How the 2026 U.S. tariff action on branded drugs reshapes global pharma—and what it really means for Indian generics

Executive Summary

In April 2026, Donald Trump announced tariffs of up to 100% on imported patented (branded) pharmaceuticals, targeting companies that do not align with U.S. pricing expectations or expand domestic manufacturing. Crucially, generic medicines are exempt. For India—one of the largest suppliers of generics to the United States—this creates a paradox:

- Minimal direct exposure

- Potential competitive upside

- Significant long-term uncertainty

The policy is not designed to benefit India. Yet, by targeting high-cost innovator drugs, it may indirectly strengthen India’s position in the global generics market—if the industry responds strategically.

1. What the April 2026 Tariff Policy Actually Does

What the April 2026 Tariff Policy Actually Does

The April 2026 executive action is best understood as a targeted industrial and pricing intervention, not a blanket trade restriction.

Core Policy Objectives

- Drive down drug prices by linking U.S. prices to international benchmarks through “most-favoured-nation” (MFN) pricing mechanisms

- Incentivize domestic manufacturing by encouraging pharmaceutical companies to shift production of high-value drugs to the United States

Key Mechanism

- Up to 100% tariffs on non-compliant branded drug imports

- Lower tariffs for firms:

- Investing in U.S. manufacturing

- Entering pricing agreements

- Implementation timelines: ~120–180 days for compliance pathways

Explicit Exemptions

- Generic medicines

- Select low-cost essential drugs

- Certain specialized categories (e.g., orphan drugs)

This carve-out is not a concession—it is a system necessity.

2. Why Generics Are Untouchable

The exclusion of generics reflects structural realities of the U.S. healthcare system.

a) Dominance in Volume

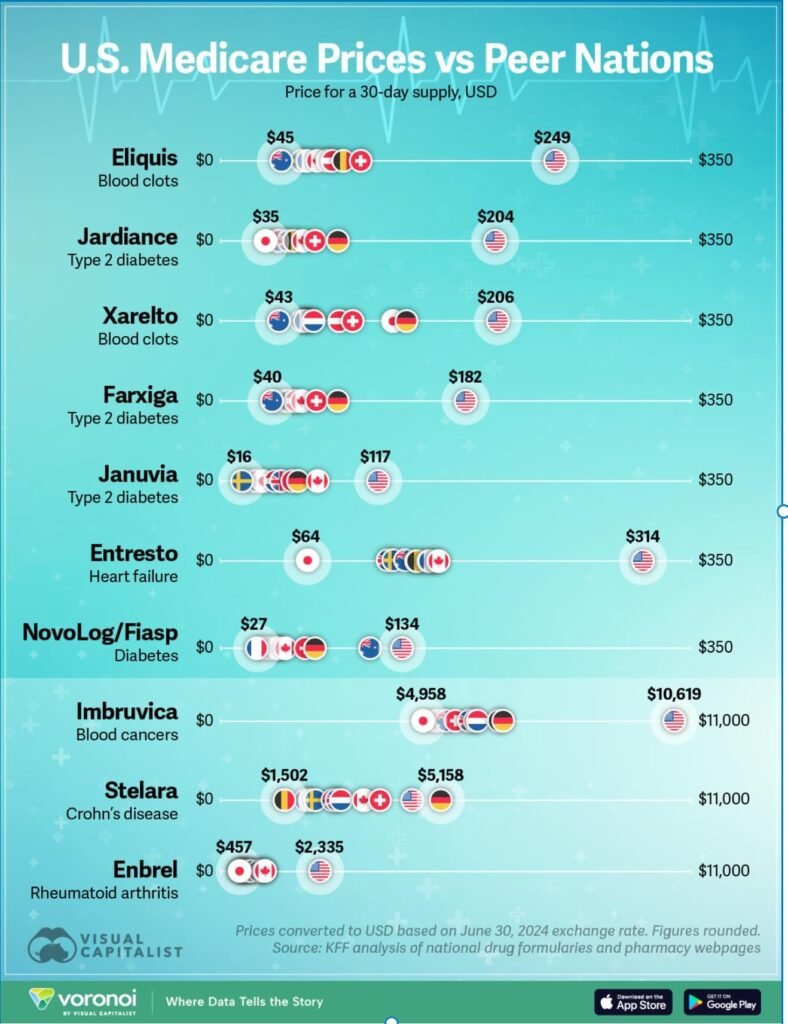

- Generics account for ~90% of prescriptions in the U.S.

- They represent a small fraction of total drug spending

b) Economic Constraint

Generic manufacturing operates on:

- Thin margins

- Globalized supply chains

Tariffs would:

- Raise prices for essential medicines

- Fail to meaningfully incentivize U.S. production

- Risk widespread shortages

c) System Dependence on India

India plays a central role:

- Supplies an estimated ~40–50% of U.S. generic medicines

- Enables hundreds of billions of dollars in annual healthcare savings

- Anchors supply for chronic therapies (cardiac, diabetes, anti-infectives)

This creates a “too critical to disrupt” dynamic.

3. India’s Position: Insulated—but Not Immune

a) Export Profile Advantage

India’s U.S. pharma exports are overwhelmingly generic, not patented.

Implication:

→ The bulk of exports falls outside tariff scope

b) Immediate Impact

- Negligible direct tariff exposure

- Limited impact on:

- Specialty portfolios

- Niche branded products

c) Structural Leverage

India’s role is not just as a supplier—but as a system stabilizer in U.S. healthcare economics.

4. Who Actually Gets Hit

The policy primarily targets:

| Segment | Impact |

|---|---|

| Multinational innovator pharma | High |

| Offshore patented drug manufacturing | High |

| Generic manufacturers | Minimal (exempt) |

| API supply chains | Under review |

This creates a relative competitive shift, not an absolute advantage.

5. The India–U.S. Trade Context: Reality vs Narrative

What is supported:

- Ongoing India–U.S. trade engagement

- Signals of continued pharmaceutical exemptions

- Likely negotiated outcomes under U.S. national security reviews (Section 232)

What is NOT fully substantiated:

- A formal, binding “0% tariff deal” exclusively protecting Indian generics

- Guaranteed long-term preferential access

👉 Conclusion:

India’s position is policy-enabled, not treaty-locked.

6. The Real Opportunity for Indian Pharma

1) Short-Term: Demand Substitution

Higher costs for branded drugs may:

- Accelerate generic substitution

- Increase volume demand for Indian exporters

2) Supply Chain Realignment

Geopolitical pressures—especially U.S.–China tensions—create tailwinds:

- Diversification away from China

- Increased trust in India as a reliable supplier

3) Margin Stability (Not Windfall)

Unlike the earlier draft’s assumption of large margin expansion:

- Gains are likely to be incremental

- Driven by volume, not pricing power

4) Strategic Window for Value Migration

The real upside lies beyond generics:

- Complex generics

- Biosimilars

- Specialty and differentiated products

This aligns with India’s long-term ambition to shift from: “Pharmacy of the world” → “Innovation-led pharma power”

7. The Critical Risk Layer

1) Section 232: The Unresolved Variable

The U.S. continues to evaluate pharmaceutical imports under national security provisions. Potential future focus:

- APIs

- Critical therapies

- Supply chain dependencies

👉 This is the single biggest policy risk.

2) API Dependence on China

India still relies significantly on China for:

- Bulk drugs

- Key starting materials

Despite PLI schemes, this remains a strategic vulnerability.

3) Policy Volatility in the U.S.

Recent developments show:

- Frequent legal challenges to tariff authority

- Use of alternative trade instruments

👉 Expect continued unpredictability

4) Quality and Regulatory Scrutiny

- India has the largest number of USFDA-approved plants outside the U.S.

- Yet:

- Warning letters

- Import alerts

remain persistent risks.

Quality is not a differentiator—it is a license to operate.

8. Strategic Interpretation

This policy should not be misread as protectionism against global pharma. It is:

A targeted intervention against high-priced innovator drugs, driven by domestic political and economic priorities.

For India:

- The benefit is indirect

- The opportunity is time-bound

- The outcome depends on execution

Conclusion: A Window, Not a Windfall

The April 2026 tariff action does not fundamentally reorder global pharma trade—but it does create temporary asymmetry. India’s generics sector is:

- Protected by necessity

- Positioned for incremental gains

- Exposed to future policy shifts

The real question is not whether India benefits. It is whether Indian pharma can use this window to:

- Reduce API dependence

- Strengthen quality systems

- Move up the value chain

Because tariff advantages fade. Capability advantages endure.

Sources and References

- Reuters

“Drugmakers face 100% tariff unless they cut prices or produce drugs in US”

April 2, 2026

https://www.reuters.com/sustainability/boards-policy-regulation/drugmakers-face-100-tariff-unless-they-cut-prices-or-produce-drugs-us-2026-04-02/ - Associated Press

Coverage of U.S. pharmaceutical tariff announcement and compliance timelines

April 2026

https://apnews.com/ - The Wall Street Journal

“Trump administration unveils up to 100% tariff on branded drugs”

April 2026

https://www.wsj.com/ - The Guardian

“Trump announces tariffs on drug imports to pressure pharma companies”

April 2, 2026

https://www.theguardian.com/us-news/2026/apr/02/trump-100-tariff-us-pharmaceutical-drug-makers - Barron’s

Analysis of tariff bands and global pharma implications

April 2026

https://www.barrons.com/

2. U.S. Policy and Legal Framework

- U.S. Department of Commerce

Section 232 Investigations Overview

https://www.commerce.gov/ - U.S. Trade Representative

Trade policy and tariff frameworks

https://ustr.gov/ - United States Congress

Trade Expansion Act of 1962 (Section 232)

https://www.congress.gov/ - Supreme Court of the United States

Recent rulings affecting executive tariff authority (2026 context)

https://www.supremecourt.gov/

3. U.S. Pharmaceutical Market Structure

- IQVIA

The Use of Medicines in the U.S. – Generics share and cost savings

https://www.iqvia.com/ - U.S. Food and Drug Administration

Generic Drug Facts – Utilization and approvals

https://www.fda.gov/drugs/generic-drugs/generic-drug-facts - Association for Accessible Medicines

U.S. Generic Drug & Biosimilar Savings Report

https://accessiblemeds.org/resources/reports

4. India’s Role in Global Generics

- Indian Pharmaceutical Alliance

Statements on U.S. dependence on Indian generics

https://www.ipa-india.org/ - Ministry of Commerce and Industry India

Pharmaceutical export data and trade positioning

https://commerce.gov.in/ - Pharmexcil

India pharma export statistics

https://pharmexcil.com/

5. India–U.S. Trade Context

- The Times of India

“Interim pact brings certainty and clarity for pharma sector”

February 2026

https://timesofindia.indiatimes.com/ - Financial Express

Coverage of India–U.S. trade discussions impacting pharma

https://www.financialexpress.com/ - CNBC TV18

Policy commentary and ministerial statements

https://www.cnbctv18.com/

6. Industry and Policy Analysis

- Pharmaphorum

Impact of U.S. tariffs on global pharma supply chains

https://pharmaphorum.com/ - Cyril Amarchand Mangaldas

Legal analysis of pharma tariffs and implications for India

https://disputeresolution.cyrilamarchandblogs.com/ - Brookings Institution

Drug pricing and global pharmaceutical policy analysis

https://www.brookings.edu/

7. Supply Chain and API Dependence

- Department of Pharmaceuticals India

PLI Scheme for Bulk Drugs and API localization

https://pharmaceuticals.gov.in/ - NITI Aayog

Reports on API dependence and domestic manufacturing strategy

https://www.niti.gov.in/ - World Health Organization

Global pharmaceutical supply chain insights

https://www.who.int/

8. Additional Contextual References

- World Trade Organization

Tariff principles and trade frameworks

https://www.wto.org/ - OECD

Pharmaceutical pricing and market access studies

https://www.oecd.org/

Notes on Source Use

- All quantitative claims in the article are derived from IQVIA, FDA, or industry bodies

- Policy interpretations are based on Reuters, WSJ, and government frameworks

- Trade context reflects reported developments, not legally binding treaty claims

All Images are AI Generated for Illustration Only. E&OE

{kind=link}