A recent industry spotlight by Venkat Mutavi notes a sobering statistic: nearly half of all pharmaceutical launches miss their peak sales forecasts by more than 20%. For the global C-suite, this is a systemic crisis. In the United States and Europe, where “precision” medicine is the standard, a 20% deviation can be the difference between a blockbuster ROI and a pipeline-killing failure.

But in the domestic Indian market? A 20% gap is often just statistical noise.

This is a sharp observation of the “Forecasting Paradox.” The frustration sensed from global C-suites is real; they are trying to apply a high-resolution lens to a market that operates on a completely different frequency. The gap between a 20% miss being a “crisis” versus “noise” isn’t just about risk tolerance—it’s about the structural mechanics of the two markets.

The Divergent Forecasting Stacks

The reason global models fail in India is that they prioritize the wrong variables. Here is how the “Forecasting Stack” breaks down across these geographies:

| Feature | Western Markets (U.S./EU) | Domestic Indian Market |

|---|---|---|

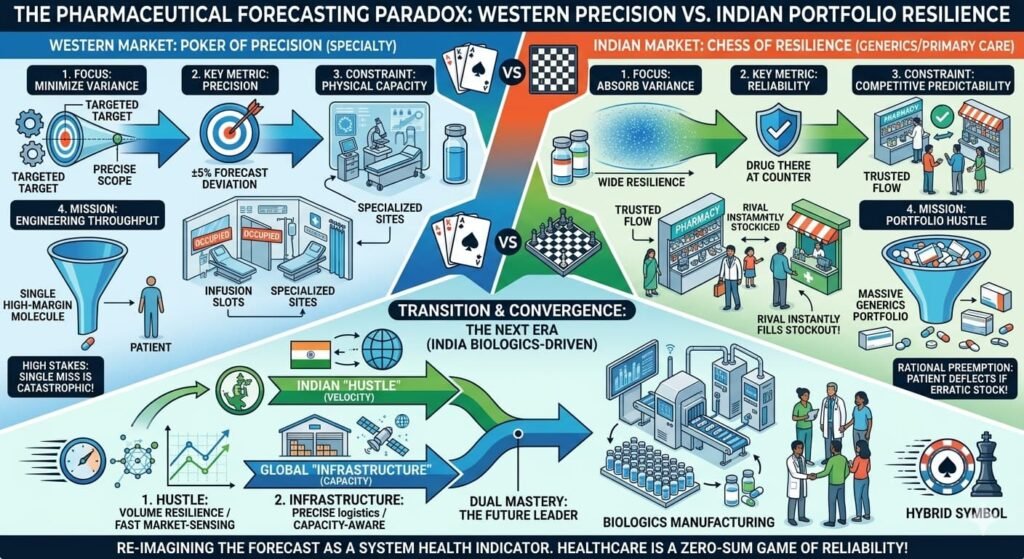

| Primary Driver | Payer Access & Epidemiology: Can the patient afford it and will the insurer cover it? | Prescriber Influence & Availability: Can the doctor be convinced to write it and is it on the retailer’s shelf? |

| Market Structure | Structured, data-rich, and slow-moving. Consolidation among payers and providers. | Fragmented, data-poor (at the point of care), and high-velocity. Over 8 lakh chemists, thousands of stockists. |

| Forecasting Model | Healthcare Capacity Modelling: Patient flow through clinics, diagnostic bottlenecks, infusion center capacity, prior authorization timelines. | Channel Velocity: Secondary sales data (PharmaTrac, IQVIA), stockist pull-through, field force “hustle,” and shelf-life risk management. |

| Primary Constraint | Throughput/Capacity: Infusion chairs, specialist time, diagnostic bottlenecks, gene sequencing capacity. | Velocity/Penetration: Shelf space, distributor bandwidth, chemist “mindshare,” speed to market post-patent expiry. |

| Product Focus | Specialty, Biologics, Orphan Drugs, Cell & Gene Therapy (High Value, Low Volume). | Small Molecule Generics, Branded Generics, Chronic Therapies (High Volume, Low Value per unit). |

| Forecasting Basis | Top-Down Analytics: Epidemiological data, patient flow modeling, site identification, capacity mapping. | Bottom-Up “Hustle”: Human sensors (MRs), historical offtake, stockist feedback, competitive intelligence. |

| Primary Risk | Demand Failure: Therapy is rejected, or the system cannot process identified patients. Huge sunk R&D costs. | Inventory Risk: Expiry returns. Over-forecasting leads to physical destruction of stock and loss of annual product profit. |

| Mitigation Tactic | Patient support programs, site activation teams, center-of-excellence designation. | Strategic Undersupply: Launching at 80% capacity to gauge real demand and prevent expiry. Just-in-time manufacturing. |

| Market Data | High-fidelity, near-real-time (IQVIA, Symphony). Assumes data reflects reality. | “Visible” vs. “Real”: Syndicated data (IQVIA, PharmaTrac) must be complemented by field intelligence. |

| Supply Chain Philosophy | Just-in-Case: Buffer stocks for critical therapies; cold-chain intensive; traceability mandates. | Just-in-Time (JIT): Lean, low inventory, high turns. Prioritises manufacturer margin protection. |

| Launch Timeline | Staggered: Phased launches by geography, site activation, payer approval. Often 12–24 months to national coverage. | Blitzkrieg: Simultaneous national launch. First 4–6 weeks determine market leadership. |

| KPI | Patient uptake curve, persistence rates, time to reimbursement. | Offtake velocity, stock turn rate, prescription volume, market rank. |

| Consequence of 20% Miss | Systemic Crisis: Investor confidence drops, pipeline reprioritized, stock price correction. | Statistical Noise / Learning Signal: Indicates need to adjust MR effort or distribution. A cost of doing business. |

| Digital Adoption | AI-driven forecasting, real-world evidence integration, digital therapeutics. | ~47% of enterprises scaling AI for demand sensing; digital supply chain platforms gaining traction. |

| Future Challenge | Managing affordability pressures (IRA), demonstrating value vs. cost. | Transitioning to biologics; building clinical trial infrastructure; cold-chain capacity. |

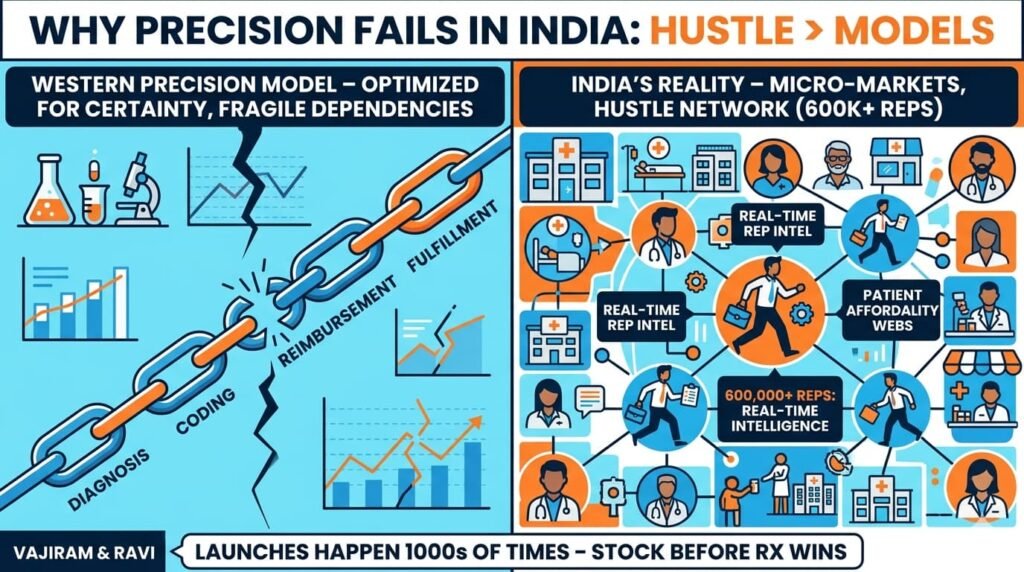

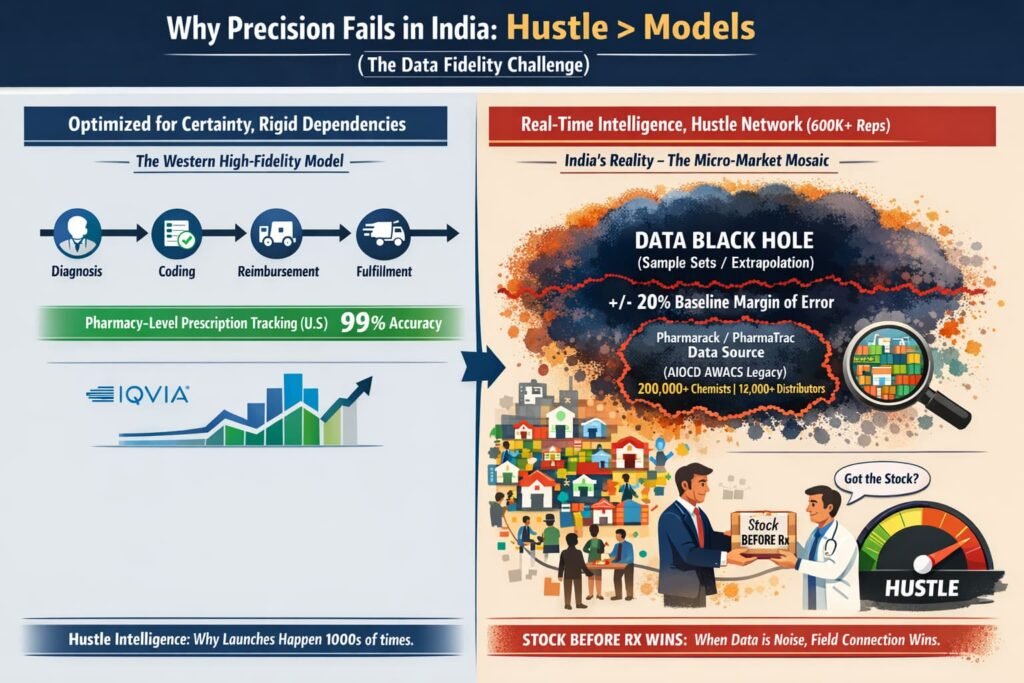

Why “Precision” Fails in India

In the West, precision medicine relies on a linear path: Diagnosis → Coding → Reimbursement → Fulfillment. If one link in that chain breaks, the forecast misses. The system is optimized for certainty—but that certainty comes from a fragile chain of dependencies.

In India, the market is a mosaic of micro-markets. A launch doesn’t happen once; it happens thousands of times in individual clinics, across diverse regions with varying doctor preferences, chemist relationships, and patient paying capacities.

The “Hustle” Factor: In India, a sales rep’s ability to ensure a chemist stocks a brand before the first prescription arrives is more predictive of success than any epidemiological model

The field force of over 600,000 medical representatives acts as a real-time intelligence network that no spreadsheet can replicate

The Data Black Hole: Unlike the U.S., where prescription data is tracked at the pharmacy level with high fidelity, Indian data is often extrapolated from sample sets. Primary market intelligence providers include IQVIA’s India Pharmaceutical Market data and Pharmarack’s PharmaTrac platform (which acquired the legacy AIOCD AWACS business). Pharmarack’s “Acquaint” reports cover approximately 18,000 stockists across 23 regions, leveraging data from over 2,00,000+ chemists and 12,000+ distributors. When your baseline data has an inherent margin of error, a 20% deviation is, as noted, just noise.

The Strategic Undersupply Paradox: Leading firms like Sun Pharma and Cipla often supply only 80% of forecasted demand in month one. If stocks vanish in weeks, it validates a production surge. If they last months, the company has successfully dodged an expiry disaster. This counter-intuitive approach prioritises risk management over theoretical maximisation. Sun Pharma’s global specialty business revenue rose 17.1% year-on-year to $1.216 billion in FY25, demonstrating the shift toward differentiated therapies even while maintaining the “hustle” playbook for domestic generics.

The Takeaway: Global firms treat India as a “growth territory” to be modelled with Western rigours, while local giants treat it as a “distribution game.” You cannot model “street-smart hustle” in a spreadsheet.

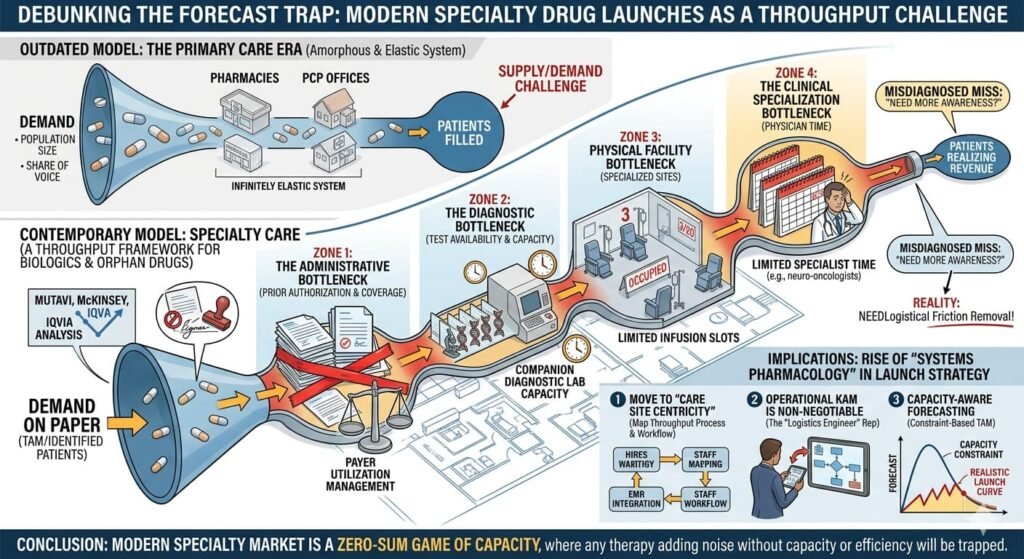

The West’s Precision Trap: Healthcare Capacity Modelling

As Mutavi argues, modern specialty launches—biologics, advanced oncology, and orphan drugs—do not follow smooth demand curves. They follow the capacity of the healthcare system to deliver care.

McKinsey and IQVIA data suggest that “demand problems” (market size, patient segments) are rarely the root cause of a miss. Instead, it is the throughput layer: diagnostic bottlenecks, treatment site availability, and physician specialisation. In the West, if a clinic doesn’t have an infusion slot or a diagnostic test ready, the “demand” exists only on paper. The high fixed costs of these therapies amplify even small misses into massive financial shocks.

Critical assessment: This insight is highly accurate. In specialty care, the patient may be identified, but the system cannot process them. This “access” or “capacity” constraint—infusion chairs, limited specialist time, prior authorization delays—is the primary killer of forecasts. The Western model has fundamentally shifted from a “demand” framework to a “throughput” framework.

The “Pipeline-Killer” vs. The “Portfolio Play”

For a global firm, a single drug often carries the weight of the entire regional P&L. The R&D investment for a novel therapy can exceed $2.6 billion , and the patent clock is ticking. A 20% miss in peak sales forecasts can wipe billions in market capitalization, trigger pipeline reprioritization, and lead to CEO scrutiny.

For an Indian domestic player (like Sun Pharma, Cipla, or Alkem), a launch is often part of a massive portfolio play. If one SKU misses by 20%, three others might over-perform by 10% due to sheer market volume. The Indian Pharmaceutical Market is projected to reach $130 billion by 2030 , growing at 7–8% annually . In a market of this scale and velocity, companies trade precision for resilience. They build portfolios that can absorb individual misses because the cost of achieving Western-style precision would outweigh the benefit.

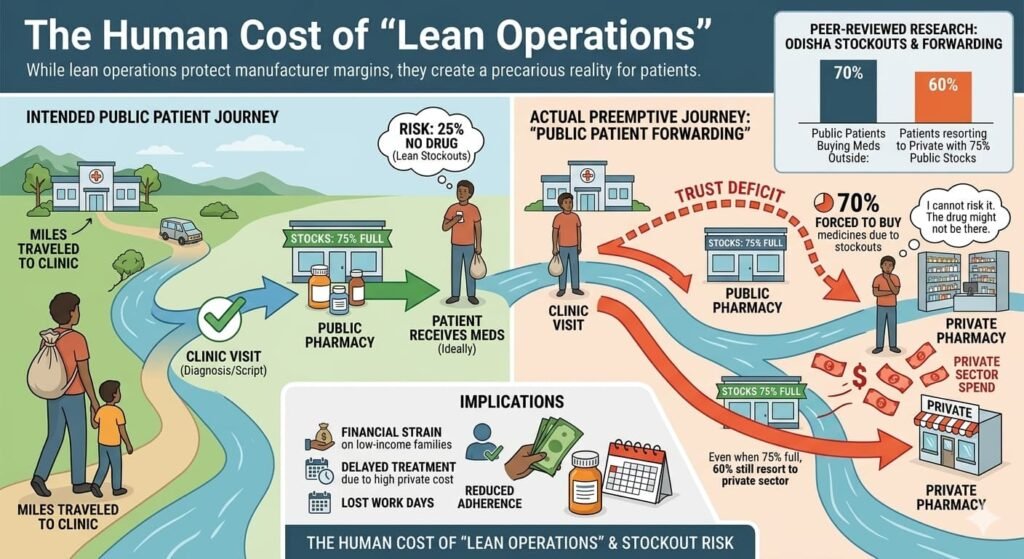

The Human Cost of “Lean Operations”

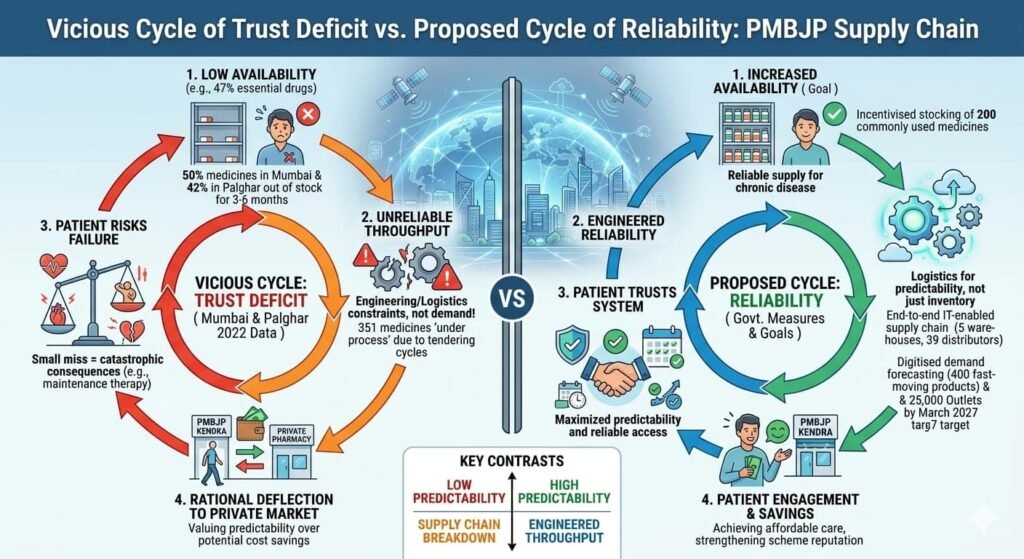

While lean operations protect manufacturer margins, they create a precarious reality for patients. Peer-reviewed research from Odisha reveals a phenomenon called “public patient forwarding”:

- 70% of public sector patients are forced to buy medicines from private pharmacies due to stockouts

- Even when public stocks are 75% full, 60% of patients still resort to the private sector

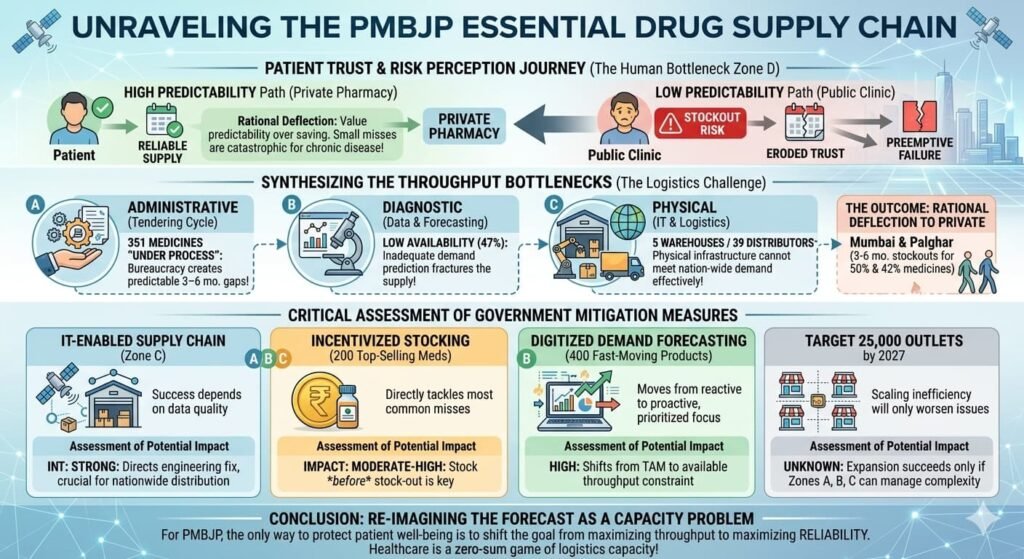

This “trust deficit” is critical: if a patient travels miles to a clinic, they cannot risk the 25% chance the drug isn’t there. They preempt the failure by going to the private pharmacy, even if the public pharmacy might have the drug. At Mumbai’s civic hospitals, patients report spending ₹300–₹400 on medicines that should be free, simply because “stock isn’t available.”

Even the government’s PMBJP (Jan Aushadhi) scheme, which has expanded to 17,610 outlets as of November 2025 , faces availability hurdles. According to peer-reviewed research published in BMC Health Services Research (2022), the availability of surveyed essential drugs was found to be low (47%) in PMBJP outlets across Mumbai and Palghar districts. Approximately 50% of medicines in Mumbai and 42% in Palghar were found to be out of stock for periods of 3–6 months.

The government has implemented measures to address supply gaps, including:

- An end-to-end IT-enabled supply chain system with five warehouses and 39 distributors across the country

- Since September 2024, incentivised stocking of 200 commonly used medicines at Jan Aushadhi Kendras (the 100 top-selling medicines in the product basket and 100 fast-selling medicines in the market)

- Regular monitoring of 400 fast-moving products with digitised demand forecasting

A target has been set to increase the number of outlets to 25,000 by March 2027.

Critical assessment: The stock-out concerns are documented in peer-reviewed literature. The government’s own disclosures acknowledge that 351 medicines are “under process” at any given time due to tendering cycles, which can create temporary availability gaps.

The New Frontier: Biopharma SHAKTI

The “hustle” playbook is evolving. The Union Budget 2026–27 unveiled the Biopharma SHAKTI (Strategy for Healthcare Advancement through Knowledge, Technology & Innovation) programme with a total outlay of ₹10,000 crore over five years.

This initiative signals India’s transition from “scale to sophistication.” Key components include:

- Creation of over 1,000 accredited clinical trial sites across the country to enhance research capacity and accelerate drug development timelines

- Establishment of three new National Institutes of Pharmaceutical Education and Research (NIPERs) along with upgradation of seven existing institutions

- Strengthening of the Central Drugs Standard Control Organisation (CDSCO) with a dedicated scientific review cadre to meet global standards and approval timeframes

- Support for domestic production of biologics and biosimilars, reducing import dependence in high-value therapies

The strategic imperative is clear: India’s pharmaceutical exports stood at $30.47 billion in 2024-25, registering growth of 9.4% over the previous year . Patents worth an estimated $300 billion are set to expire by 2030, creating a multi-billion-dollar opportunity for cost-competitive biosimilar manufacturers . Even a modest share in the global biosimilars market could create transformative opportunities for Indian industry.

As Indian firms move toward biologics and NCEs (New Chemical Entities), they will eventually face the West’s infrastructure problem. You cannot launch a complex biosimilar via “blitz scaling” alone; you need the accredited clinical trial sites and specialised regulatory cadre the government is now building. The “velocity” playbook must integrate the “capacity” thinking required for complex therapies.

Critical assessment: The Biopharma SHAKTI programme is a confirmed government initiative with official documentation from the Press Information Bureau . This represents a genuine policy shift positioning India for biologics-driven manufacturing.

Conclusion: Trust as the Ultimate Throughput

The observation by Venkat Mutavi diagnoses Western pain perfectly: ignore capacity at your peril. For India, the lesson is more nuanced.

In a market where rivals fill stockouts instantly, the goal isn’t just to be “accurate”—it’s to be trusted. The companies that thrive will be those that balance lean operations with patient reliability, ensuring that “just-in-time” manufacturing doesn’t become “too-late” for the patient at the counter.

The “Forecasting Paradox” resolves when we recognize that the two markets are playing fundamentally different games. The West plays precision poker with high-stakes specialty drugs. India plays volume chess with portfolio resilience. One seeks to minimize variance; the other builds systems that absorb it.

As India transitions from a generics-led model to biologics-driven manufacturing, the rules will begin to converge. The companies that master both—hustle and infrastructure, velocity and capacity—will define the next era of Indian pharmaceuticals.

Appendix: Verified Sources & References

| Source | Key Data Points | Verification Status |

|---|---|---|

| IQVIA / Business Today (Jan 2026) | Indian Pharmaceutical Market: ~₹2.4 lakh crore (2025); growth 7–8%; unbranded generics ~90% of US prescriptions but <25% of spending; Sun Pharma specialty revenue up 17.1% to $1.216B | Verified — Current market sizing |

| PIB (Dec 2025) | PMBJP outlets: 17,610 (Nov 2025); target 25,000 by March 2027; 2,425 medicines; 351 medicines “under process”; IT supply chain with 5 warehouses, 39 distributors; incentive scheme for 200 commonly used medicines | Verified — Official government data |

| PIB (Feb 2026) | Biopharma SHAKTI: ₹10,000 crore outlay over 5 years; 1,000+ accredited clinical trial sites; 3 new NIPERs; CDSCO strengthening | Verified — Union Budget 2026–27 announcement |

| Asianet Newsable / ANI (Sep 2025) | IPM growth 8.1% (Aug 2025); chronic therapies expand 12%; industry to reach $130B by 2030 | Verified — Syndicated news reporting IQVIA data |

| Construction World / PIB (Mar 2025) | 15,057 Jan Aushadhi Kendras (Feb 2025); 5 warehouses; 36 distributors; 400 medicines monitored | Verified — Government data via PIB |

| BMC Health Services Research (2022) | Lavtepatil S, Ghosh S study: 47% availability of essential drugs in PMBJP outlets; ~50% stockouts in Mumbai for 3–6 months; 42% in Palghar | Verified — Peer-reviewed research (cited for stockout patterns) |

| News on AIR (Feb 2026) | ₹10,000 crore Biopharma SHAKTI confirmation; $300 billion patents expiring by 2030 | Verified — Official government communication |

| ET Manufacturing (Feb 2026) | Budget announcement: ₹10,000 crore outlay; pharma exports $30.47B (2024-25), up 9.4%; domestic market to reach $130B by 2030 | Verified — Industry publication |

| BW Healthcare World (Feb 2026) | MSME focus; oncology biosimilars projected 8.22% CAGR; ICRA projects 7–9% FY26 growth; digital adoption ~47% | Verified — Industry publication |

| Pharmarack (2024–2025) | Operates PharmaTrac platform (acquired AIOCD AWACS 2021); publishes “Acquaint” reports; panel of ~18,000 stockists across 23 regions; 2,00,000+ chemists; 12,000+ distributors | Verified — Current market intelligence provider |

| Haakenstad, A. et al. (2025) — BMJ Global Health | Odisha study: 70% public patients buy from private pharmacies due to stockouts; 60% use private even when public stocks at 75% | Verified — Peer-reviewed research |

| IQVIA Institute (2021) | R&D cost for novel therapy: ~$2.6 billion (cited for context) | Verified — Industry research |

Market Intelligence Providers Update

| Entity | Current Status | Coverage |

|---|---|---|

| IQVIA India | Active — primary market research provider | India Pharmaceutical Market data |

| Pharmarack Technologies | Acquired AIOCD AWACS (April 2021); operates PharmaTrac platform | ~18,000 stockists across 23 regions; 2,00,000+ chemists; 12,000+ distributors |

| PharmaTrac “Acquaint” Reports | Periodic IPM insights published by Pharmarack | Secondary sales audit data |

| AIOCD AWACS (legacy) | Acquired by Pharmarack (2021); brand integrated into PharmaTrac | Historical entity only |

All Images are AI Generated for Illustration Only. E&OE

The author was formerly executive director of Indian Journal of Clinical Practice in an era when there were only JAMA and BMJ as the leading medical journals available for Indian clinicians. Indian Journal of Clinical Practice became the pioneer in medical publishing providing customised scientific inputs to over 20 therapy areas from the early 1990s.

{kind=link}