Every month, MedicinMan in partnership with IMS Health, brings our readers the latest industry numbers related to sales and revenues of the top companies, brands and therapy areas in the Indian Pharmaceutical Market.

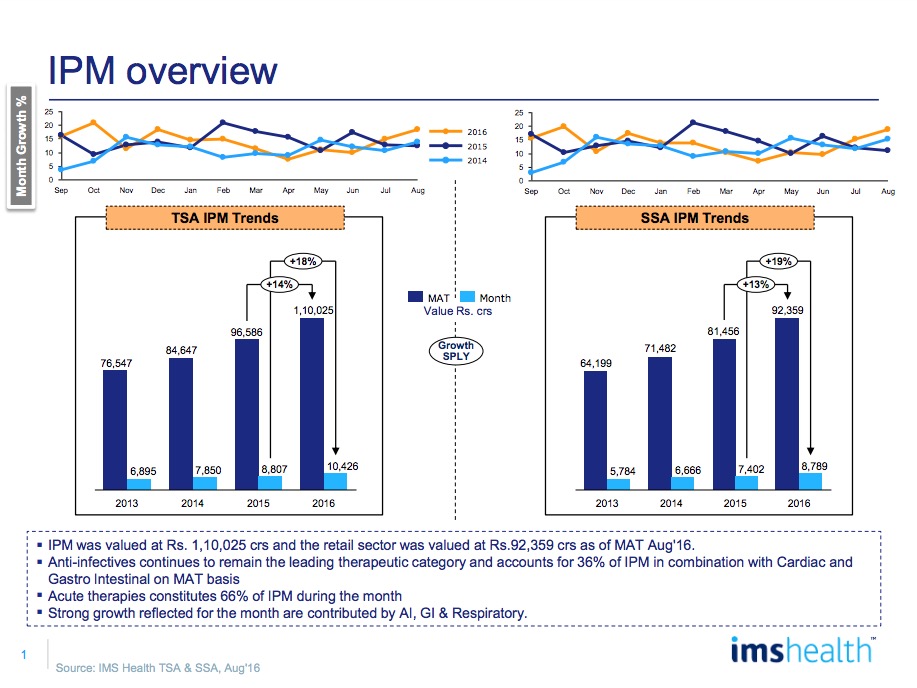

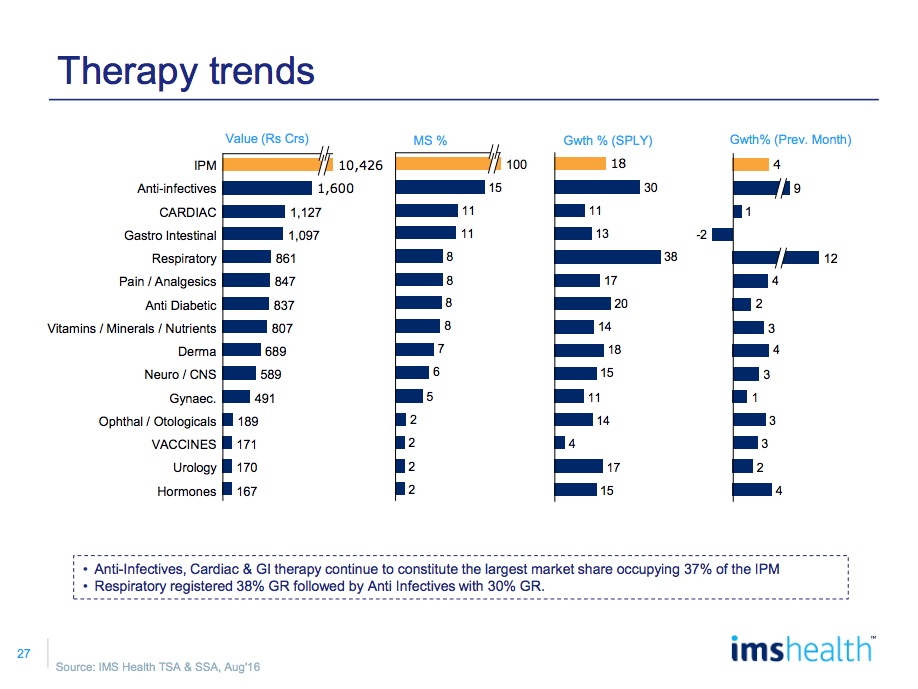

TThe Indian Pharmaceutical Market (IPM) was valued at Rs. 10,426 crores in the month of August 2016 clocking a strong 18% growth over same period last year (SPLY). This was the second consecutive month where the IPM crossed the 10,000 crore mark. On a MAT August 2016 basis, the industry was valued at Rs. 110,025 crores and reflected a 14% growth with volumes contributing around 35% of this growth.The Indian Pharmaceutical Market (IPM) was valued at Rs. 10,426 crores in the month of August 2016 clocking a strong 18% growth over same period last year (SPLY). This was the second consecutive month where the IPM crossed the 10,000 crore mark.

The retail channel remained the largest channel in IPM contributing 84% of the overall sales and reflected a 13% growth. The hospital and doctor channel contributed to 16% of the overall sales and reflected a growth of 17% on a MAT August basis. It is expected that the hospital channel will continue to report robust growth rates due to rapid capacity expansion in this space. As per IMS Health data which captures sales from trade stockists, more than 10 Therapy Areas in the IPM have already crossed a sale of Rs. 500 crores in the hospital segment viz. Anti Infectives, Cardiac, Gastrointestinals, Pain, Neuro, VMN, Gynae, Anti-diabetics, Vaccines and Respiratory.

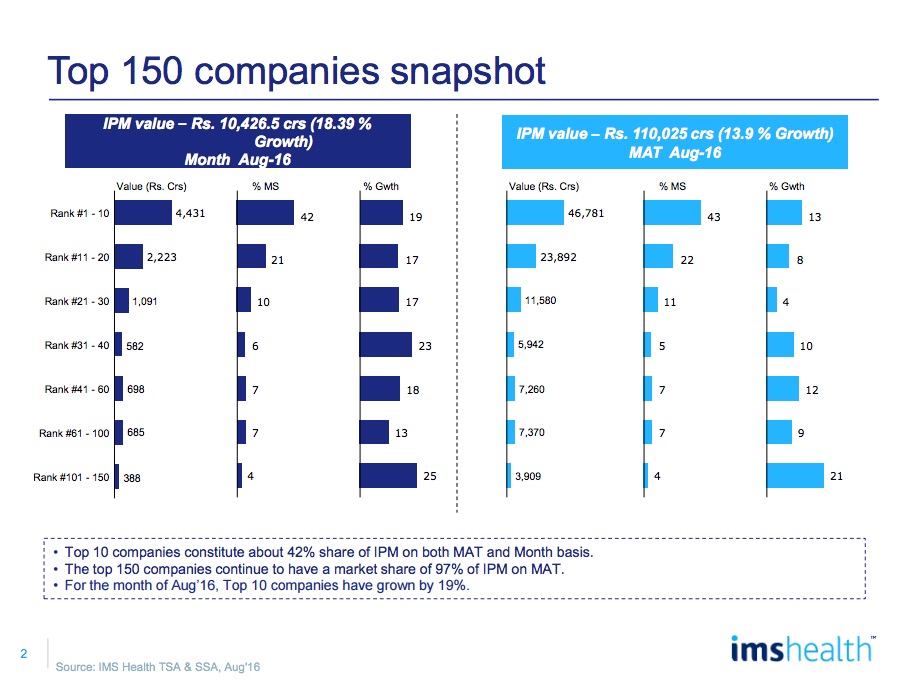

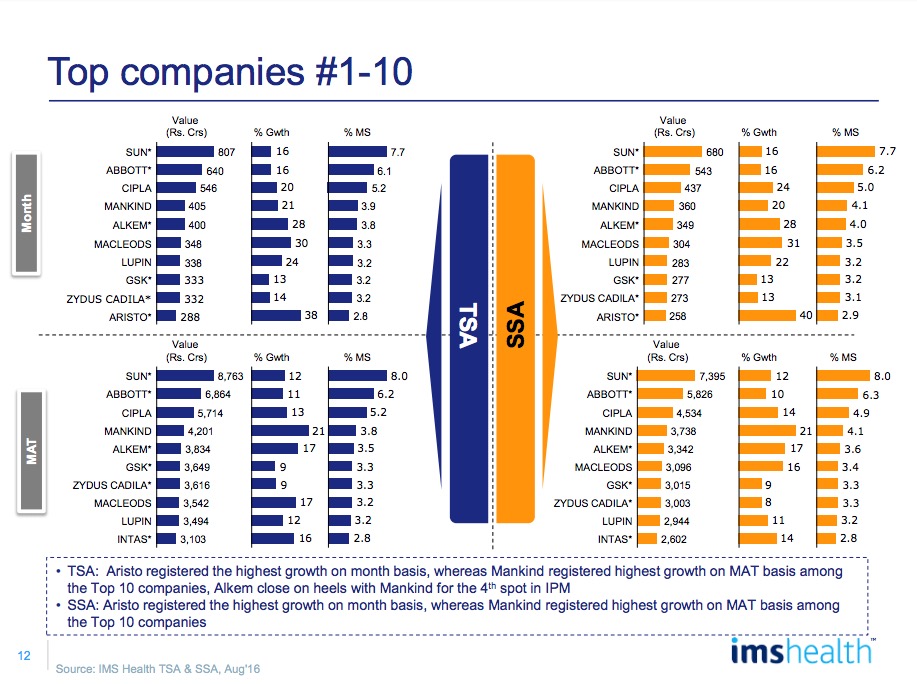

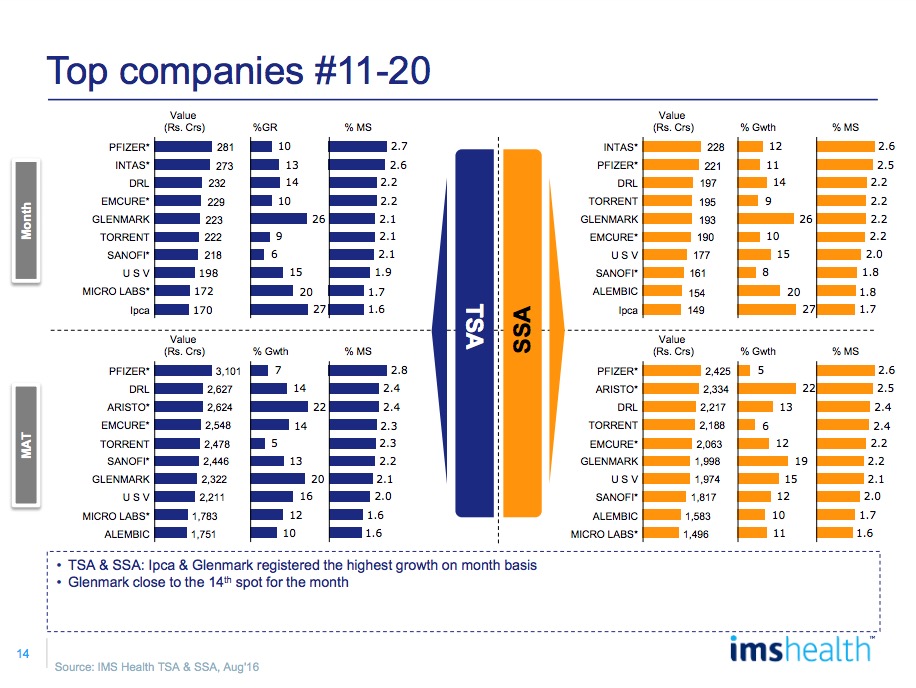

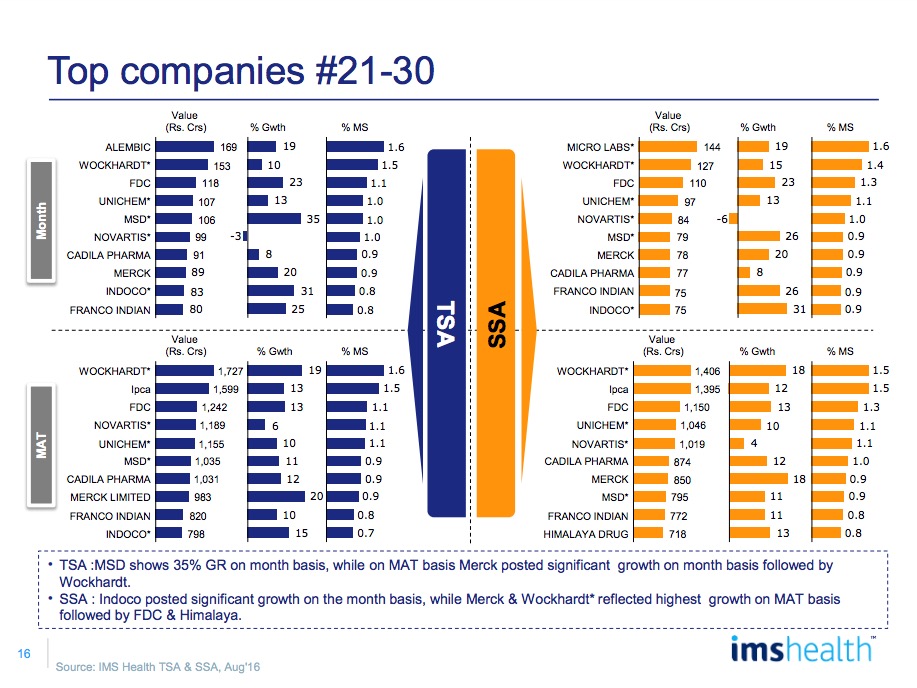

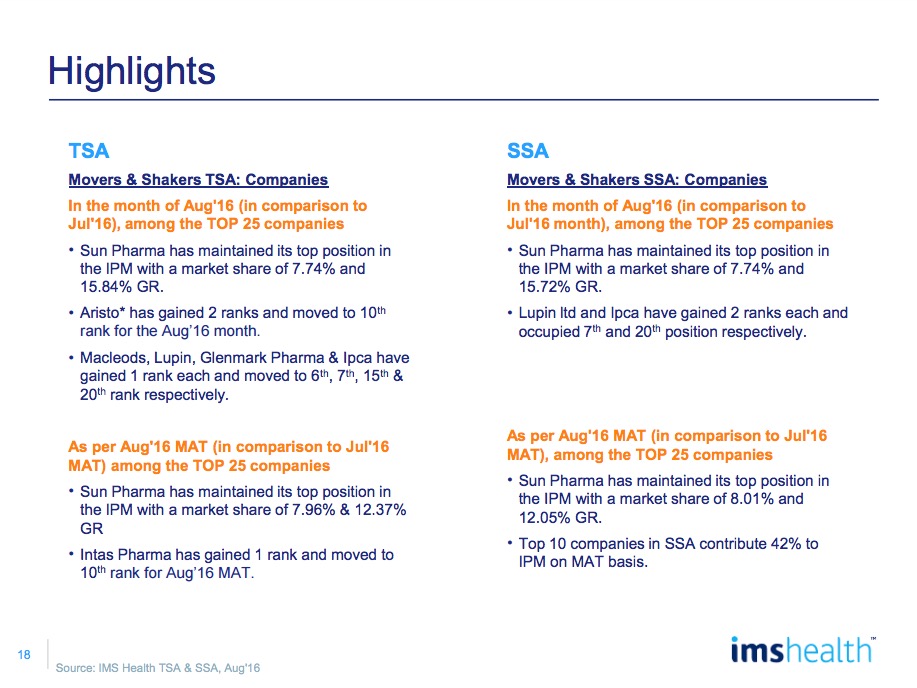

IPM continued to remain fragmented with top 10 companies occupying 42% of the share and companies across value buckets reflecting strong double digit growth for the month. Top 10 companies grew at 19% for the month of August 2016 while companies in the 11-20 and 21-30 slabs grew at 17% each.

Among the top 10 companies, Cipla (20%), Mankind (21%), Alkem (28%), Macleods (30%), Lupin (24%) and Aristo (38%) grew faster than IPM for the month.

Among the top 10 companies, Cipla (20%), Mankind (21%), Alkem (28%), Macleods (30%), Lupin (24%) and Aristo (38%) grew faster than IPM for the month while in the 11-20 companies, Glenmark (26%), Micro labs (20%) and IPCA (27%) outpaced the market.

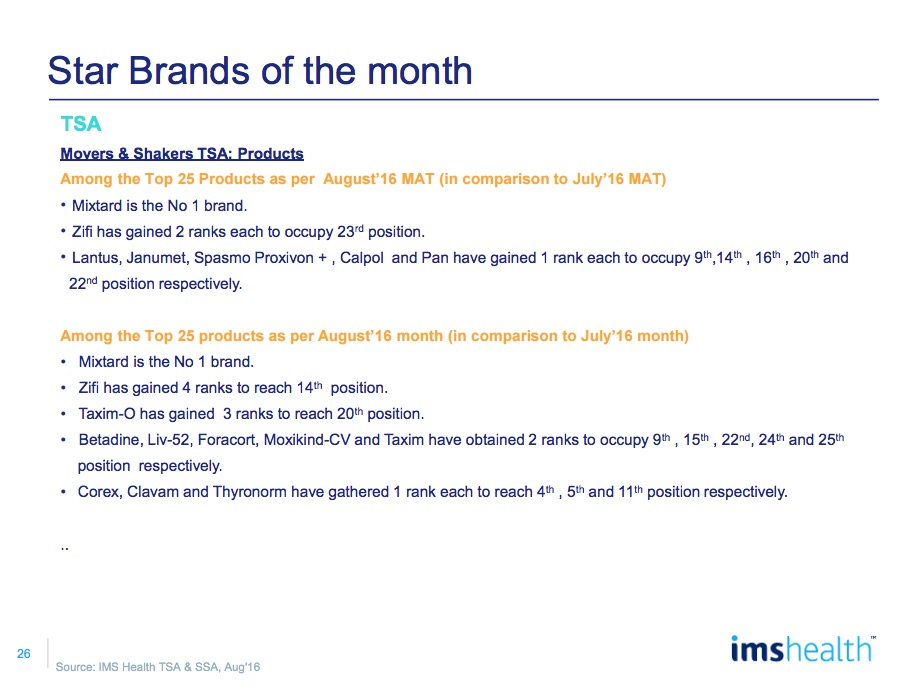

Among top 25 companies, Aristo gained 2 ranks and moved to 10th rank for the month while Macleods, Lupin, Glenmark & Ipca gained 1 rank each and moved to 6th, 7th, 15th and 20th rank respectively vis-à-vis July 2016.

Domestic companies continued to dominate the market with a 79% share in August 2016 with a growth of 20.1%.

Domestic companies continued to dominate the market with a 79% share in August 2016 with a growth of 20.1%. MNCs continued to reflect an improvement in growth, clocking a 12.4% growth vis-à-vis a 9.3% in July 2016. Large MNCs like Abbott, GSK and Pfizer which contributed around 57% of the total MNC share in the month reflected growths of 16%, 13% and 10% respectively. GSK growth stabilized after a spurt last month while Sanofi reflected a 6% growth reflecting a slowdown.

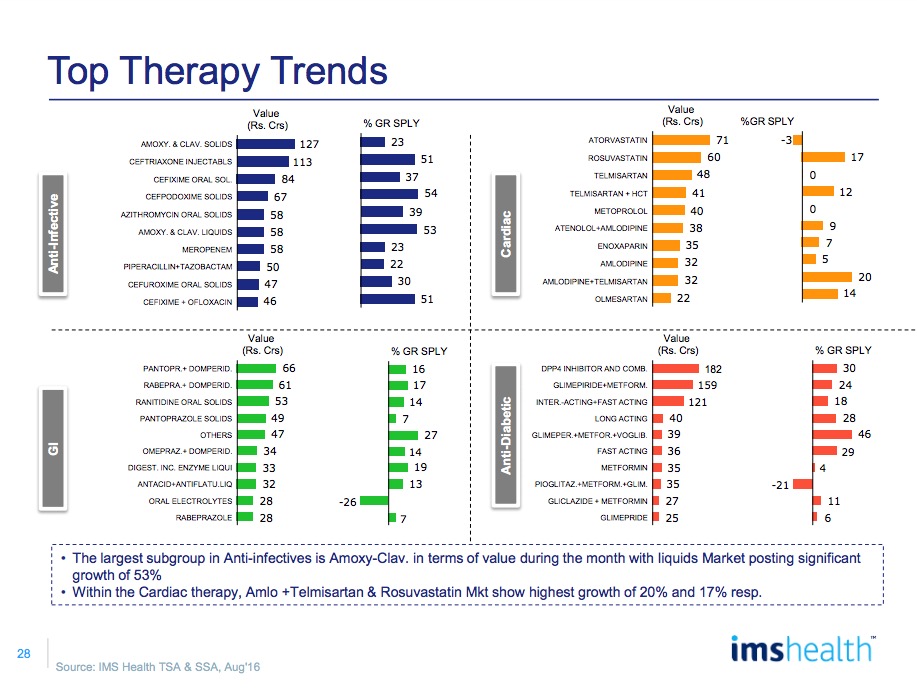

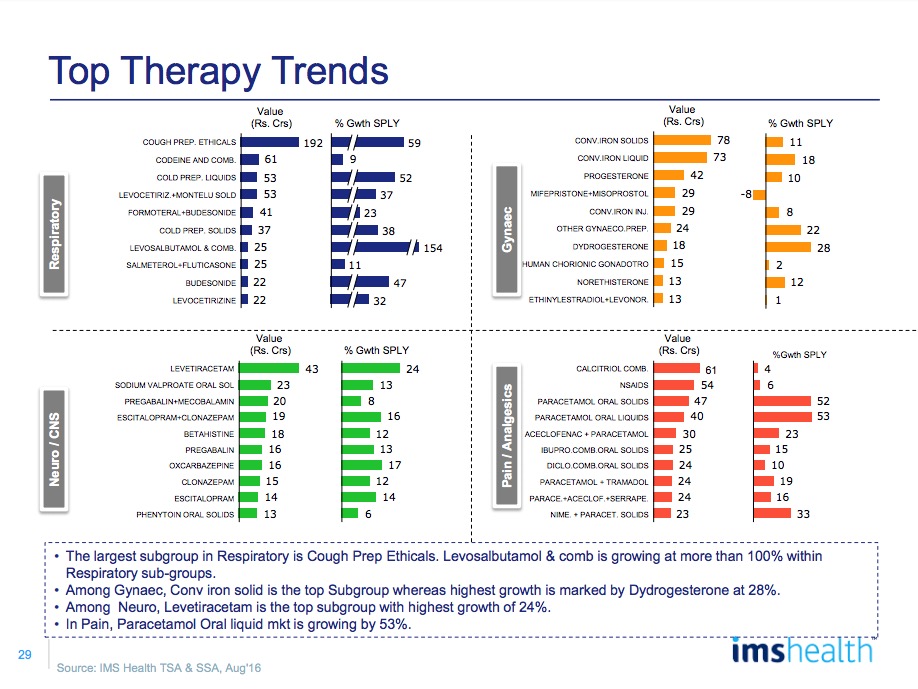

Acute therapies remained the strongest pillar of IPM with a 68% contribution to the total market; acute therapy areas (19.6%) continued to outpace chronic therapy areas (15.9%) in terms of growth carrying forward the momentum from last month. Anti-infectives (30%), Cough Preparations (59%), Pain & Analgesics (17%) spearheaded the growth in the acute space while Anti-Diabetics (20%) and Urologicals (17%) were the fastest growing chronic therapy areas.

Anti-infectives was by far the largest therapy area for the month with a revenue of Rs. 1600 crores reflecting a 30% growth on the back of a good monsoon witnessed across the country.

Anti-infectives was by far the largest therapy area for the month with a revenue of Rs. 1600 crores reflecting a 30% growth on the back of a good monsoon witnessed across the country. This was an impressive performance considering 14% of the portfolio impacted by the FDC ban comprised of anti-infectives while it was also one of the largest therapy areas to be affected by the NLEM notification. Top 10 anti-infective molecules reflected an average growth of 38% for the month with Cefpodoxime, Ceftriaxone injectables and Amoxyclav liquids reflecting growth of 54%, 51% and 53% respectively.

Cardiac therapy area regained its no. 2 position in IPM for the month of August 2016 clocking a revenue of Rs. 1127 crores growing at 11%.

Cardiac therapy area regained its no. 2 position in IPM for the month of August 2016 clocking a revenue of Rs. 1127 crores growing at 11%. The therapy area was driven by Rosuvastatin (17% growth), Amlodipine+ Telmisartan (20% growth). Telmisartan which recently came under price control reflected a 0% growth which was an improvement over the -3% growth it reflected last month.

Gastrointestinals was the 3rd largest therapy area for the month garnering a revenue of Rs. 1097 crores with a growth of 13%. PPIs and their combination with Domperidone reflected strong double digit growth. Rabeprazole + Domperidone, Pantoprazole + Domperidone and ranitidine were among the fastest growing molecules with a growth of 17%, 16% and 14% respectively. Digestive enzymatic liquids reflected a 19% growth driven primarily by the east zone.

Respiratory emerged to be the 4th largest therapy area for the month gaining 3 ranks over July 2016 and clocked a 38% growth over SPLY. Cough preparations, Levosalbutamol combinations and cold preparations (liquids & solids) were among the fastest growing categories in the respiratory space reflecting growth of 59%, 154%, 52% and 38% respectively.

Among chronic therapy areas, Anti-Diabetic, Urology and Neurology were among the fast growing therapy areas, growing at 20% and 17% and 15% for the month respectively. DPP4 inhibitors driven by teneligliptin & the unprecedented number of players it has got into the market and glim+ met formulations spearheaded growth for the AD market. In the neurology space Levetiracetam continued to be the fastest growing molecule in neuro psychiatry for the month clocking a value of Rs. 43 crores with a growth of 24% in Aug’16. Escitalopram plain & its combination with Clonazepam found place among the fastest growing CNS molecules for the month with a growth of 14% and 16% respectively.

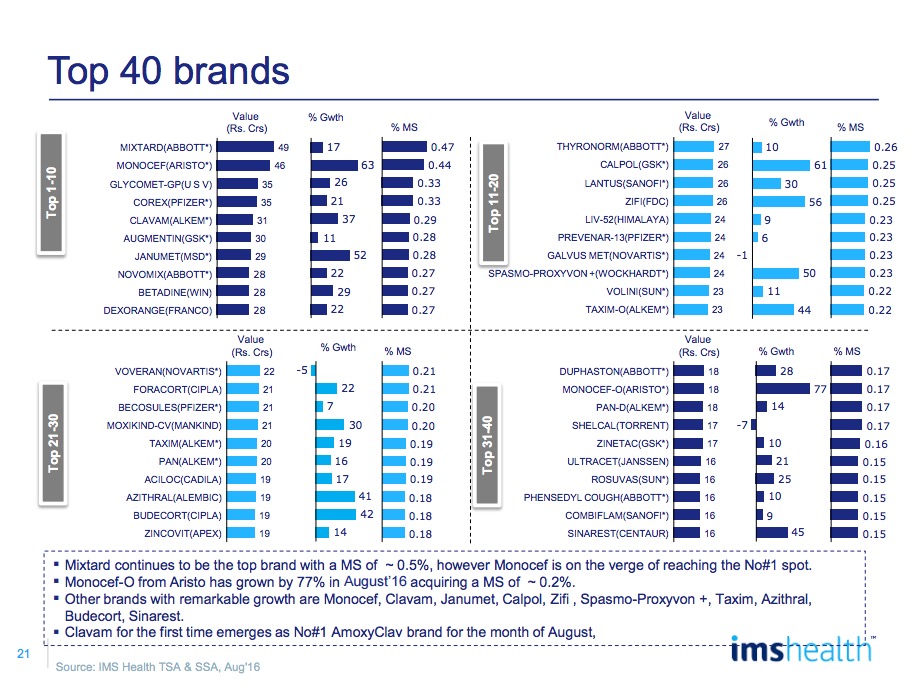

Brand building efforts across top companies continued to be evident with 8 out of top 10 companies driving robust double digit growth for their portfolio falling under top 300 brands with only Sanofi and Zydus reflecting single digit growth. Clavam, Pan and Taxim-O drove Alkem performance for the month while Augmentin and Calpol propelled GSK. Moxikind-CV and Manforce spearheaded growth for Mankind. Clexane, Cardace and Targocid performance led to sluggish growth for Sanofi while Atorva, Aten & Skinlite led to near stagnancy for Zydus.

Company

No. of Brands in Top 300 For Aug 2016

Value. of Brands in Top 300 For Aug 2016(Rs. Crores)

Growth

2015

2016

2015

2016

ABBOTT

25

28

255

328

29%

SUN

29

28

234

271

16%

CIPLA

22

23

176

227

28%

PFIZER

17

16

169

191

13%

GLAXOSMITHKLINE

13

15

165

201

22%

ALKEM

14

15

146

194

33%

MANKIND

9

12

69

104

52%

ARISTO PHARMA

10

11

102

157

54%

SANOFI

12

11

111

120

7%

ZYDUS CADILA

13

11

85

86

1%

Note: Companies have been ranked as per number of brands which feature in top 300 brands in IPM.

IPM Snapshot

TSA = Total Sales Audit which includes Hospital, doctor and retail channels

SSA = Secondary Sales Audit which is retail channel sales from the local pharmacy retailers

-

- IMS Market Reflection Report August 2016

-

- IMS Market Reflection Report August 2016

-

- IMS Market Reflection Report August 2016

-

- IMS Market Reflection Report August 2016

-

- IMS Market Reflection Report August 2016

-

- IMS Market Reflection Report August 2016

-

- IMS Market Reflection Report August 2016

-

- IMS Market Reflection Report August 2016

-

- IMS Market Reflection Report August 2016

-

- IMS Market Reflection Report August 2016

-

- IMS Market Reflection Report August 2016

IMS Health is a leading global information and technology services company providing clients in the healthcare industry with end-to-end solutions to measure and improve their performance.