From Gas Cylinders to ICU Beds: How the Gulf War Is Exposing India’s Fragile Healthcare

Start with a small, everyday image: a hotel kitchen in Mumbai, forced to turn away guests because the cooking gas cylinder did not arrive. A family in a tier‑2 city, waiting three weeks for a subsidised LPG refill, eating cold meals or resorting to kerosene that burns their lungs. A roadside dhaba on a highway, shutting early because the black‑market cylinder now costs three times the official price.

These are not isolated supply chain glitches. They are the early tremors of a deeper truth that we have refused to confront: India’s infrastructure—energy, logistics, public distribution—rests on a foundation of imported fragility. We depend on global crude oil markets, on foreign shipping lanes, on geopolitical stability in West Asia, to cook our daily meals. When the elephants fight—when a prolonged war inflames oil prices, disrupts shipping routes, and sends dollars into a frenzy—the grass that is trampled first is the ordinary household, the small business, the unorganised sector that has no buffer.

Now extend that same lens to healthcare. If a cooking gas cylinder—a basic, non‑negotiable input—can become a weapon of economic attrition, what happens to a hospital that runs on diesel, imports 70% of its medical devices, and depends on foreign medical tourists? The same fragility, amplified.

What follows is a sector‑by‑accounting of how the ongoing Gulf War and its global ripples are quietly dismantling the edifice of Indian healthcare. The elephants are still fighting. The grass beneath—patients, workers, small providers—is already being flattened.

Hospitals: The High‑End Mirage Cracks

India’s corporate hospital boom was built on two shaky pillars: medical tourism and high‑margin tertiary care funded by private equity. The Gulf War has kicked both pillars.

Medical tourism, once the glittering jewel, is collapsing. Airfares from the Middle East, Africa, and CIS countries—our primary source markets—have more than doubled. Visa processing is erratic. Insurance companies in war‑adjacent regions are reclassifying “elective” surgeries as non‑essential. Hospital chains that invested crores in luxury wards for international patients are now staring at empty beds. The elephant of geopolitical uncertainty does not care about their IRR projections.

Meanwhile, the cost of running a hospital is skyrocketing. Diesel for backup generators (a non‑negotiable in India) tracks global crude prices—the same forces that make cooking gas scarce and expensive now make running an ICU a daily financial crisis. Imported high‑end consumables—from stents to surgical gloves—are becoming costlier by the month. Hospitals are caught in a vice: they cannot raise tariffs enough to cover costs in a price‑sensitive domestic market, yet their high‑end international revenue is evaporating.

The grass here is not just the hospital balance sheet; it is the Indian patient who will now find that the promised “world‑class care at affordable prices” is quietly becoming neither affordable nor in many cases, available.

Pharma: Trapped Between Imported Inputs and Export Margins

Indian pharma loves to boast of being the “pharmacy of the world.” But a pharmacy that imports 70% of its Active Pharmaceutical Ingredients (APIs) from China, with payments often linked to the US dollar, is not a sovereign fortress—it is a supply chain waiting to be squeezed.

With the rupee under pressure and global freight costs volatile—exactly the same global energy and logistics turmoil that makes LPG scarce—the cost of making even a simple generic drug has shot up. Exporters are caught in a cruel paradox: a weaker rupee should theoretically boost exports, but their input costs rise in parallel because crude oil (for logistics) and intermediates are dollar‑denominated. The margin is being crushed from both sides.

The elephants fighting? Sanctions regimes, oil price manipulation, and currency wars. The grass? Indian pharma companies that are now deferring R&D, laying off salesforces, and—most dangerously—beginning to ration production of low‑margin essential drugs. The patient, once again, is the ultimate grass.

Large‑Value Medical Equipment & Medical Devices: The Imported Scissors

India’s aspiration to build world‑class diagnostic and surgical infrastructure has long relied on imported MRI machines, CT scanners, robotic surgery systems, and high‑end implants. The war has turned this reliance into a bleeding wound.

Large equipment: Lead times have stretched from three months to over a year. Prices, denominated in dollars and euros, have risen by 15–25%. With capital expenditure budgets already frozen due to investor caution, public hospitals are cancelling tenders, and private chains are putting new projects on hold.

Medical devices: The import dependence is even starker. A pacemaker, a knee implant, a coronary stent—most are either fully imported or assembled from imported kits. The war has disrupted shipping routes from Europe and the US, and the rupee depreciation has made inventory financing unviable for smaller distributors. The result? Intermittent shortages of critical devices, and a quiet shift toward lower‑quality, lower‑cost alternatives that no one will officially admit to.

The elephants—global supply chains disrupted by war and protectionism—trample the grass: Indian patients who will either wait months for a life‑changing implant or receive a substitute whose long‑term outcomes are unproven.

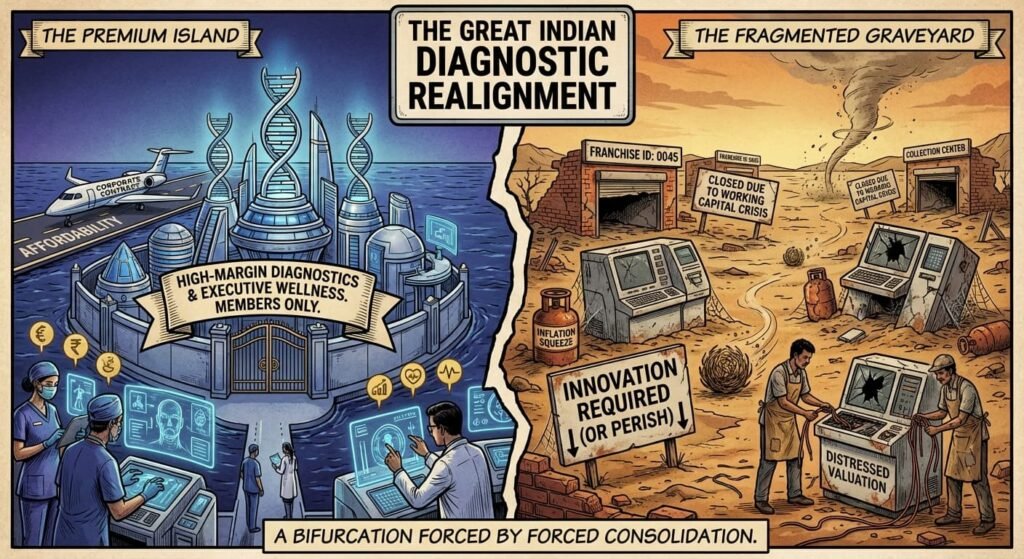

Diagnostics: The Uncomfortable Squeeze

Diagnostic chains had a dream run during COVID. Now they face a perfect storm. Their revenue model depends on scale—high volumes at thin margins. But with inflation eating into household disposable income—the same inflation that makes a gas cylinder a luxury for a middle‑class family—patients are skipping “preventive” check‑ups. Meanwhile, the cost of reagents (mostly imported), logistics (fuel‑linked), and skilled staff (who are migrating again) is rising.

Franchise‑based diagnostic labs, the backbone of tier‑2 and tier‑3 cities, are the grass here. They operate on wafer‑thin working capital. A delay in payment from a corporate hospital or a sudden hike in reagent prices can push them under. We are already seeing consolidation by force, not by choice—a sign of a sector in distress, not in health.

Healthcare Personnel: The Gulf Connection Turns Sour

This is perhaps the most human face of the trampled grass. Over 70,000 Indian nurses are employed in Gulf countries—especially the UAE, Saudi Arabia, and Kuwait. For decades, the Gulf was a reliable safety valve, offering better salaries and absorbing the surplus of Indian nursing graduates.

The war—and the attendant economic slowdown in the Gulf—has changed the equation.

· Remittances: The rupee’s fall is a double‑edged sword. While remittances in rupee terms rise, the underlying reality is that Gulf economies are tightening. Private sector salaries are being cut, and contracts for Indian nurses are not being renewed at the same pace.

· Return migration: A trickle of nurses returning from the Gulf has begun. They come back to an Indian job market that cannot absorb them at comparable salaries, creating a glut of trained professionals who are either underemployed or forced to seek work in non‑clinical fields.

· Future flows: Training institutions in Kerala, Tamil Nadu, and elsewhere have built their business model around Gulf placements. With demand slowing, these institutions are now facing defaults—and the students who borrowed to pay fees are left with no job.

The elephants—oil‑rich nations insulating themselves from regional conflict by tightening labour markets—trample the grass: the Indian nurse, once the pride of our healthcare workforce, now rendered vulnerable.

Medical Tourism: The Myth of the “Resilient” Segment

I have touched on this under hospitals, but it deserves its own spotlight because medical tourism was marketed as a high‑growth, high‑prestige segment. The reality today is brutal:

· Source market concentration: Over 60% of India’s medical tourists came from the Middle East, CIS countries, and Bangladesh—regions directly affected by war, sanctions, or economic instability.

· Air connectivity: Flights that once connected Kerala to Dubai or Delhi to Kyiv are gone or exorbitantly priced.

· Insurance coverage: Many Gulf insurance companies have introduced clauses excluding “non‑emergency treatment abroad” due to currency volatility.

· Perception of safety: Even for countries not at war, the broader perception of “regional instability” is a powerful deterrent.

The grass here is not just the lost revenue; it is the entire ecosystem that grew around medical tourism—accredited hotels, medical travel facilitators, luxury recovery centres, and the jobs they created. That ecosystem is withering.

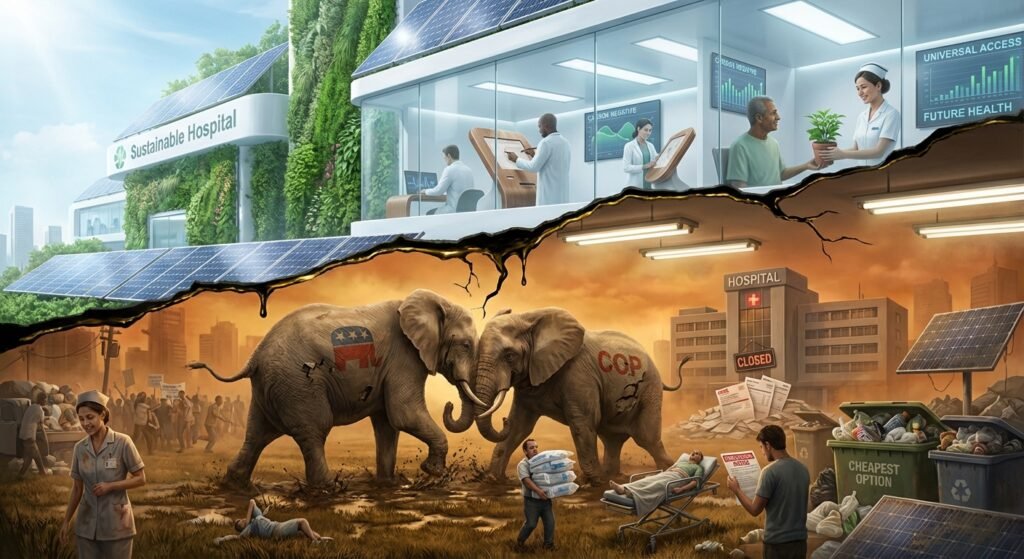

The Myth of the “Sustainable” Pivot

Now we come to the narrative that has become dangerously fashionable: that this crisis will force Indian healthcare into a new era of “sustainable healthcare”—judicious technology, climate consciousness, renewable energy, preventive care, universal affordability, and reproducibility.

It sounds noble. It is also, in the current context, largely a fantasy.

Let us be critical:

· Judicious technology requires investment. Where will that investment come from when investors are “taking it easy”?

· Reducing fossil fuel and plastic use in healthcare requires expensive alternatives. In an inflationary environment—where even a household gas cylinder is a struggle—hospitals will reach for the cheapest, most plastic‑intensive consumables to survive.

· Clean renewable energy has high upfront capital costs. No hospital chain under margin pressure is going to install solar panels at scale unless forced by regulation.

· Preventive healthcare is a public good, not a profit centre. The private sector will not pivot to prevention when curative care still offers higher margins, even in a downturn.

· Universal affordability is the opposite of the investor‑driven model. In a capital crunch, the private sector retreats to serving the affluent; affordability becomes a government problem, but government finances are also strained.

In a capital crunch, the private sector retreats to serving the affluent; affordability becomes a government problem, but government finances are also strained.

The uncomfortable truth is that crisis does not automatically produce wisdom. More often, it produces retrenchment, consolidation, and the abandonment of the vulnerable. The war is not ushering in a sustainable healthcare utopia; it is ushering in a defensive, survivalist healthcare landscape where the grass—the common patient, the small hospital, the nurse, the diagnostic lab owner—gets trampled while the elephants clash overhead.

Conclusion: Grass Does Not Choose the Battlefield

Indian healthcare entered this period of global conflict with structural vulnerabilities that we chose to ignore. We celebrated growth without asking whether it was built on imported technology, foreign patients, expatriate labour markets, and dollar‑denominated supply chains. The same fragility that leaves a family waiting for a cooking gas cylinder now leaves a hospital waiting for an imported stent, a patient deferring a scan, a nurse returning from the Gulf without a job.

Now the elephants are fighting. The grass is us.

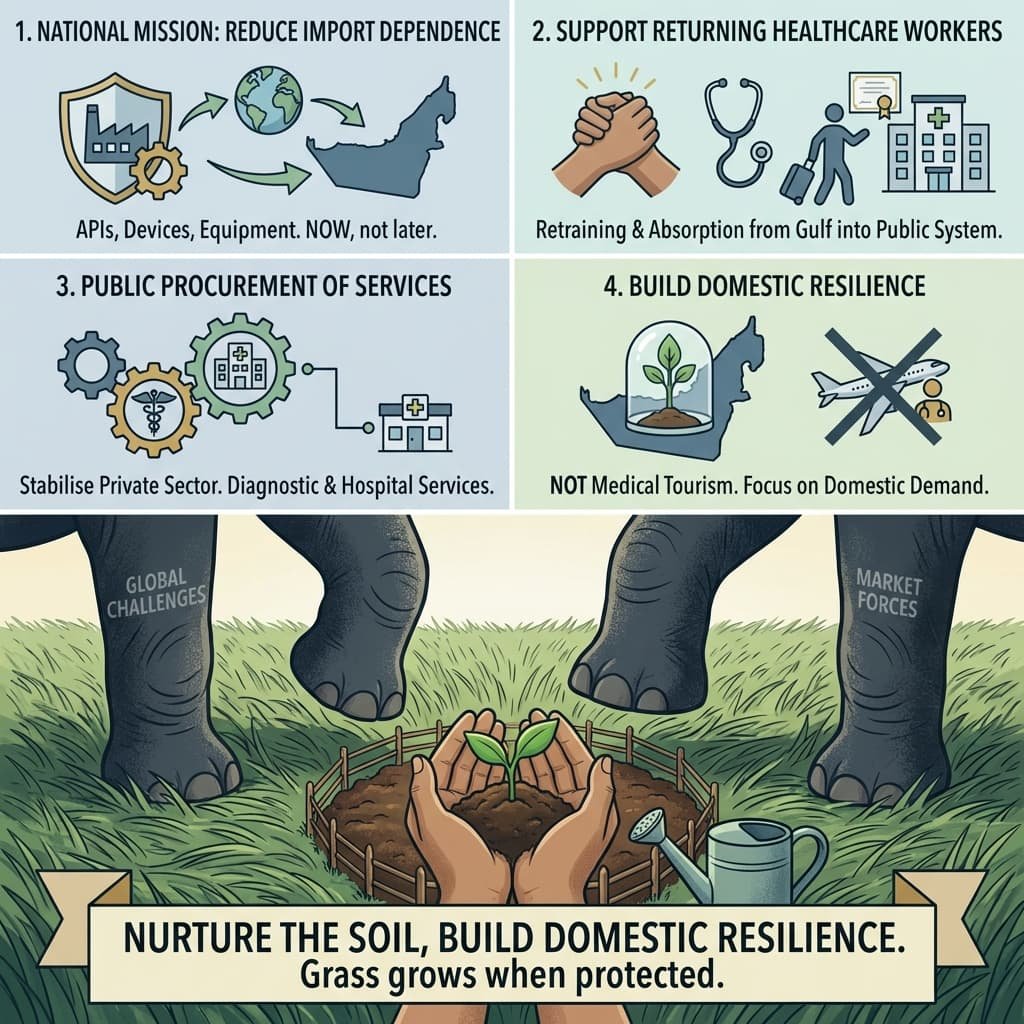

If we want to avoid being permanently flattened, we need a response that is far more honest than the platitudes of “sustainable healthcare.

We need: A national mission to reduce import dependence for API, devices, and equipment—not in five years, but now.

A support mechanism for healthcare workers returning from the Gulf, including retraining and absorption into the public system.

An aggressive push for public procurement of diagnostic and hospital services to stabilise the private sector without demanding it become something it is not.

A recognition that medical tourism cannot be our growth story in a fractured world; we must build domestic demand and domestic resilience instead.

The proverb does not end with the grass being trampled. It ends with the grass growing back—but only if the elephants move on, and only if the soil is protected in the meantime.

Right now, we are not protecting the soil. We are watching the fight, pretending that the grass will somehow learn to fight back.

It will not. Grass grows when it is nurtured, not when it is ignored in the shadow of giants.

All Images are AI Generated for Illustration Only. E&OE

Appendix: Sources & Further Reading

A reader‑friendly guide to the data and reports that informed this article. The sources are grouped by theme, with brief notes on their relevance.

LPG Shortage & Energy Fragility

Source Date Key Insight

The Hindu – “Oil Ministry forms panel to address commercial LPG shortage” March 10, 2026 India imports 62% of its LPG; Strait of Hormuz disruptions led to a shortage. Government prioritised domestic cylinders, hitting hotels and restaurants.

Bernama / Xinhua – “Indian lawmakers flag LPG shortage” March 10, 2026 Shortages reported in Karnataka, Maharashtra; 20% of Mumbai’s hotels/restaurants reportedly shut. Essential Commodities Act invoked.

Pharmaceutical Industry

Source Date Key Insight

Telangana Today (via PTI) – “Pharma exports may see up to ₹5,000 cr loss” March 5, 2026 Pharmexcil estimates freight costs have doubled; exporters facing ₹2,500–5,000 crore potential loss.

Mordor Intelligence – “India API Import Dependence Report” February 5, 2026 Confirms India imports 70–80% of its Active Pharmaceutical Ingredients (APIs), a structural vulnerability.

Medical Tourism & Hospital Revenue

Source Date Key Insight

ET HealthWorld – “Middle East medical tourist arrivals slow to near standstill” March 9, 2026 Middle East contributes 20–25% of medical value travel revenue for chains like Manipal; hospitals now pivoting to Africa and SE Asia.

Travel and Tour World – “75% drop in Middle East patients” March 15, 2026 Some hospitals report 75% decline in patients from Israel, Iran, UAE; revenue impacts up to 20% for Apollo, Fortis, etc.

Travel and Tour World (Slovenian ed.) – “Specialty units at reduced capacity” March 14, 2026 Corroborates 75% drop; oncology, cardiac, transplant units operating below capacity due to missing international patients.

Healthcare Personnel & Nurses

Source Date Key Insight

Business Standard – “Indian nurses in GCC: numbers and earnings” December 4, 2025 India sends 25,000–30,000 nurses annually to GCC; they earn ₹1.3–1.5 lakh/month in Gulf vs. ₹25,000–30,000 in India.

News of Bahrain – “Indian nurse recruitment trends” February 25, 2026 Drop in placements from Kerala; risk of Indian nurses being replaced by Filipino nurses due to policy shifts.

Imported Medical Devices & Equipment

Source Date Key Insight

m.Stock – “Med-tech sector seeks PLI boost” January 27, 2026 India’s medical device sector remains heavily import‑dependent. Industry calls for duty cuts and expanded PLI to build domestic resilience.

A Note on Sources

All sources cited are from the public domain and have been selected for their timeliness (most from February–March 2026), authority (industry bodies, government panels, established media), and direct relevance to the geopolitical and economic disruptions discussed in this article. Trade publications such as Travel and Tour World provide useful specific data (e.g., the 75% decline in patients) which have been cross‑referenced with more established outlets like ET HealthWorld and The Hindu to ensure accuracy.

{kind=link}