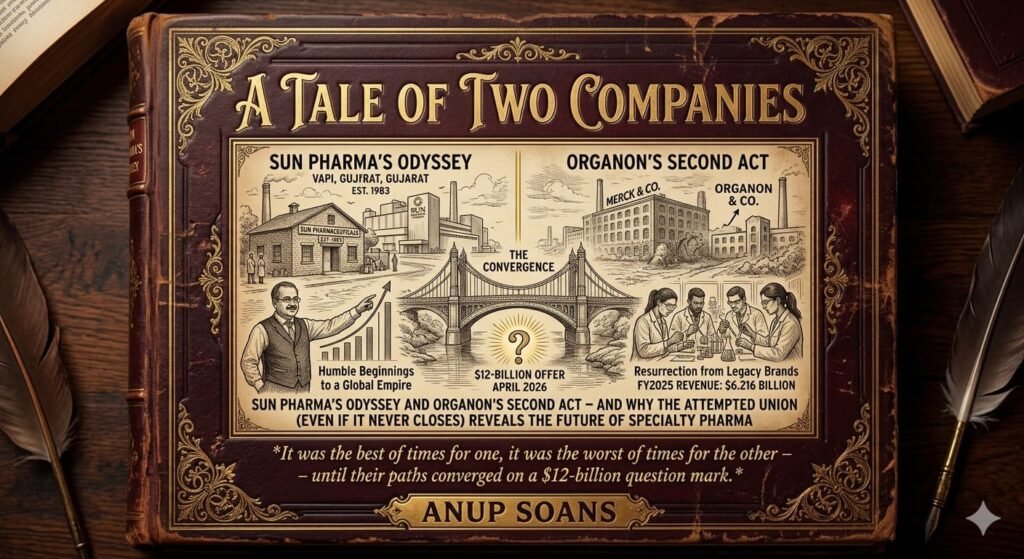

Sun Pharma’s Odyssey and Organon’s Second Act – And Why the Attempted Union (Even If It Never Closes) Reveals the Future of Specialty Pharma

It was the best of times for one, it was the worst of times for the other – until their paths converged on a $12-billion question mark.

Prologue: Two Origins, One World

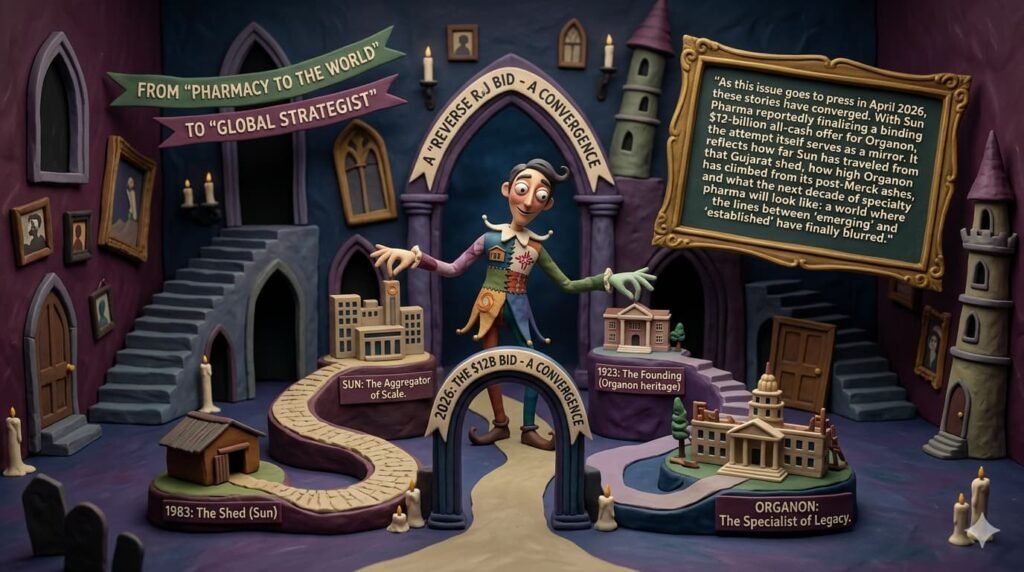

From a two-person startup in a Gujarat shed to one of the world’s largest specialty generics players, Sun Pharmaceutical Industries Ltd. has scripted one of India’s most remarkable growth stories. Founded in 1983 by Dilip Shanghvi, the company has grown through deliberate “delta moments”: strategic pivots, bold acquisitions, and portfolio shifts that redefined global scale.

On the other side of the world, another story was unfolding. Organon & Co., born from the vaults of Merck & Co. (MSD), carried a heritage stretching back to the 20th century’s breakthroughs. But by 2021, it was a cast-off: a collection of off-patent brands and women’s health assets Merck no longer wanted. Investors yawned. Then something unexpected happened.

led, how far Organon has climbed from its ashes, and what the next decade of specialiAs this issue went to press in April 2026, these stories converged. Sun Pharma was reported to be finalizing a binding $12-billion all-cash offer for Organon. Whether the deal closes or not, the attempt itself is a mirror: it reflects how far Sun has traveled, how far Organon has climbed from its ashes, and what the next decade of specialty pharma will look like.

Part One: Sun Pharma – The Outsider Who Built an Empire

1983–2009: From Vapi to Detroit

Sun Pharma began in 1983 with five psychiatry products. The first major diversification came in 1988 with cardiology, followed by a 1994 IPO that was oversubscribed 55 times. The decisive international “delta” arrived in 1997 with the acquisition of Caraco Pharmaceutical Laboratories in Detroit—Sun’s first US foothold. By 2007, the demerger of SPARC signaled that Sun was no longer content being a pure-play generics firm.

2010–2015: The Scale Game-Changers

The 2010 acquisition of a controlling stake in Taro Pharmaceuticals brought dermatology expertise and a branded-generics platform. This was followed by the era-defining 2014 move: the $4-billion acquisition of Ranbaxy Laboratories. Overnight, Sun became India’s largest pharma company and a global top-five player, proving its ability to absorb massive, complex entities despite regulatory headwinds.

2016–2026: The Specialty Pivot

Post-Ranbaxy, Sun pivoted toward high-margin branded specialty products like Ilumya (psoriasis) and Cequa (dry eye). Recent precision tuck-ins, including Concert Pharmaceuticals (2023) and Checkpoint Therapeutics (2025), filled gaps in alopecia and immuno-oncology. By early 2026, with a market cap exceeding $44 billion, Sun had the firepower but lacked a massive, physician-driven flagship portfolio.

Part Two: Organon – The Distinguished House That Merck Discarded

2021: The Spinoff – A Second Act No One Expected

In June 2021, Merck spun off Organon & Co. with a portfolio dismissed as a “legacy grab bag.” It debuted on the NYSE with $9 billion in debt and a collection of women’s health assets (Nexplanon, NuvaRing) and established brands (Singulair, Cozaar). Wall Street predicted annual revenue erosion of 3-5%.

2022–2025: The Resurrection and Transition

Under the initial leadership of veteran Kevin Ali, Organon executed a quiet turnaround. Instead of declining, it stabilized. Ali’s team used cash flow from mature brands to fund a digital fertility platform and to expand the biosimilars pipeline through Samsung Bioepis.

By the time Ali stepped down in October 2025, Organon had proved the skeptics wrong. While the company was under interim leadership as of early 2026, it reported FY2025 revenue of $6.216 billion. It had pared debt down to approximately $8.0 billion and showed double-digit growth in biosimilars. The “discarded” assets had become a lean, cash-generating specialty machine.

Part Three: The Convergence – Why Organon Fits Sun’s Playbook

As of April 10, 2026, Sun Pharma is reportedly finalizing its $12-billion bid. Here is the strategic logic:

| Sun’s Historic Pattern | How Organon Matches (2026 Data) |

| New Specialty Verticals | Women’s health and fertility are new to Sun; Organon offers instant #1 global leadership. |

| Branded Revenue Streams | Organon’s $6.2B revenue is 74% ex-US, matching Sun’s global infrastructure. |

| Scale Advantage | A $12B all-cash bid requires a fortress balance sheet; Sun is one of the few to have it. |

| Margin Expansion | Organon’s specialty portfolio carries margins (60-80%) far above commoditized generics. |

For Organon, this is a homecoming. Sun’s manufacturing prowess could revitalize Organon’s legacy brands in emerging markets, while Sun’s specialty R&D provides a path forward for Organon’s late-stage assets.

Part Four: The Vulnerabilities

The Financial Strain: A $12-billion acquisition would be Sun’s largest ever. Investor skepticism is already visible, with Sun’s stock dipping 4-5% on news of the binding bid. Markets worry about the $8 billion in legacy debt Sun would inherit.

Integration Risk: Organon is currently in a leadership transition. Integrating a US-listed company with Merck-legacy processes into Sun’s promoter-led, execution-heavy culture will be the ultimate test of Dilip Shanghvi’s “hands-off” management model.

Epilogue: Why This Tale Matters

The Organon bid—whether it closes or is outbid by global suitors—reveals Sun’s diagnosis of the future: Generics alone are no longer enough. To compete globally, Sun needs scale in specialty categories that are physician-protected and margin-insulated.

If it fails, Sun will hunt elsewhere. If it succeeds, the “Tale of Two Companies” becomes a singular story of an Indian giant transforming into a diversified global innovator.

The pattern is clear: Sun does not stand still. Organon, once discarded, has become indispensable.

Sources:

| Source | Citation/Reference |

| Sun Pharma Milestones | official corporate filings (1983-2025) |

| Organon FY2025 Results | Form 10-K, February 2026 ($6.216B Revenue; $8.0B Debt) |

| Leadership Change | Organon Press Release, Oct 2025 (Kevin Ali departure; Interim CEO Joe Morrissey) |

| Sun/Organon Bid Report | Economic Times, April 8, 2026 (Binding $12B offer details) |

| Due Diligence Status | Bloomberg Law, April 3, 2026 (“Sun Pharma Nears Completion of DD”) |

| Market Data | NSE/BSE stock price tracking as of April 10, 2026 (~4.5% dip on bid news) |

Editor’s Note for MedicinMan: This analysis treats the reported bid as a strategic indicator. As of press date, no definitive agreement has been filed with the exchanges. All financial figures are cross-referenced with the 2025-26 annual disclosures.

All Images are AI Crafted for Illustration Only. E&OE

{kind=link}