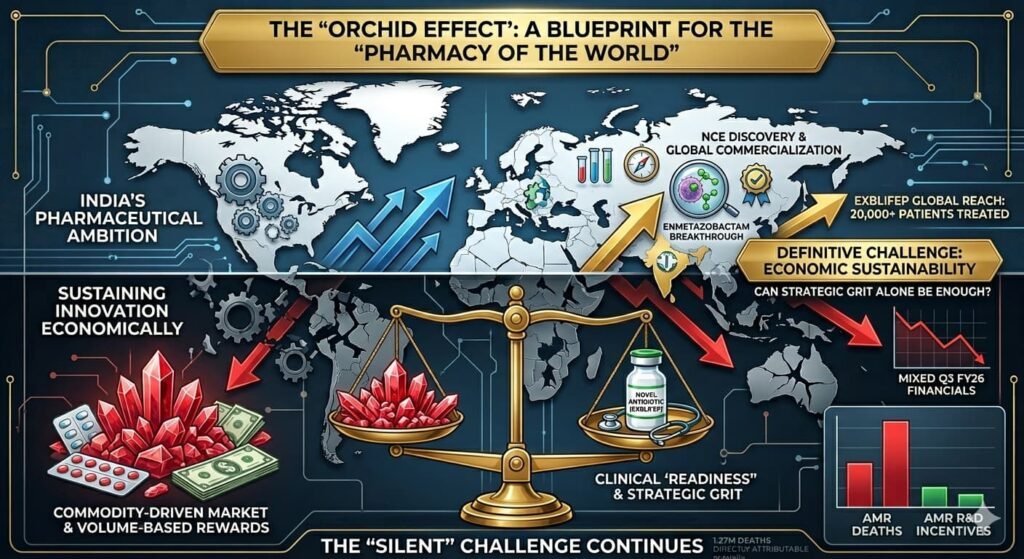

Opening Frame: The “Silent” Pandemic Meets Strategic Grit

In the world of high-stakes pharma, oncology and gene therapy command the headlines. Yet, the real battlefield is microscopic and increasingly resistant. Antimicrobial Resistance (AMR) is no longer a “future threat”—it is a present-day crisis contributing to nearly 5 million deaths annually.

Amidst this, Orchid Pharma has emerged as a rare protagonist: an Indian firm that transitioned from the brink of insolvency to global innovation. But as this case study reveals, scientific success is only half the battle; the “broken” economics of antibiotics remains the ultimate hurdle.

Executive Summary

Orchid Pharma’s journey—from cephalosporin dominance to IBC insolvency to an innovation-led revival under the Dhanuka Group—is one of the most significant turnarounds in Indian pharma.

- The Breakthrough: Enmetazobactam (part of Exblifep), approved by the US FDA and EMA in 2024.

- The Scale: As of early 2026, Exblifep has been used to treat over 20,000 patients globally.

- The Strategic Shift: Moving from a “commodity” API player to a “backward-integrated innovator.”

Part I: The Strategic Bet and the “Allecra” Model

Orchid’s foundation was built on vertical integration. However, its defining move was the 2008 discovery of enmetazobactam, a novel beta-lactamase inhibitor.

To manage the crushing costs of global trials, Orchid employed Strategic Optionality:

- Out-licensed the molecule to Allecra Therapeutics (Germany).

- Enabled external funding for Phase III trials, de-risking the balance sheet.

- Retained long-term rights, which allowed for a full “repatriation” of the molecule in 2025.

Part II: The 2026 Pivot — From Import Dependence to Self-Reliance

Orchid’s current strategy is defined by two pillars: Innovation and Sovereignty.

1. The Kathua Milestone (March 2026)

In March 2026, the foundation stone was laid for Orchid’s ₹600–700 crore fermentation-based 7-ACA plant in Jammu.

- Significance: 7-ACA is the key starting material (KSM) for cephalosporins. India currently relies heavily on Chinese imports for this.

- Impact: This PLI-backed facility is the first of its kind in India, aimed at making Orchid (and India) immune to global supply chain shocks.

2. Portfolio Diversification: The “Cefiderocol” Factor

Orchid has moved beyond a single-molecule story. Through a technology transfer pact with Shionogi and GARDP, Orchid is now positioned as a global manufacturer for Cefiderocol, a “Trojan Horse” antibiotic for ultra-resistant pathogens.

Part III: Clinical Utility vs. Competitive Reality

Exblifep (cefepime–enmetazobactam) is clinically positioned as a carbapenem-sparing therapy.

| Feature | Exblifep (Orchid) | Avycaz (Ceptazidime-Avibactam) |

| Primary Target | ESBL-producing pathogens | KPC, OXA-48, Pseudomonas |

| Positioning | Sparing Carbapenems | Salvage therapy for CRE |

| Real-World Use | 20,000+ patients (April 2026) | Standard of care for CRE |

Part IV: The Core Problem — Antibiotic Economics

Despite the 2024–2026 milestones, Orchid faces a structural tension. The very nature of antibiotics works against traditional business models:

- Stewardship Restriction: Unlike a “blockbuster” statin, a successful new antibiotic is reserved for the sickest patients to prevent resistance. Success = Lower Volume.

- Price Erosion: Legacy API segments (still roughly 70% of revenue) face intense pricing pressure.

- The “Value” Gap: As of early 2026, the US PASTEUR Act and the UK’s subscription model (paying for “readiness” rather than volume) are still in trial or legislative phases, leaving innovators in a commercial limbo.

Part V: Financial Reality Check (Q3 FY26)

Profitability remains the “final frontier.” Recent filings for the quarter ending December 2025 (Q3 FY26) showed:

- Consolidated Net Loss: ~₹12.6 crore (compared to a profit in the previous year).

- Pressure Points: Higher costs associated with the Global Rights Repurchase from Allecra and initial capital outlays for the Jammu 7-ACA project.

- Market Sentiment: The stock has seen volatility, reflecting investor caution regarding the long gestation period of innovation-led returns.

Conclusion: A Blueprint for the “Pharmacy of the World”

Orchid Pharma in 2026 is a microcosm of India’s pharmaceutical ambition. It has proven that an Indian company can discover and commercialize a New Chemical Entity (NCE) globally.

The question for the next decade is no longer “Can we innovate?” but “Can we sustain innovation?” Orchid’s success in 2026 hinges on whether the global healthcare system begins to value “antibiotic readiness” as much as it values “cancer cures.”

Appendix: Key Sources & References (2026 Context)

- Global AMR Burden: WHO Global Surveillance Report (GLASS, 2025/26) – Data on 1 in 6 resistant infections.

- Manufacturing Milestones: Press Release (March 2026): Foundation stone ceremony for 7-ACA fermentation plant, Kathua, J&K.

- Financials: Orchid Pharma Q3 FY26 Earnings Transcript (Feb 2026): Discussion on gross margins (31%) and Russian market impacts.

- Strategic Pacts: GARDP/Shionogi Tech Transfer Agreement (2024-2026 updates): Manufacturing licenses for Cefiderocol in 135 countries.

- Clinical Adoption: Internal Company Estimates (April 2026): Global patient reach of Exblifep surpassing 20,000 treatments.

- Policy Environment: Contagion Live (Feb 2026): Status of the PASTEUR Act reintroduction in the US Congress.

- Why the World Still Doesn’t Celebrate Antibiotic Breakthroughs like Zaynich https://medicinman.net/2026/02/why-the-world-still-doesnt-celebrate-antibiotic-breakthroughs-llike-zaynich/ via @medicinman-editorial

All Images are AI Crafted for Illustration Ony. E&OE

{kind=link}