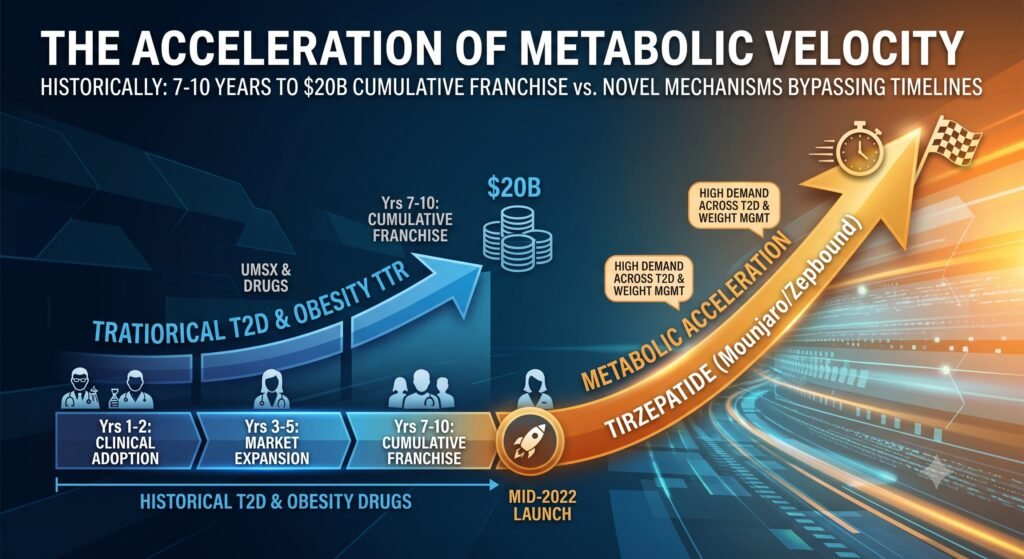

2. The Acceleration of Metabolic Velocity

The entry of Ozempic (Novo Nordisk) and Mounjaro (Eli Lilly) onto this historical list highlights a profound shift in market speed. Historically, building a $20 billion cumulative franchise took a minimum of 7 to 10 years of clinical adoption and market expansion.

Eli Lilly’s tirzepatide (Mounjaro/Zepbound), launched only in mid-2022, has bypassed traditional life-cycle timelines entirely. Driven by high demand across both type 2 diabetes and chronic weight management indications, its trajectory highlights how rapidly a novel metabolic mechanism can achieve systemic market penetration.

3. High-Value Insulation via Orphan and Niche Modalities

Products like Vertex’s Trikafta and Alexion/AstraZeneca’s Soliris illustrate the economic stability of targeted rare-disease therapeutics. By addressing critical therapeutic gaps within small patient populations, these assets face minimal competitive pressure.

This creates sustainable revenue baselines that allow them to match or outpace broad-market small molecules that operate in highly contested therapeutic spaces.

The Strategic Reality: Managing the Patent Cliff

For leadership teams across the global pharmaceutical ecosystem, these historic totals underscore the high concentration of revenue risk inside single-molecule platforms. With a major wave of brand exclusivity expirations scheduled between 2026 and 2030, the primary challenge remains replacing these legacy pillars.

Modern commercial portfolios are balancing these expirations by shifting toward next-generation assets: antibody-drug conjugates (ADCs), radioligand therapies (RLTs), and multi-receptor metabolic co-agonists. These emerging modalities aim to construct the next era of long-term blockbuster lifecycles.

Appendix: Definitive Data Sources and Methodologies

The financial metrics and longitudinal valuations presented in this report are compiled from official corporate disclosures, regulatory filings, and audited annual results:

- AbbVie Inc. Annual Reports (Form 10-K, 2013–2025): Direct tracking of global Humira net sales post-spin-off from Abbott Laboratories; historic baseline consolidated data (2003–2012).

- Merck & Co., Inc. Financial Disclosures (Form 10-K, 2014–2025; Q1 2026 updates): Product-specific revenue tracking for Keytruda (pembrolizumab) oncology extensions.

- Bristol Myers Squibb & Pfizer Inc. Joint Earnings Releases (2012–2025): Reconciled global alliance share records for Eliquis (apixaban) commercial distribution.

- Novo Nordisk A/S Corporate Announcements (Annual Reports 2017–2025): Segment tracking of GLP-1 cardiovascular and metabolic platforms (Ozempic/Wegovy/Rybelsus).

- Sanofi & Regeneron Pharmaceuticals Financial Reporting: Audited joint-venture tracking for Dupixent (dupilumab) global sales across immunology indications.

- SEC Filings & Product Sales Logs: Consolidated data streams from Amgen (Enbrel), Gilead Sciences (Biktarvy), Vertex (Trikafta), and Johnson & Johnson (Stelara/Darzalex).

{kind=link}