Is Obesity (Drugs) Masking Underlying (Metabolic) Risk Factors in Indian Pharma?

Executive Summary

The Indian Pharmaceutical Market (IPM) entered 2026 with strong momentum, delivering approximately 11% year-on-year growth in February 2026. The narrative appears compelling: chronic therapies are expanding, volumes are stabilizing, and GLP-1 agonists are positioning India within the global specialty drug landscape.

However, beneath this momentum lies a more complex reality. This analysis presents three grounded conclusions:

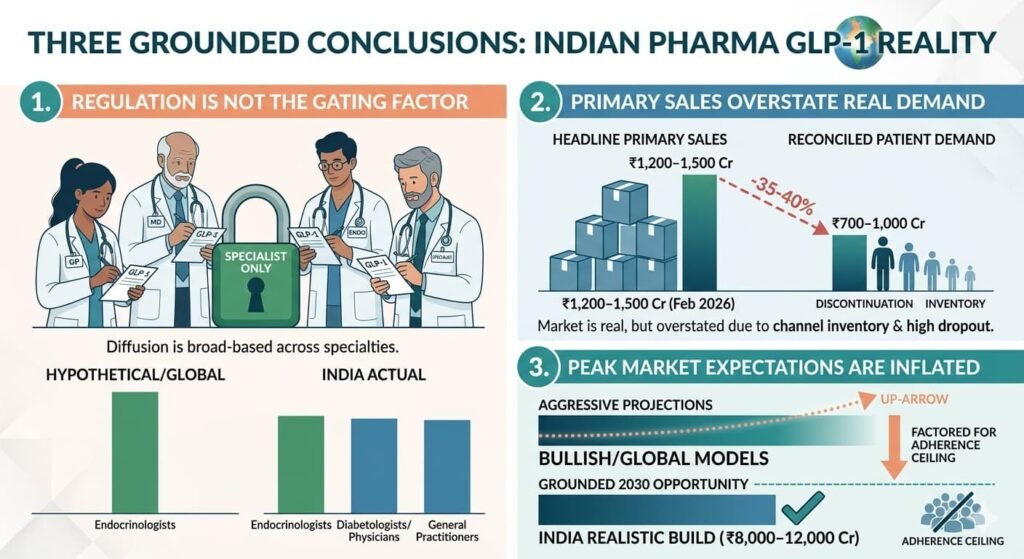

- Regulation is not the primary constraint — GLP-1 prescribing is not restricted to endocrinologists in practice; adoption is broad-based across specialties.

- Primary sales overstate real demand — A meaningful portion of the reported GLP-1 market reflects channel inventory rather than patient consumption.

- Peak market expectations are inflated — A realistic 2030 GLP-1 opportunity is ₹8,000–12,000 crore, materially below aggressive projections.

1. Prescription Reality — Diffusion, Not Restriction

The Regulatory Position

GLP-1 therapies are classified as Schedule H prescription drugs in India. While clinical practice often favors specialist-led initiation, there is no enforceable restriction limiting prescribing exclusively to endocrinologists. Moreover, India lacks a systematic, large-scale prescription audit mechanism, limiting the enforceability of any such guidance.

The Operating Reality

Prescription behavior in India is shaped less by regulation and more by field-force reach and patient demand. The pharmaceutical industry deploys an estimated ~600,000 medical representatives (MRs) nationwide. This enables high-frequency engagement across both doctors and retail pharmacies, creating rapid therapy diffusion across specialties.

Prescriber Mix (Indicative)

| Segment | Share of Usage |

|---|---|

| Endocrinologists | 25–35% |

| Diabetologists / Physicians | 30–40% |

| General Practitioners | 15–25% |

| Others (Cardio, Gynae, etc.) | 10–15% |

Implication:

GLP-1 adoption is commercially diffused and multi-specialty, not tightly specialist-controlled.

2. Field Force Economics — Scale Drives Adoption

Large Indian pharmaceutical companies deploy field forces ranging from 5,000 to 15,000 representatives, enabling deep geographic and prescriber coverage.

Early movers such as Sun Pharma, Dr. Reddy’s, and Zydus Lifesciences are structurally well-positioned to scale GLP-1 adoption. However, it is critical to contextualize the revenue impact:

GLP-1 therapies are likely to contribute ~1–3% of India revenues at steady state (FY2027–28), following ramp-up in FY2026–27

Implication:

GLP-1 is a meaningful growth lever, but not a near-term company-defining revenue driver.

3. The GLP-1 Market — Primary vs Patient Reality

Current Market Structure (FY2025–26 Annualised)

- Primary sales (company to stockist): ₹1,200–1,500 crore

- Patient-level consumption: ₹700–1,000 crore

Understanding the Gap

The difference between primary and patient-level sales is explained by:

- Channel inventory (typically 2–6 weeks)

- High discontinuation rates

- Sampling and price variability

Patient-Level Dynamics

| Variable | Realistic Estimate |

|---|---|

| Active patients at a point in time | 100,000–200,000 |

| Monthly therapy cost | ₹3,000–8,000 |

| Median duration of therapy | 3–6 months |

Conclusion:

The GLP-1 market is real and growing, but headline primary sales overstate actual patient consumption.

4. The Discontinuation Problem — The Binding Constraint

Global Evidence

Large real-world datasets (~170,000 patients) indicate:

- ~30% discontinue within the first month

- ~50–60% discontinue within 3 months

Indian Context

Indian real-world data remains limited but is directionally consistent, with key drivers including:

- Gastrointestinal side effects

- Cost burden

- Variable perception of efficacy

Key Drivers of Dropout

| Factor | Impact |

|---|---|

| Gastrointestinal side effects | High |

| Cost | High |

| Expectation mismatch | Moderate |

| Injection fatigue | Moderate |

Adherence—not awareness—is the primary constraint on market expansion

5. 2030 Market — Separating Signal from Speculation

Corrected Base Population

| Parameter | Estimate |

|---|---|

| Diabetes population | ~100–110 million |

| Overweight/obese population | ~180–220 million |

| Unique addressable pool | ~250–300 million |

Realistic Market Build

| Variable | Assumption |

|---|---|

| Penetration | 1–2% |

| Treated patients | 2.5–6 million |

| Average annual spend | ₹12,000–20,000 |

Outcome

₹8,000–12,000 crore GLP-1 market by 2030 (primary sales)

Contextual Perspective

- ~5% of projected IPM size

- Comparable to a mid-sized therapy segment

- Significant, but not transformational

6. Therapy-Level Reality Check

Vaccines — Structural Growth

- High-teens to mid-20% growth (depending on dataset)

- Driven by volume expansion and adult immunization awareness

Verdict: Structural long-term growth segment

Cardiac Therapies

- Growth largely driven by pricing and premiumisation

- Volume growth in low-to-mid single digits

Verdict: Stable, mature segment

Anti-diabetic (ex-GLP-1)

- GLP-1 inflates overall growth rates

- Legacy oral therapies slowing

Verdict: Transition phase underway

Acute Therapies

- ~40–45% of IPM

- Volume-driven, seasonal

Verdict: Core cash flow segment

Respiratory

- Demand linked to pollution cycles

- Episodic growth patterns

Verdict: Non-structural growth

7. Investment Implications

What May Be Mispriced

- Over-reliance on primary sales growth as a proxy for demand

- Underestimation of:

- Adherence-driven drop-offs

- Channel inventory cycles

Likely Outcomes

- Slower-than-expected secondary sales growth

- Periodic inventory corrections

- Recalibration of growth expectations in select companies

The Core Takeaway

Follow the patient, not the primary sales

GLP-1 therapies represent a genuine therapeutic advancement, but they do not resolve the structural constraints of Indian pharma:

- Affordability limitations

- Adherence challenges

- Side-effect profile

- Reversibility of benefits post-cessation

The risk is not that GLP-1 under-delivers—but that its early success is over-interpreted as systemic transformation.

Appendix — Sources and Evidence Quality

High Confidence

- Pharmarack / IQVIA — Market growth, therapy segmentation

- IDF Diabetes Atlas — Prevalence estimates

- Blue Health Intelligence — Adherence trends

- CareEdge — Market projections

Moderate Confidence

- ET Pharma, BioSpectrum — Market size, pricing, inventory insights

Directional / Non-Audited

- Field force estimates

- Prescriber mix distribution

- Company-level GLP-1 revenue contribution estimates

About the Author

Anup Soans is Founder-Editor of MedicinMan, a platform at the intersection of medicine, markets, and strategy.

All Images are AI Crafted for Illustration Only. E&OE

{kind=link}