The Indian Pharmaceutical Market (IPM) has entered a definitive “Gold Rush” phase. The launch of Semaglutide branded generics in late March 2026 has served as a primary catalyst for a historic shift in metabolic health therapy. While the broader market maintains a healthy 10.1% monthly value growth (reaching ₹20,012 Cr), the real story lies in the structural disruption of the chronic therapy segment.

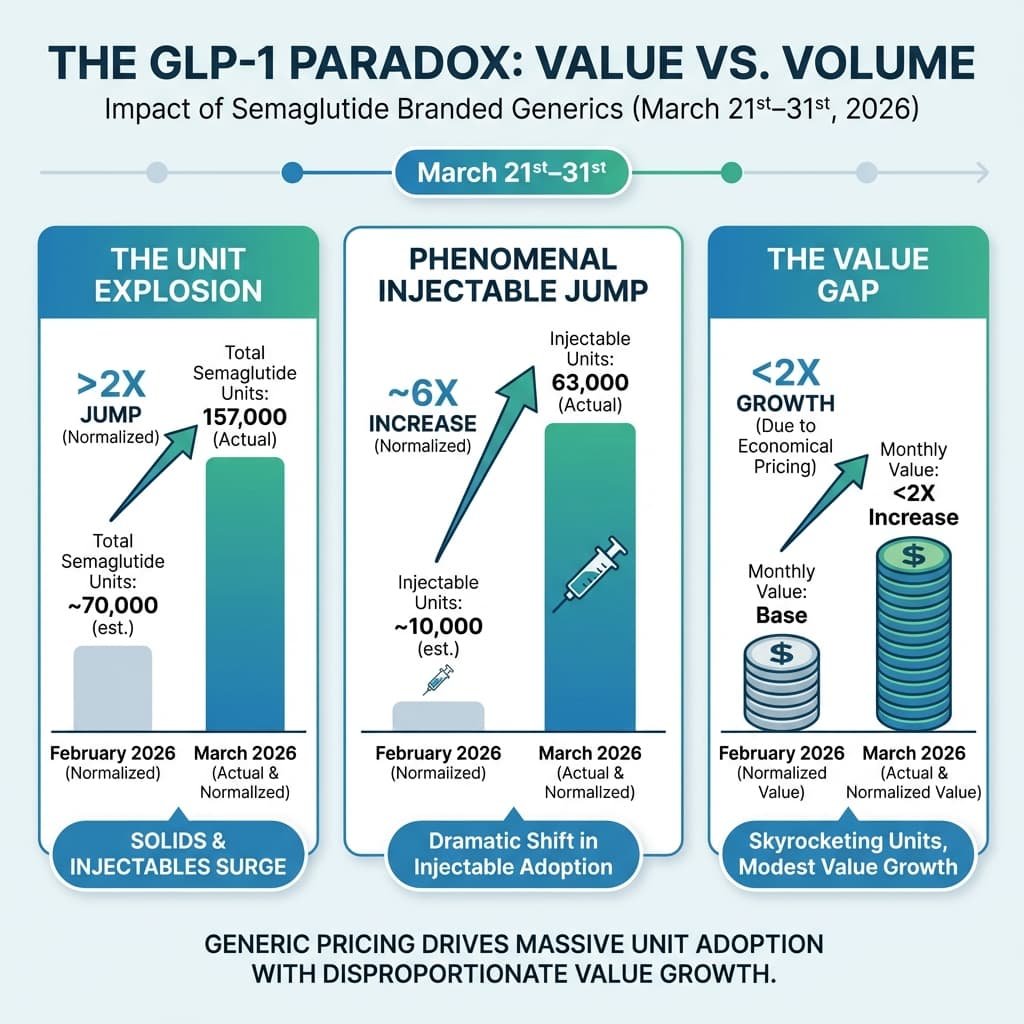

1. The GLP-1 Paradox: Value vs. Volume

The most significant trend is the explosive entry of Semaglutide branded generics. Within just 10 days of the generic launch (March 21st–31st), the market shifted dramatically:

- The Unit Explosion: Total Semaglutide units (solids and injectables) surged to 157,000 in March. Normalized to 30 days, this represents a >2X jump in units.

- Phenomenal Injectable Jump: The shift is most visible in injectables, which saw an actual unit jump to 63,000 in March, a normalized ~6X increase over February 2026.

- The Value Gap: Because generic pricing is extremely economical, the jump in monthly value was <2X, even as unit adoption skyrocketed.

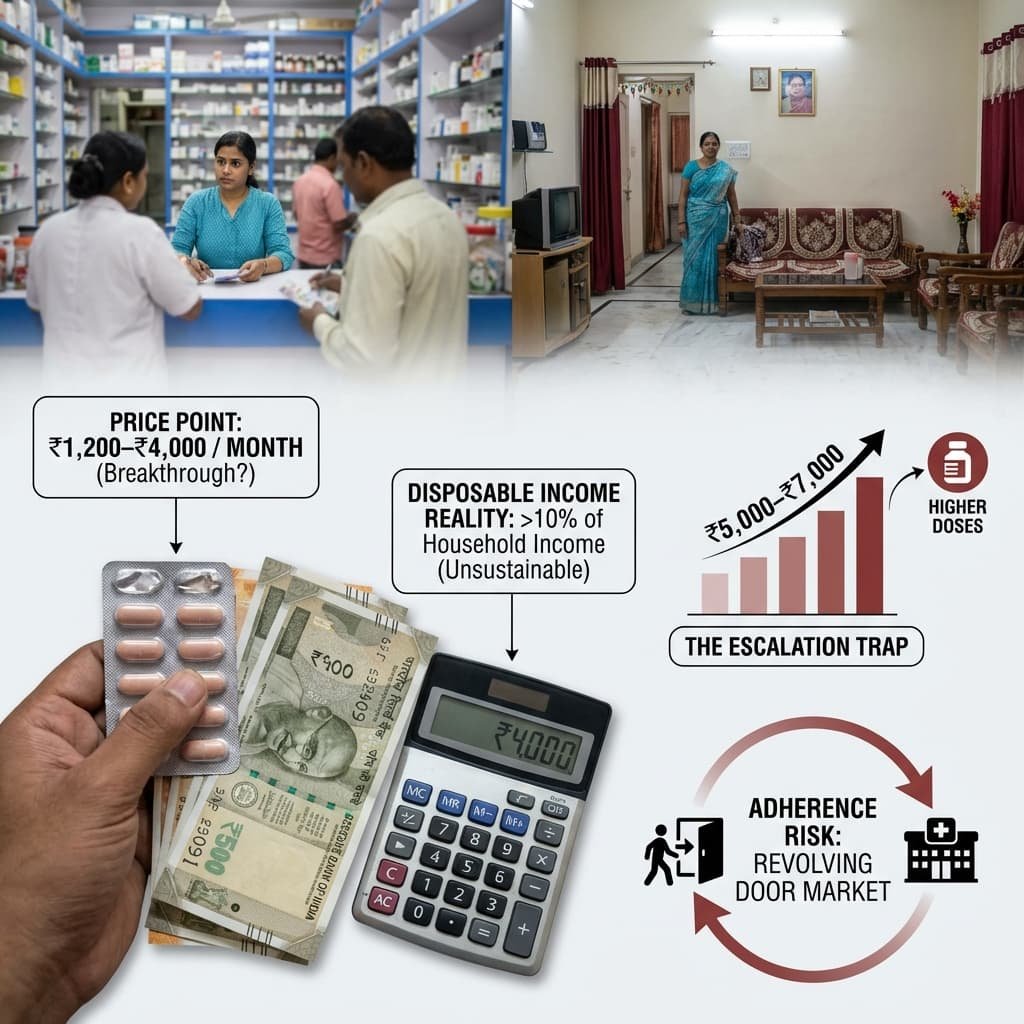

2. Affordability and the Sustainability Question

While a price point of ₹1,200–₹4,000 per month is hailed as a breakthrough, its long-term sustainability is questionable against India’s economic reality.

- Disposable Income Reality: For a chronic medication to be sustainable in India’s high Out-of-Pocket Expenditure (OOPE) environment, it typically should not exceed 10% of a household’s monthly disposable income.

- The Escalation Trap: While “starting doses” are affordable, clinical necessity often requires dose escalation. At higher doses, even generic costs can jump to ₹5,000–₹7,000 per month, potentially pushing the therapy out of reach for the middle class.

- Adherence Risk: Experiences in comparable markets show that while volume spikes early, adherence often drops sharply after 6 months due to cost fatigue. If patients stop after a few months, the “market size” is a revolving door rather than a stable foundation.

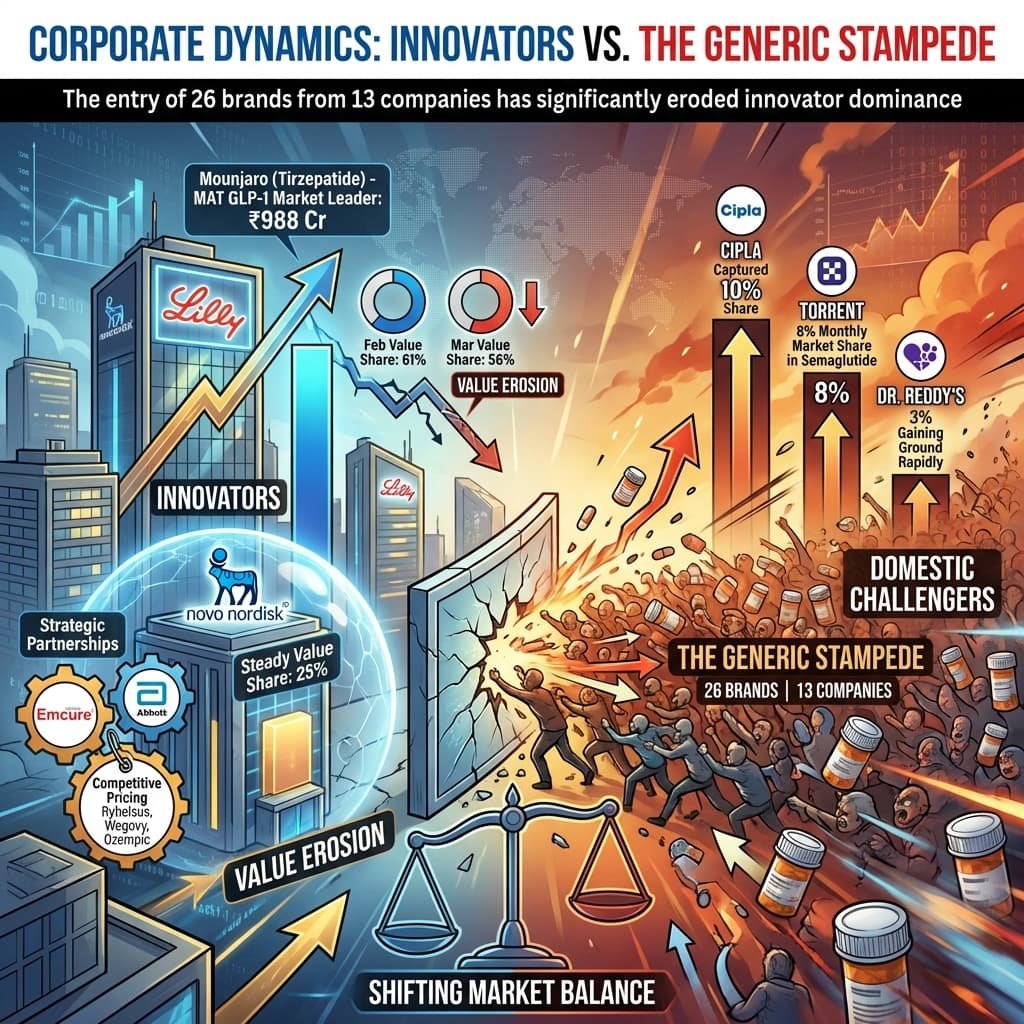

3. Corporate Dynamics: Innovators vs. The Generic Stampede

The entry of 26 brands from 13 companies has significantly eroded innovator dominance.

- Eli Lilly’s Value Erosion: While Tirzepatide (Mounjaro) leads the MAT GLP-1 market at ₹988 Cr, its monthly value share dropped from 61% in February to 56% in March.

- Novo Nordisk’s Resilience: Novo Nordisk has managed to hold its ground better, maintaining a steady 25% value share through strategic partnerships with Emcure and Abbott and competitive pricing for its Semaglutide brands (Rybelsus, Wegovy, Ozempic).

- Domestic Challengers: Cipla has captured a 10% share, while Torrent (8% monthly market share in Semaglutide) and Dr. Reddy’s (3%) are gaining ground rapidly.

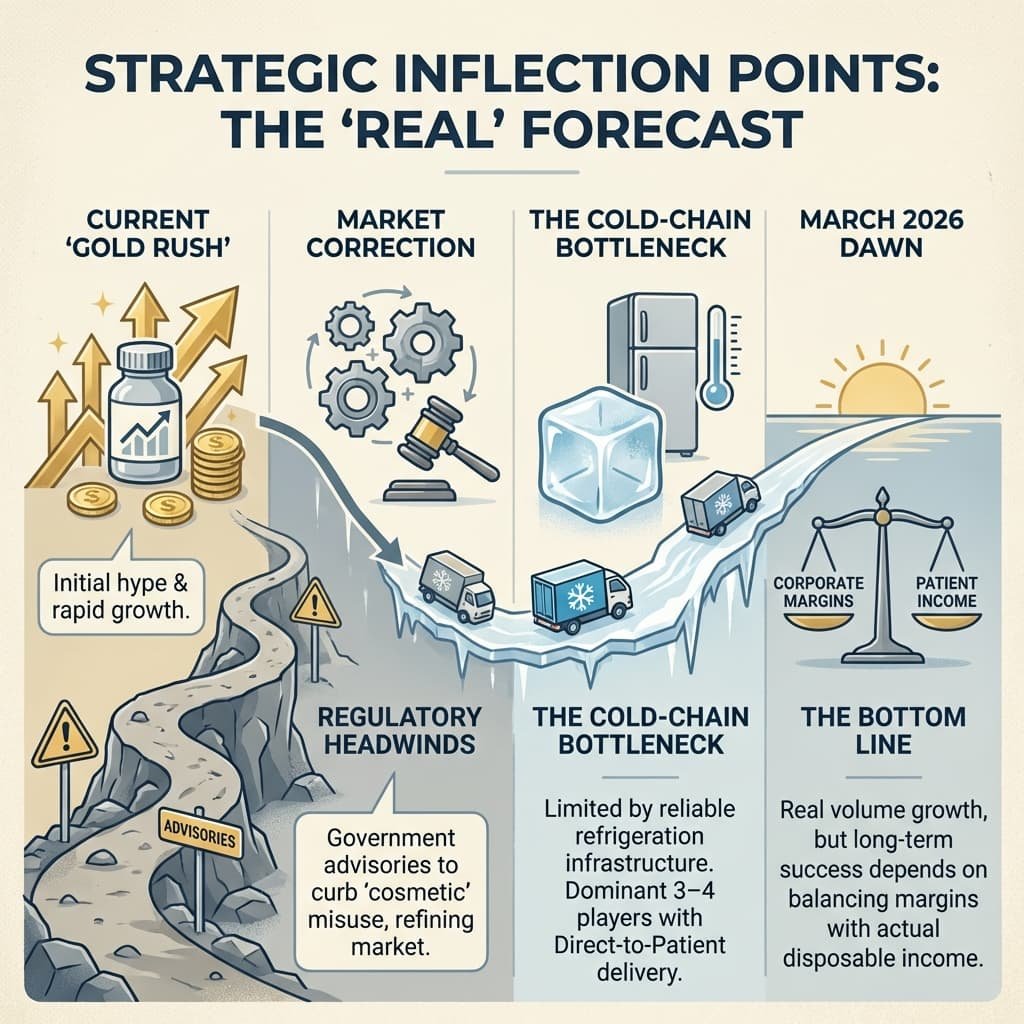

4. Strategic Inflection Points: The “Real” Forecast

The current “Gold Rush” will likely be followed by a market correction:

- Regulatory Headwinds: Upcoming government advisories to curb “cosmetic” misuse may refine the market, potentially slowing the initial growth trajectory.

- The Cold-Chain Bottleneck: The real market size is currently limited by reliable refrigeration infrastructure. Companies that master Direct-to-Patient cold-chain delivery will likely be the 3–4 players who eventually dominate this segment.

The Bottom Line: March 2026 was the “Dawn” of a new therapy class in India. The volume growth is real, but long-term success depends on moving beyond the initial hype to build a model that balances corporate margins with the actual disposable income of the Indian patient.

Sources:

- Pharmarack PharmaTrac (MAT March 2026 Report): Primary source for all IPM value/unit growth, therapy performance, and brand rankings.

- Can Eli Lilly Outrun the Semaglutide Stampede? (MedicinMan, April 2026): Analyzes the competitive threat to Tirzepatide from upcoming generic Semaglutide and pipeline candidates like Orforglipron.

- Semaglutide: Just Another Off-Patent Generic? (MedicinMan, March 2026): Explores why Semaglutide is a “different beast” requiring high-trust delivery devices and cold-chain integrity.

- ICMR-INDIAB Study: Baseline data on obesity and diabetes prevalence in India, defining the Total Addressable Market (TAM).

- National Health Accounts (NHA) India: Data on Out-of-Pocket Expenditure (OOPE) and household healthcare spending thresholds.

All Images are AI Crafted for Illustration Only. E&OE

{kind=link}